For most retirees, tax free retirement is simply never part of the plan.

If your savings sit primarily in a 401(k) or traditional IRA, every dollar you withdraw is taxed as ordinary income. Add RMDs, Social Security taxation, and rising tax brackets, and a well-funded retirement can feel significantly smaller than expected.

The good news is that with the right plan, structure, and timing, you can build a retirement income strategy that reduces your annual tax burden and minimizes the taxes you pay to the IRS over a lifetime.

This guide walks through the most powerful tax free retirement investments available, how they work together as a coordinated system, and the specific decisions that determine whether your savings last 20 years or 35.

Whether you are five years from retirement or already drawing income, understanding tax free investments for retirement is one of the highest-leverage financial insights you can gain.

What Is Tax Free Retirement, And Why It Matters

Tax free retirement refers to a strategy where your wealth grows and is accessed without triggering ordinary income taxes. Rather than deferring taxes until withdrawal — as with a traditional 401(k) or IRA — tax free retirement investments are structured so that the growth, withdrawals, or both are shielded from taxation.

This matters more in today's environment than ever before. Modern retirees are living longer, facing shifting tax laws, and navigating a distribution phase that can span three decades or more. Without a deliberate structure, even a well-funded retirement can be quietly eroded by tax drag over time.

The Tax Trap Most Retirees Don't See Coming

Most people are surprised to learn that their tax bills don't drop significantly once they stop working. In many cases, they increase. Here's why:

Traditional retirement accounts create a tax time bomb.

Every dollar withdrawn from a 401(k) or traditional IRA is taxed as ordinary income — at whatever rate applies in the year you take it. If you've accumulated significant savings in these accounts, your distributions in retirement can push you into higher tax brackets than you experienced during your working years.

Social Security benefits can become partially taxable.

The IRS uses a figure called "provisional income" — a combination of your adjusted gross income, nontaxable interest, and half of your Social Security benefit — to determine how much of your benefit is taxable. If provisional income exceeds $25,000 for individuals or $32,000 for couples, up to 85% of your Social Security benefit can become subject to federal income tax.

RMDs eliminate your control over the timing.

Once you reach age 73, the IRS requires you to begin taking Required Minimum Distributions from traditional retirement accounts, whether you need the income or not. These mandatory withdrawals increase your taxable income each year, often triggering taxation on Social Security benefits you would otherwise have kept tax-free.

Without a plan built around tax free retirement investments, these three forces compound against each other — reducing your spendable income year after year throughout retirement.

Why Tax Management Is Now a Core Retirement Skill

A generation ago, retirees could reasonably expect to draw down savings over 15 to 20 years. Today, a couple retiring at 65 has a meaningful probability that at least one partner will live into their late eighties or beyond. That's a 30+ year retirement — and 30 years of compounding tax drag is a fundamentally different problem than 15.

Tax laws also shift. What is deductible or advantaged today may not be the same in a decade. Building a tax free retirement plan that relies on a single strategy or account type leaves you exposed to exactly that kind of legislative change.

The retirees who are best positioned are those who diversify not just their investments — but their tax treatment. Taxable accounts, tax-deferred accounts, and tax free accounts each respond differently to changes in rates and rules. Holding all three gives you options. Holding only one eliminates them.

A Guide to Tax Free Investments for Retirement

There are five primary vehicles through which tax free investments for retirement are structured. Each has a different mechanism, different contribution rules, and a different role within a complete retirement plan. Used together, they form the foundation of a genuinely tax-efficient retirement.

Roth IRA: The Foundation of Tax Free Retirement

The Roth IRA is the most well-known of all tax free retirement investments — and for good reason. Contributions are made with after-tax dollars, meaning you pay taxes on the money before it goes in. From that point forward:

- Your investments grow completely tax-free inside the account

- Qualified withdrawals in retirement (after age 59½, from an account open at least five years) are 100% tax-free

- There are no Required Minimum Distributions during your lifetime, meaning the account can continue growing tax-free indefinitely, or pass to your heirs intact

Direct Roth IRA contributions are available to most earners, though the ability to contribute phases out at higher income levels, your financial advisor or tax professional can confirm whether you qualify based on your current income.

The real power of a Roth IRA within a tax free retirement strategy is flexibility. Because Roth withdrawals don't count as provisional income, they don't trigger Social Security taxation, don't push you into higher brackets, and don't factor into Medicare IRMAA premium calculations, a critical advantage later in retirement.

Backdoor Roth IRA: For High Earners Who Exceed Income Limits

For individuals and couples whose income exceeds the direct contribution thresholds, the Backdoor Roth IRA provides a fully legal pathway to the same benefits.

The process works in two steps:

- Make a nondeductible contribution to a traditional IRA (anyone can do this, regardless of income)

- Convert that contribution to a Roth IRA, typically shortly after the contribution is made

Because you've already paid taxes on the contribution, the conversion itself is generally tax-free (assuming no other pre-tax IRA balances exist). Growth after conversion accumulates tax-free, and qualified withdrawals in retirement carry no tax liability.

One important caveat: if you hold other pre-tax IRA balances, the IRS's pro-rata rule will require you to calculate taxes across all IRA assets rather than just the newly contributed amount. Working with a tax-aware financial advisor before executing a backdoor Roth conversion is strongly recommended to avoid unexpected tax bills.

Roth 401(k): Employer-Sponsored Tax Free Growth

The Roth 401(k) brings the tax free growth mechanics of a Roth IRA into the employer-sponsored plan structure. Like the Roth IRA, contributions are made with after-tax dollars and qualified withdrawals are tax-free. However, there are two important distinctions:

There are no income limits

To contribute to a Roth 401(k), making it accessible to high earners who can't directly contribute to a Roth IRA

Roth 401(k)

If your employer offers a Roth 401(k) option, maximizing it alongside a Roth IRA can create a powerful two-account tax free retirement investment base where contribution limits are meaningfully higher than a Roth IRA alone. Your advisor can confirm current limits based on your age and plan

Cash Value Life Insurance: Tax Advantaged Savings Without Contribution Limits

Permanent life insurance policies with a cash value component, such as whole life or indexed universal life, can function as a significant source of tax free retirement income when structured properly. While they are frequently overlooked in retirement planning conversations, their advantages are substantial for high earners who have maxed out other tax-advantaged options:

- The cash value inside the policy grows on a tax-deferred basis

- You can access the cash value through policy loans that are not considered taxable income by the IRS

- Death benefits pass to beneficiaries income tax-free

- Unlike Roth IRAs and 401(k)s, there are no IRS contribution limits — making these policies an important overflow vehicle for those who want additional tax-sheltered growth

Cash value life insurance can play a role in a broader tax strategy for certain clients, but like any complex product, it requires objective, fiduciary evaluation to determine whether it genuinely fits your plan or simply adds cost and complexity

Municipal Bonds: Tax Free Income After Retirement

Municipal bonds, debt obligations issued by state and local governments, offer interest income that is exempt from federal income tax. In many cases, interest from bonds issued within your home state is also exempt from state income tax, creating a fully tax-free income stream.

For retirees in higher tax brackets, the after-tax equivalent yield of a municipal bond can significantly outperform taxable bonds of comparable credit quality. They are generally lower-volatility than equities, making them a natural fit for the stability-focused portion of a retirement portfolio.

Municipal bonds are a particularly effective vehicle for tax free investments after retirement because they generate regular income without adding to your adjusted gross income, helping to keep provisional income below Social Security taxation thresholds and IRMAA premium triggers.

How Tax Free Retirement Investments Work Together

Owning tax free retirement investments in isolation is only a component of your strategy. What separates a plan that preserves wealth over 30 years from one that doesn't is how these vehicles are coordinated with each other, with your taxable and tax-deferred accounts, and with the timing of other income sources.

The framework most retirement planners use to visualize this is the Three-Bucket System:

| Bucket | Account Type | Tax Treatment |

| Bucket 1 | Taxable accounts (brokerage, savings) | Taxed on gains and dividends annually |

| Bucket 2 | Tax-deferred accounts (401(k), traditional IRA) | Taxed upon withdrawal as ordinary income |

| Bucket 3 | Tax free accounts (Roth IRA, Roth 401(k), cash value life insurance) | Not taxed on qualified withdrawals |

The goal of a well-structured tax free retirement plan is to have meaningful assets in all three buckets — giving you the flexibility to draw from whichever source minimizes your tax exposure in any given year.

The Withdrawal Sequence That Protects Long-Term Savings

Most retirees assume they should draw down their taxable accounts first, then tap tax-deferred accounts, and leave tax free accounts untouched for as long as possible. As a general framework, this is directionally correct — but the execution matters enormously.

The conventional withdrawal sequence looks like this:

- First: Taxable accounts: Spend down brokerage accounts and savings first. Gains here are taxed at more favorable long-term capital gains rates, and depleting these accounts early preserves the tax-advantaged growth in buckets two and three.

- Middle: Tax-deferred accounts: Draw from 401(k)s and traditional IRAs in the middle years of retirement, ideally in amounts that keep you from jumping into higher brackets

- Last: Tax free accounts: Preserve Roth accounts for as long as possible to maximize tax-free growth and provide a buffer against future tax changes.

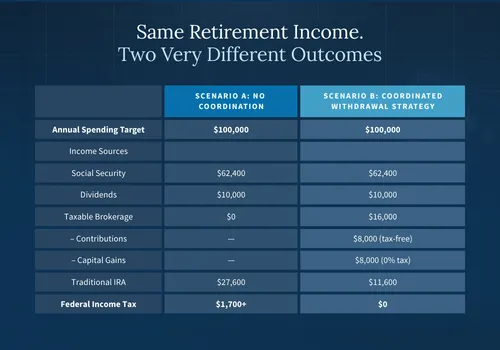

However, strictly following this sequence without adjustment can lead to large, forced taxable events when RMDs kick in. A more sophisticated approach blends income sources across all three buckets each year to actively manage your annual taxable income, keeping you in lower brackets, minimizing Social Security taxation, and avoiding Medicare premium surcharges.

Roth Conversion Windows: A Critical, Time-Sensitive Opportunity

One of the most powerful and time-sensitive tax free retirement strategies is the Roth conversion, converting assets from a traditional IRA or 401(k) into a Roth IRA during a period of relatively low taxable income.

The optimal window for most retirees is the period between retirement and age 73, when RMDs begin. During this window:

- Earned income has stopped or dropped significantly, often creating a lower effective tax bracket

- RMDs have not yet started, so taxable income is at its lowest point in decades

- Social Security may not yet be claimed, reducing provisional income further

Converting pre-tax assets during this window — even at a modest tax cost — can dramatically reduce future RMD obligations, lower lifetime tax drag, and increase the portion of your retirement income that is permanently tax-free.

Every year you delay past retirement without utilizing the Roth conversion window is a planning opportunity that closes. Once RMDs begin and Social Security starts, the calculation becomes significantly less favorable.

Coordinating Social Security With Your Tax Free Strategy

Social Security timing is a tax decision. Delaying Social Security to age 70 (to maximize the monthly benefit) while simultaneously executing Roth conversions in the years prior can be a highly effective combination:

- Delayed claiming reduces provisional income during the conversion years, allowing you to convert more assets at lower tax rates

- A larger Social Security benefit, when it does begin, often comes with a higher percentage being tax-free, because a well-structured Roth-heavy portfolio reduces provisional income in those years

- Roth distributions don't count toward the IRS's provisional income calculation at all, meaning even substantial retirement income from Roth accounts doesn't trigger taxation of your Social Security benefit

This interaction between account type, Social Security timing, and provisional income is one of the most complex, and most impactful, areas of retirement tax planning. It requires multi-year projection modeling, not a one-year tax return.

Best Tax Free Investments for Retirement by Financial Goal

Not every tax free retirement investment is the right fit for every person. The right vehicle depends on your income level, timeline, existing account balances, and estate planning priorities. Here's a quick-reference comparison:

| Vehicle | Best For | Key Advantage |

| Roth IRA | Most earners within income limits | Tax-free growth + no RMDs |

| Backdoor Roth IRA | High earners above Roth income limits | Full Roth access regardless of income |

| Roth 401(k) | Earners with employer plan access | High contribution limits + no income ceiling |

| Cash Value Life Insurance | High earners needing overflow tax shelter | No contribution limits + estate planning |

| Municipal Bonds | Stability-focused retirees | Tax-free income without adding to provisional income |

A genuinely tax-optimized retirement plan typically incorporates more than one of these. The combination that works best for you depends on a coordinated analysis of your full financial picture, current accounts, projected income, Social Security timing, estate goals, and tax bracket trajectory over the next 20 to 30 years.

Tax Free Investments After Retirement: Managing What You've Already Built

Much of the conversation around tax free investments for retirement focuses on the accumulation phase, what to invest in during your working years. But the distribution phase is where these decisions actually pay off, and it requires a distinct set of strategies.

How to Draw Down Tax Free Accounts Without Triggering Unnecessary Taxes

The goal of tax free investments after retirement is not simply to avoid taxes in any single year. It's to manage your total taxable income across every year of retirement, keeping income low enough to minimize Social Security taxation, stay in lower brackets, and avoid IRMAA surcharges while still funding your lifestyle.

In practice, this means:

- Blending income sources annually rather than drawing exclusively from one bucket

- Monitoring provisional income each year and limiting taxable withdrawals to stay below key Social Security thresholds

- Using Roth distributions strategically to fill in income needs without adding to your adjusted gross income

- Using policy loans from cash value life insurance as a tax-free supplemental income source that doesn't appear on your tax return at all

This annual income-blending approach is what separates a reactive withdrawal strategy from a proactive one, and the difference in lifetime tax savings can be measured in six figures or more over a 30-year retirement.

Medicare IRMAA and Income Thresholds

Most retirees don't realize that their Medicare Part B and Part D premiums are income-dependent. The Income-Related Monthly Adjustment Amount (IRMAA) adds surcharges to Medicare premiums once your modified adjusted gross income exceeds certain thresholds, thresholds the IRS adjusts annually. The higher your income, the higher your premiums.

Here's the critical tax planning advantage: Roth IRA withdrawals and life insurance policy loans do not count toward MAGI. This means that strategic use of tax free retirement income sources, rather than taxable IRA withdrawals, can keep you below IRMAA surcharge thresholds and save thousands of dollars annually in Medicare premiums, year after year.

This is not a marginal consideration. For a retiree in the first IRMAA tier, the surcharge adds over $800 per person per year. In higher tiers, the premium difference exceeds $3,000 per person annually. Over a decade or more of retirement, this is a material amount of wealth preserved through intelligent tax free income sequencing.

Multi-Year Tax Projections: The Strategy Most Advisors Skip

The vast majority of financial advisors review your tax situation once per year — typically through the lens of last year's return. This reactive approach captures what happened. It doesn't optimize what's coming.

A genuine multi-year tax projection looks forward across every year of your expected retirement. It models:

- When RMDs begin and what they'll force onto your tax return

- Which years offer optimal Roth conversion opportunities before those RMDs start

- How Social Security timing interacts with your provisional income at each point on the timeline

- What IRMAA thresholds you'll cross in different income scenarios

- How inflation and rising costs affect the real purchasing power of your tax savings

This level of planning requires a team with both financial planning expertise and tax strategy depth. It's the difference between a plan that looks good on paper and one that actually protects your cash flow over 30 years.

How to Build a Tax Free Retirement Plan That Lasts 30+ Years

A tax free retirement planning is not a single account decision. It is a coordinated system — one where income mapping, Roth conversions, Social Security timing, withdrawal sequencing, and investment selection work together as a unified strategy.

The elements of a durable plan include:

Income mapping

That shows exactly where every dollar of retirement income will come from — year by year — across Social Security, portfolio withdrawals, pensions, and cash-flow reserves.

A Roth conversion strategy

Built around the pre-RMD window, designed to reduce future tax-deferred account balances and shift more of your wealth into permanently tax-free territory before mandatory distributions begin.

A withdrawal sequence

That coordinates taxable, tax-deferred, and tax free accounts with timing decisions that reduce early-retirement vulnerability and extend portfolio longevity across decades.

Social Security optimization

That accounts for provisional income, benefit taxation thresholds, and the interaction between claiming age and your overall tax free retirement strategy.

Ongoing tax projection and monitoring

Not just an annual tax return review, but a multi-year model that identifies opportunities and threats well in advance.

The window to build and execute this plan is not open indefinitely. Roth conversion windows narrow as RMD age approaches. Tax brackets shift as income sources change. Social Security timing options close once you've claimed. Portfolio risk becomes harder to adjust as retirement deepens.

The earlier a coordinated tax free retirement plan is in place, the more control you retain over the outcome.

Make Your Tax Strategy Work for You

A tax free retirement is the result of deliberate decisions, made early, coordinated across accounts, and updated as your life changes. The window to act is open now. Roth conversion opportunities narrow. RMDs begin. Social Security timing options close.

The earlier a coordinated plan is in place, the more of your retirement you get to keep.

If you're ready to see how income, taxes, and withdrawals can work together for your specific situation, Seaside Wealth Management is here to help. Schedule a free introductory call.

Frequently Asked Questions

What is the best way to avoid taxes in retirement?

The most effective way to minimize taxes in retirement is to diversify your retirement assets across three types of accounts: taxable accounts (like brokerage accounts), tax-deferred accounts (like traditional IRAs and 401(k)s), and tax free accounts (like Roth IRAs and cash value life insurance). From there, the key strategies are: executing Roth conversions during the window between retirement and RMD age (73), sequencing withdrawals intelligently to avoid bracket creep, managing provisional income to limit Social Security taxation, and using tax free income sources like Roth distributions to stay below Medicare IRMAA thresholds. No single move eliminates all taxes in retirement — but a coordinated, multi-year plan manages them with precision.

How much can you take tax-free on retirement?

There is no single dollar limit on how much income you can receive tax-free in retirement — it depends on your account types and income structure. Qualified Roth IRA withdrawals are entirely tax-free with no dollar ceiling. Policy loans from cash value life insurance are also not subject to income tax regardless of amount. Municipal bond interest is federally tax-exempt (and often state-exempt). The real constraint is not a legal cap on tax-free income — it's how much of your retirement wealth has been positioned in tax-free vehicles before distributions begin. This is why front-loading Roth contributions and executing strategic Roth conversions during your working years and early retirement window has such a significant long-term impact.

How much tax will I pay if I am retired?

Retired individuals are taxed on their ordinary income just like working individuals — the same federal brackets apply. However, what counts as "income" in retirement depends heavily on your account types. Traditional IRA and 401(k) withdrawals are taxed as ordinary income. Social Security benefits may be 0%, 50%, or up to 85% taxable depending on your provisional income.

Capital gains from taxable accounts are taxed at preferential long-term rates. Roth IRA qualified withdrawals and life insurance policy loans are not counted as income at all.

A retiree with a well-structured tax free retirement plan — drawing primarily from Roth accounts and managing provisional income carefully — may pay very little in federal income tax despite a comfortable standard of living.

Sign in to leave a comment.