When students start exploring education loans, most of them ask the wrong question:

“Can I get a loan without collateral?”

But the smarter question is:

“Which education loan structure actually fits my course, family situation, and future income?”

Because choosing between a secured (collateral) loan and an unsecured (no-collateral) loan isn’t about convenience — it’s about your long-term financial health.

Let’s simplify this in a way that actually helps you make a confident decision.

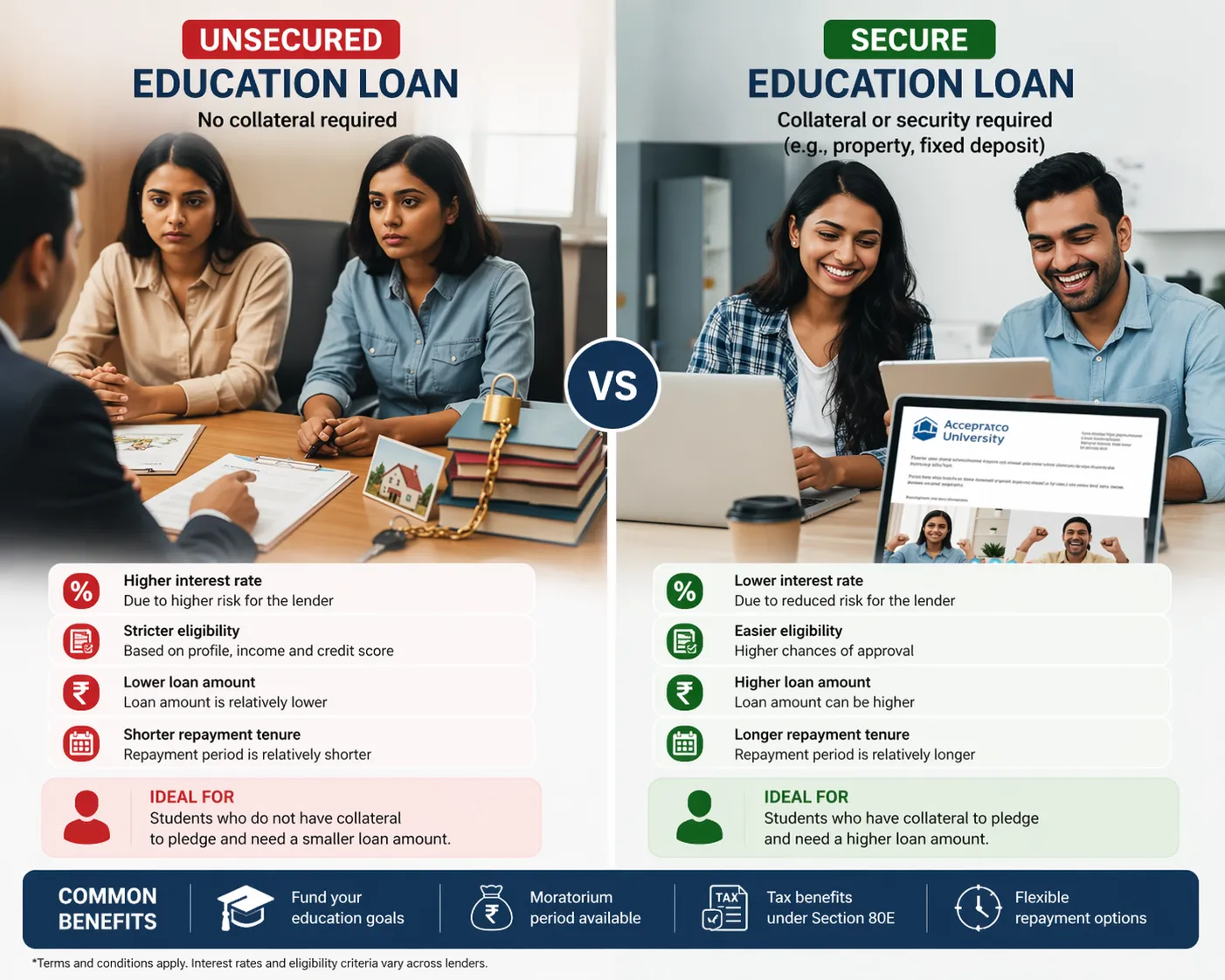

What Is a Secured (Collateral) Education Loan?

A secured education loan is backed by an asset. This gives the lender security and reduces their risk.

Common collateral options include: Residential property

Residential land Fixed deposits Insurance policies (accepted in some cases) Why banks prefer secured loans:

Because there’s security involved, you typically get:

Lower interest rates Higher loan amounts Longer repayment tenure

In simple terms: less pressure on your future income

What Is an Unsecured (No-Collateral) Education Loan?

An unsecured education loan does not require any assets. Approval depends entirely on your profile.

Banks evaluate: Student academic profile Course and university Country of study Co-applicant’s income and credit score Trade-offs you should know: Higher interest rates Lower loan limits Strict eligibility criteria

In simple terms: faster access, but higher long-term cost

The Biggest Myth About Education Loans

Many students believe:

“Unsecured loans are always better.”

That’s not entirely true.

They are easier, not always smarter. They shift the financial burden to your future earnings Over time, they can cost ₹5–10 lakhs more

Convenience today can become financial pressure tomorrow.

Key Factors to Decide the Right Loan Structure

1. Total Cost of Education

Your total budget plays a major role.

₹20–30 lakhs → Unsecured loan may be sufficient ₹40–80 lakhs → Secured loan is usually more practical

Why?

Unsecured loans often don’t cover the full amount, forcing families to arrange funds from multiple sources.

2. Course & Future Earning Potential

Banks don’t fund dreams — they assess return on investment (ROI).

High-ROI courses (STEM, MBA) → Better chances for unsecured loans Niche or moderate ROI courses → Secured loans improve approval chances and reduce interest rates

The stronger your earning potential, the less security banks demand.

3. Interest Rates (The Silent Wealth Killer)

Even a small difference matters.

A 1–2% higher interest rate can lead to ₹5–10 lakhs extra repayment over time Higher EMIs during early career years

Secured loans often win in the long run — even if they involve more paperwork.

4. Family Asset Situation

Ask these questions honestly:

Is the property loan-free? Are ownership documents clear and complete? Is the asset legally mortgageable?

If yes, not using it may be financially inefficient.

But avoid collateral if:

Ownership is disputed Documents are unclear Family has a plan for the asset

In such cases, an unsecured loan is safer — even if costlier.

5. Emotional & Psychological Impact

This is often ignored — but extremely important.

Secured Loans: Lower EMI pressure Longer repayment flexibility Financial stability Unsecured Loans: No emotional stress of pledging property But higher repayment pressure after graduation

Choose the option that helps you focus on your studies — not stress about EMIs.

6. Visa & Approval Advantage

Many students don’t realize this:

Secured loans can: Strengthen visa documentation Improve bank approval chances Support higher loan amounts Unsecured loans require: Strong profile alignment Correct lender selection Accurate documentation

One wrong bank choice can lead to delays or rejection.

It’s not just about interest rates or collateral.

Most problems happen due to:

Choosing the wrong bank Poor loan structuring Lack of proper guidance

A rushed decision today can impact your finances for the next 10–15 years.

Final Thoughts

The goal of an education loan is simple:

To support your growth — not create financial stress.

There is no one-size-fits-all answer.

The right loan structure is the one that:

Protects your family Aligns with your career path Keeps your future financially secure

Because when planned correctly, Both secured and unsecured loans can work beautifully.

Sign in to leave a comment.