Being an independent doctor means you wear two hats: you’re the medical expert and the boss! You need money to get new equipment, keep your business running smoothly, or make your clinic bigger. Finding the right medical practice financing solutions is the secret to keeping your independence and helping more patients grow.

Forget the confusing, slow process at big banks. The world of money for doctors has totally changed. Now there are much smarter, easier ways for you to get the cash you need to succeed in the coming year, 2026.

Regular Bank Loans: The Old-School Way (But Slow!)

A standard loan from a local bank is usually the first thing doctors think of, especially if they have excellent credit and cash flow. These loans often give you the lowest interest rates, which is great for huge purchases like buying the actual building you work in.

But here’s the catch: be ready to wait a long time and fill out endless paperwork. Banks need tons of documents and often just don't understand the unique ways independent practices get paid by insurance.

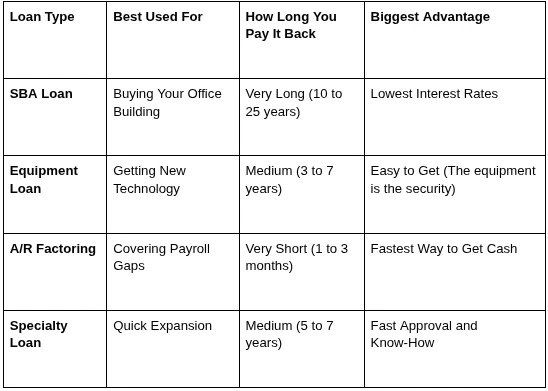

Specialty Medical Business Loans: The Fast Pass to Cash

Specialty lenders, like our team at National Medical Funding, only focus on the healthcare industry. This means they already understand things like insurance delays, medical billing cycles, and how expensive equipment can be. Because they "get it," they can approve your application much faster than a regular bank.

They offer flexible medical business loans perfect for things like expanding your waiting room or buying out another doctor's practice. Their speed and deep understanding make them the best choice when you need money quickly.

Equipment Financing: Get New Tools Without Paying Upfront

Need a new, modern ultrasound machine or want to update your patient records to a fancy digital system? Equipment financing lets you buy that new technology right now without touching the cash you use for daily operations. The equipment you buy acts as the security for the loan, which makes it easier to get approved.

For example, a children's doctor can use this to buy specialized examination tables and diagnostic tools. This financing is perfect for staying up-to-date and giving patients the advanced tools they expect.

Accounts Receivable (A/R) Financing: Turn Slow Payouts into Quick Money

Independent practices often have to wait two or three months for insurance companies to finally send their payments. A/R financing (or factoring) lets you sell those future insurance payments to a lender for immediate cash, minus a small service fee.

This is a fantastic option for bridging short-term gaps in your cash flow. If you suddenly have a big payroll due or need to buy extra supplies while waiting for a massive insurance payout, this solution gives you cash immediately.

SBA Loans: Government Help for Big Building Projects

The Small Business Administration (SBA) is a government agency that guarantees a portion of certain loans. This makes banks much more willing to lend you money for large projects like building an entirely new clinic. SBA 7(a) loans are excellent for buying the building your office is in or starting a brand-new practice location.

These loans come with low rates and very long repayment periods, sometimes up to 25 years. They are specifically helpful for securing healthcare facility loans when you need to construct, buy, or heavily renovate a major clinic space.

Business Credit Lines: Your Easy Financial Safety Net

A business line of credit works like a flexible credit card for your practice. You get approved for a maximum amount, and here's the best part: you only pay interest on the money you actually borrow. It's perfect for those unpredictable costs that pop up unexpectedly.

For instance, if your air conditioner breaks down suddenly in the middle of summer, or if you need to stock up on expensive flu vaccines right away, a credit line gives you instant access to cash without having to fill out a long application every single time.

Investor-Backed Loans: Private Money for Explosive Growth

If your practice has the potential for huge, fast growth—maybe you've developed a special new treatment or you are expanding very quickly—you might look at private investors or online lending groups. These groups offer capital in exchange for either a higher return or, sometimes, a small percentage of your future profits.

While these loans can be a little riskier, they are a very fast source of capital when the usual bank loans aren't working out. This is a great choice for a specialist who is opening a high-demand surgical center or a new cosmetic clinic.

What Lenders Care About: Your Practice's Report Card

Lenders always look closely at three main things: how healthy your cash flow is (money in versus money out), your history of paying bills (credit), and your collateral (what big assets you own). They need proof that your practice is stable and can easily handle the new medical practice loans.

To prepare, make sure all your financial records are perfectly clean and organized. Showing steady patient visits and consistent earnings is the absolute best way to get low rates and flexible terms.

Understanding Your Choices: A Simple Loan Comparison

When you are looking at different medical practice financing solutions, it helps to compare them side-by-side. The best choice for you depends completely on what you need—is it speed, low interest, or high flexibility?

Why Team Up with a Specialty Lender Like National Medical Funding?

Working with a dedicated partner like National Medical Funding is smart because they already speak the language of medicine. This saves you tons of time and stress. They immediately know the difference between a loan for daily running costs and a big healthcare facility loan for a new building.

Building a good relationship now means getting faster, easier financing later. When an emergency happens, having a lender who knows you can be the difference between solving the problem right away and facing huge delays.

Be Generous: Don't Underestimate How Much Money You Need

A common mistake doctors make is not asking for enough money for their project, especially when you think about unexpected delays or new regulations. You should always aim to secure more financing than you think the project will actually cost.

It is always better to have access to extra money and not need it than to suddenly run out of cash halfway through a crucial renovation. Accurate planning is vital when applying for any medical business loans.

Using Your Loan to Secure Your Future

The money you borrow should do more than just pay bills; it should help you grow. Use your new loan to invest in technology that makes your staff more efficient or in a new location that attracts patients who pay well.

Think about how this medical practice loan will help you reach your goals five years from now. By funding smart growth, you are protecting your independence and ensuring you stay profitable for the long term.

The Power of Good Financial Records

Remember how important those report cards were in school? Your financial records are your practice’s report card. Keep them neat, accurate, and up-to-date. This includes patient numbers, billing cycles, and tax returns.

Clean records speed up the approval process, proving to lenders that your practice is a low-risk, responsible investment. This makes specialty medical practice financing solutions easier to access.

Are You Ready to Take the Next Step?

Deciding to expand or upgrade is a huge, positive step for your practice. Don't let the complicated process of finding money slow you down. The variety of medical practice loans available in 2026 means there is a perfect option out there for whatever your goals are.

Figure out what you need most—a new building, faster money flow, or new equipment—and then choose the solution that gives you the best mix of speed, low cost, and flexibility.

A Quick Look at the Financial Landscape in 2026

The market for independent doctors is strong, and lenders want to invest in stable practices. This means competition among lenders is good for you! Take advantage of low rates and flexible products offered by specialty lenders who truly understand your worth.

By choosing the right partner, you can stop spending time worrying about finances and get back to focusing on what you do best: taking care of your patients.

FAQs

- Q: Can I use a medical business loan to pay off my college student loans?

- A: Generally no; business loans must be used for business expenses.

- Q: Are SBA loans always the cheapest option for doctors?

- A: They often have the lowest rates, but the application process is usually very long.

- Q: Does National Medical Funding finance healthcare facility loans?

- A: Yes, specialty lenders offer funding for buying or building any large medical property.

- Q: Is getting equipment financing easier than a general loan?

- A: Yes, because the equipment you buy acts as the security (collateral) for the loan.

Sign in to leave a comment.