Australia’s telecommunications industry is a dynamic and evolving sector, playing a crucial role in the country’s economic and social development. This article delves into the current state of the market, exploring key players, trends, challenges, and future prospects.

Market Size and Structure

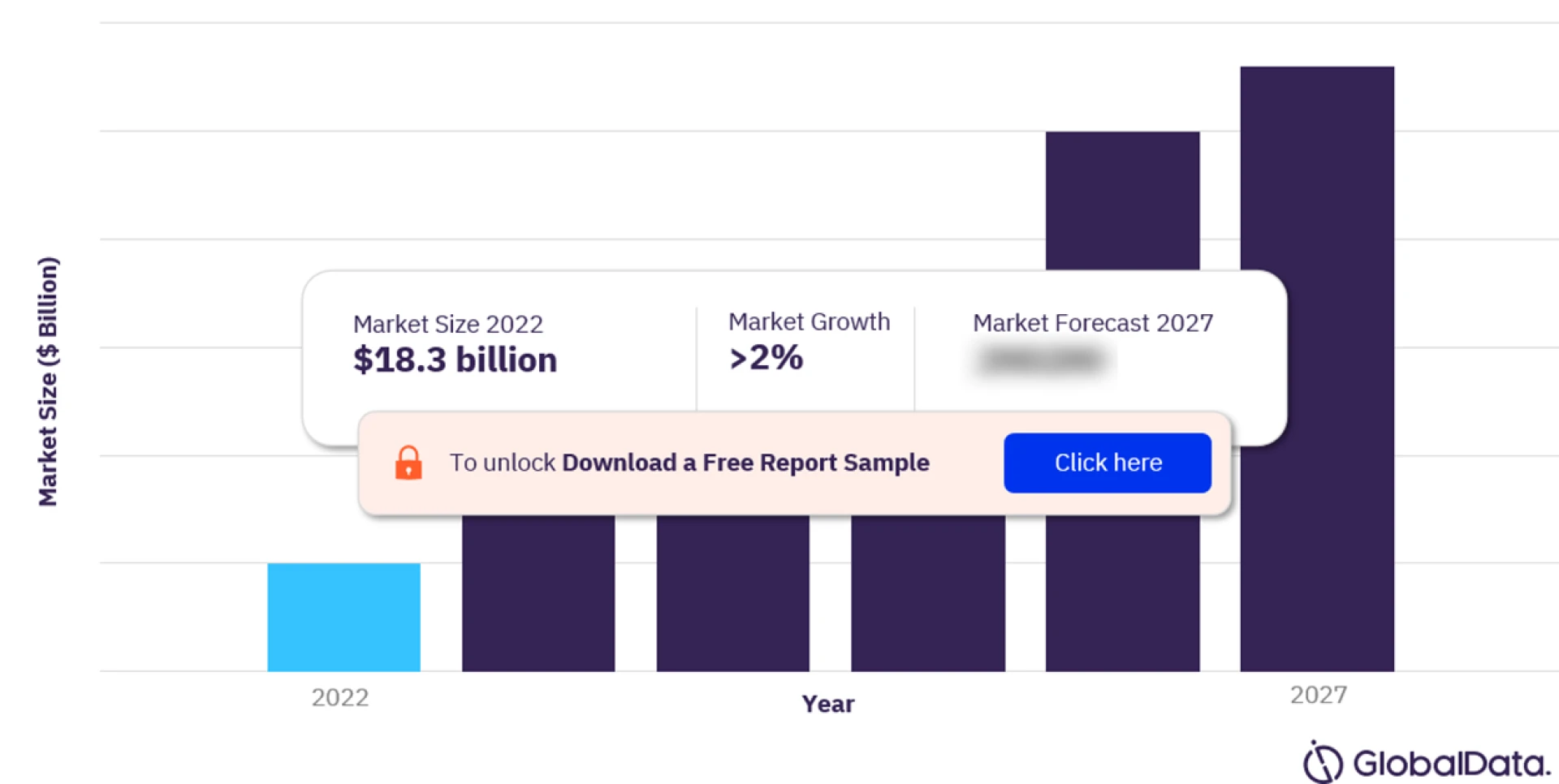

The Australian telecommunications market is estimated to be worth USD 22.13 billion in 2024, with a projected growth rate of 1.60% reaching USD 23.96 billion by 2029 [1]. The market structure is characterized by a mix of established players and emerging challengers.

Major Players

- Telstra: The dominant force in the industry, Telstra boasts the largest customer base for both mobile and fixed-line services. It offers a comprehensive suite of telecommunication products and services, including broadband internet, mobile plans, and data solutions.

- Optus: Singtel-owned Optus is Telstra’s primary competitor, providing strong competition in mobile services and fixed broadband. They are actively investing in 5G technology and network infrastructure.

- TPG Telecom: Following its merger with Vodafone Hutchison Australia (VHA) in 2022, TPG Telecom has become a significant player. They offer competitive mobile and fixed broadband plans, catering to budget-conscious consumers.

Other Notable Players:

- Macquarie Telecom: A leading provider of business telecommunication solutions, Macquarie Telecom is known for its focus on innovation and cloud-based services.

- Aussie Broadband: A rapidly growing fixed-line broadband provider, Aussie Broadband is capitalizing on the demand for high-speed fiber internet access.

Market Trends

- Shift Towards Fiber: The Australian National Broadband Network (NBN) rollout is driving a significant shift towards fiber optic infrastructure. This is enabling faster internet speeds and improved service quality for both fixed broadband and mobile data.

- Growth of Mobile Data Usage: With the increasing popularity of smartphones and data-driven applications, mobile data usage is experiencing exponential growth. This trend is prompting operators to invest in network capacity and explore new data monetization strategies.

- Consolidation and Competition: The market has witnessed consolidation with mergers like TPG-VHA, leading to a more competitive landscape with three major players. However, smaller operators and niche providers are finding opportunities in specific market segments.

- Rise of Mobile Virtual Network Operators (MVNOs): MVNOs, which utilize the network infrastructure of established operators but offer their own branded services, are gaining traction in Australia. This provides consumers with more choice and potentially lower prices.

- Focus on Customer Experience: As competition intensifies, operators are placing a greater emphasis on customer experience. This includes offering innovative service bundles, personalized data plans, and improved customer service channels.

Challenges and Opportunities

- Competition and Price Pressures: The intensified competition puts pressure on operators to keep prices competitive, potentially impacting profit margins.

- Rural Connectivity: Bridging the digital divide and ensuring equitable access to high-speed internet in remote and rural areas remains a challenge.

- Spectrum Availability: The availability of spectrum for mobile network deployment is a critical factor for future growth. Efficient allocation and management of spectrum resources will be crucial.

- Cybersecurity Threats: As reliance on telecommunication networks grows, so do cybersecurity threats. Operators need to invest in robust security measures to protect user data and infrastructure.

- Evolving Regulatory Landscape: The Australian government continues to play a significant role in regulating the telecommunications industry. Adapting to evolving regulations and ensuring compliance presents both challenges and opportunities for operators.

Future Outlook

The Australian telecommunications market is poised for continued growth, driven by factors like increasing demand for data, advancements in technology (such as 5G), and growing adoption of cloud-based services. Here’s a glimpse into what the future might hold:

- 5G Rollout: 5G technology promises significantly faster speeds, lower latency, and the potential for new applications like the Internet of Things (IoT). The rollout of 5G networks will be a key growth driver for the industry.

- Convergence of Services: We can expect further convergence of services, with operators offering bundled packages that combine mobile, fixed broadband, and other services like pay TV and streaming options.

- Focus on Innovation: Innovation will play a critical role in the future of the industry. Operators will need to invest in new technologies like network virtualization and artificial intelligence to optimize their networks and deliver a superior customer experience.

- Personalization: Personalization of services will be key to attracting and retaining customers. Operators will leverage data analytics to tailor offerings and plans to individual customer needs and preferences.

Conclusion

The Australian telecommunications market is at a crossroads, with a mix of established players and emerging forces vying for dominance.

To gain more information on Australia telecom services market forecast, download a free sample

Sign in to leave a comment.