The insurance sector is massively reliant on data. There are now many rivals and individually have a gold mine of information, but only those who can turn that data into usable insights can turn it into a gold mine. As per a predictive analytics report, the amount invested in insurance analytics in the Individual Life and Individual Health ecosystems is 70% and 40%, respectively, and is expected to increase to 90% and 80% in just two years. It is the power of data as a source of energy in today\'s world. However, this data source\'s full potential is realized by obtaining insights that will assist insurance businesses in achieving their long-term objectives. As a result, the first step for insurance businesses in maximizing the value of their data is to map out their long-term objectives. Different firms can strive for growth in various elements of the insurance process, such as overcoming everyday problems, automating complex operations, or gaining a competitive edge in the market. It may be for any one of the procedures, or it could be for all of them. Introducing analytics into the insurance process necessitates the creation of a better, more reliable database, which benefits employees even before big data is deployed. An individual is tasked with determining whether some clients spend too much time in the service center, mainly if their estimated lifetime value is low. The underwriter receives a forecasted lifetime value score based on customer journey data and insights, which they may use to make a better pricing decision. When insurance claim analytics is used, any previous activities and the customer\'s information are supplied to the insurance analytics model. As a result, future results are improved, and sales and marketing teams can target the most profitable consumers while avoiding those who are likely to be unsuccessful. Due to insurance claim analytics, decisions become more accurate, exact, and consistent, which removes most of the guesswork associated with decision-making. While training is still essential, big data allows less experienced employees to learn much more quickly because they receive recommendations based on previously proven decisions. It helps to alleviate a lot of the risk that comes with hiring a new employee. While a less experienced Insurance claim analytics solutions operator may overcompensate a consumer for a claim, an adjuster using big data is directed through recommended next steps based on previous experiences, all within the same insurance analytics system. Predicting Accurate Risk for Underwriting: Underwriting is hard work for insurers, but it is made easier with health insurance analytics. For example, if a client has been associated with reckless driving, the data-bearing would forecast a more significant premium than if the data trend predicted a lower risk profile. Minimizing Frauds: The insurance business faces a problem with fraudsters in the health insurance claim analytics process. In the insurance industry, predictive analysis helps to mitigate this. Previous fraudulent cases, for instance, are preserved in insurance massive data patterns, and the insurance companies can check to see if the trend is repeated while submitting a claim. As a result, it contributes to the elimination of fraud. Predictive analytics has been helping organizations make the most of their data, which is one of the most valuable insurance claim data an insurer can have. For years, predictive analytics and data have been working together to deliver significant insights to insurers, from predicting customer behavior to assisting underwriting procedures. Making the most of your data, on the other hand, requires excellent data administration and modeling skills. All of that data is squandered if distributed across multiple platforms, and there isn\'t a strategic plan. Take Away: Insurance claims data analytics is being used effectively by the industry\'s up-and-comers in their pricing strategy and risk selection decision-making processes. New-generation technology is gradually adopting prescriptive techniques of obtaining deep insights from big data in various insurance-related transactions such as underwriting, claim management, customer satisfaction, and policy administration to provide superior predictive analysis. It allows insurance businesses to represent analytical decision-making in all of their internal procedures and business activities.Increased Access To Data And Insights:

Consistent Employee Performance:

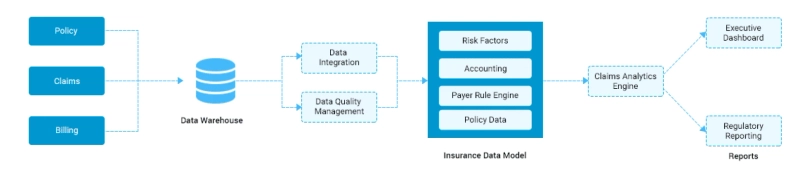

Data Management & Modeling:

The Benefits of Insurance Claims Analytics: 5 Ways It Improves Efficiency