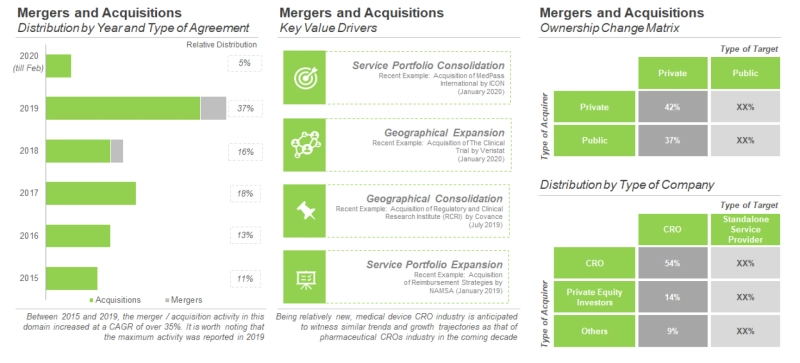

The medical device CRO domain is witnessing significant consolidation activity since the past few years. This can be attributed to the rise in competition within this domain, which has further compelled medical device service providers to diversify their portfolios through mergers and acquisitions. More than 35 instances of mergers and acquisitions have been reported in this domain, during the period 2015 and 2020 (till mid-March). It is worth noting that, of the total number of acquirers, 58% were privately held firms, while the rest were public companies. However, majority (94%) of the acquired companies were private companies.

Majority of the deals in this domain were acquisitions (92%). Examples of mergers signed in the medical device CROs industry include (in reverse chronological order) the merger of Cato Research with SMS-Oncology (October 2019), Factory CRO with Boston Biomedical Associates (January 2019) and Factory CRO with Five Corners (June 2018).

In terms of geography, maximum number of deals were signed in North America, followed by those inked by Europe based players. Further, medical device service providers based in North America witnessed significant intracontinental consolidation activity, as compared to intercontinental deals, which were signed only with firms headquartered in Europe. Similarly, all the intercontinental deals signed by companies based in the Asia-Pacific region were with the firms based in North America; examples include (in reverse chronological order) acquisition of Target Health (US) by dMed (China) in June 2019 and DZS Clinical Services (US) by WDB Holdings (Japan) in September 2018.

Key Value Drivers

The various value drivers that have been considered in this analysis have been briefly described below.

Geographical consolidation: Instances wherein a firm acquired another player based in the same geography in order to consolidate the presence of the former entity.Geographical expansion: Instances wherein a firm acquired another player in a different geography in order to expand the geographical reach of the former entity.Service portfolio consolidation: Instances wherein both the companies have a similar portfolio, however, the firm acquires another firm to enhance and strength its service portfolio.Service portfolio expansion: Instances wherein a firm acquired another firm to incorporate additional services to the former’s existing portfolio of offerings.Figure 11.10 presents an overview of the acquisitions that took place in the given time period, highlighting the distribution of the key value drivers across different years.

Figure 11.10 Acquisitions: Distribution by Key Value Drivers and Year of Acquisition

Note 1: For 2020, acquisition instances have been captured till mid-March 2020

Note 2: Acquisition instances having more than one value driver have been counted multiple times

Note 3: Instances for which the information on key value drivers was available have been included in this representation

Source: Roots Analysis

As can be observed in the figure, during the period 2015-2019, the merger and acquisition activity in this domain was focused on all the key value drivers. However, initially some fluctuations can be observed specifically for geographical consolidation. In the year 2018, service portfolio expansion and geographical consolidation emerged as the key value drivers, however, in 2020, the focus has shifted to service portfolio consolidation.