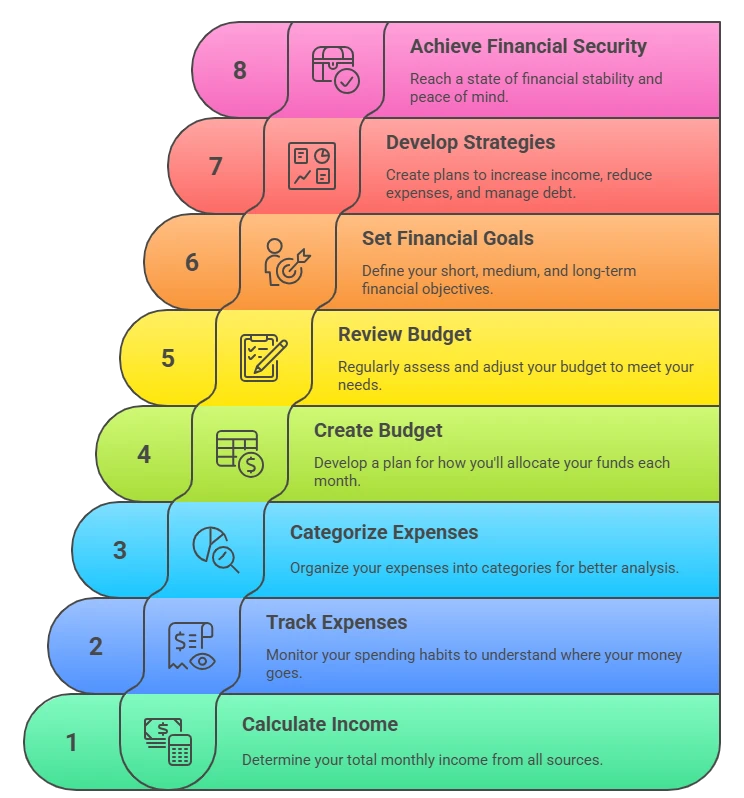

Setting clear and achievable financial goals is one of the most effective ways to take control of your money and build a secure future. Financial goal setting is more than just saving money—it's about having a defined plan for your income, expenses, savings, and investments. Whether you want to buy a home, retire early, pay off debt, or build an emergency fund, setting realistic money goals is the first step toward long-term financial success planning.

Understanding how to set financial goals can dramatically improve your ability to manage your finances, stay motivated, and track your progress. By applying structured frameworks like SMART goals and leveraging money management strategies, individuals can gain clarity, confidence, and momentum in their financial journey.

Why Financial Goal Setting Matters

Financial goal setting brings structure and direction to your financial life. It reduces stress and helps prioritize spending. People who engage in goal setting tend to have stronger financial discipline, improved financial literacy, and greater control over their economic security. When you define your financial priorities, it becomes easier to avoid impulse spending and focus on what truly matters.

Additionally, setting goals boosts motivation. Each milestone achieved, whether it's saving $500 or clearing a credit card balance, reinforces positive financial behaviors and builds momentum for bigger wins.

Types of Financial Goals You Should Set

Financial goals can be categorized into three main types: short-term, medium-term, and long-term. Understanding the differences allows you to create a balanced and realistic financial roadmap.

Short-Term Financial Goals

Short-term goals are those you aim to achieve within a year. Common examples include building a basic emergency fund, creating a spending plan, or paying off a small credit card balance. These goals lay the foundation for better money habits and provide quick wins that build confidence.

Medium-Term Financial Goals

These are goals you plan to achieve in one to five years. Examples include saving for a car, a down payment on a home, or a wedding. Having a savings plan and sticking to a budgeting routine are critical to achieving these financial priorities.

Long-Term Financial Goals

Long-term goals often involve investment planning, retirement goals, or paying off a mortgage. These require discipline, consistent savings, and a solid understanding of net worth tracking. By focusing on long-term financial planning, individuals can secure their future and gain peace of mind.

How to Set SMART Financial Goals

SMART goals are Specific, Measurable, Achievable, Relevant, and Time-bound. This method provides a structured way to set and evaluate your personal finance targets.

- Specific: Define what you want to accomplish (e.g., Save $10,000 for a down payment).

- Measurable: Track your progress and milestones.

- Achievable: Make sure it's realistic based on your income and expenses.

- Relevant: Align with your broader financial priorities.

- Time-bound: Set a deadline (e.g., within 12 months).

Using the SMART framework ensures that your goals aren't vague and that you have a roadmap for execution and success.

Budgeting and Planning for Financial Goals

Once your goals are defined, the next step is to support them with a solid budgeting for financial goals strategy. Budgeting allows you to allocate income effectively and identify areas to cut back on spending. This enables consistent contributions toward your goals, whether they're short- or long-term.

Creating a budget aligned with your financial goal setting process helps balance your income vs expenses and avoid debt accumulation. Use spreadsheets, budgeting apps, or financial planning software to stay organized and make adjustments as needed.

Overcoming Common Barriers to Financial Goal Setting

Many people struggle with financial goal setting due to lack of motivation, poor habits, or overwhelming debt. Common barriers include living paycheck to paycheck, emotional spending, or uncertainty about where to begin.

To overcome these challenges, start small. Begin with one manageable goal, like building a $1,000 emergency fund or creating a monthly spending plan. Celebrate progress and use positive reinforcement to build better money management strategies.

Tools and Apps to Help You Stay on Track

Technology can be a powerful ally in your financial goal setting journey. Popular tools include:

- Mint and YNAB (You Need A Budget): Great for daily expense tracking and budgeting.

- Personal Capital: Helps with net worth tracking and investment planning.

- CheckBoost: Optimizes taxes and increases available income for savings goals.

These tools support financial literacy by providing clear visuals, tracking features, and automated reminders.

How to Track Financial Progress Over Time

Tracking your progress is essential to staying motivated and adjusting as needed. Review your goals monthly or quarterly. Ask yourself:

- Am I on track?

- Are my contributions consistent?

- Do I need to adjust deadlines or amounts?

By regularly assessing your progress, you can make smarter decisions and refine your approach. This habit is vital for successful long-term financial planning.

Final Thoughts on Financial Goal Setting

Effective financial goal setting is a lifelong skill that empowers you to make intentional decisions with your money. From short-term wins to long-term vision, setting SMART goals, budgeting wisely, and tracking progress are foundational to building wealth and achieving security.

By defining your financial priorities, practicing financial discipline, and leveraging the right tools, you can create a personalized roadmap to success. Start small, stay consistent, and watch your efforts compound over time into meaningful financial freedom.

Sign in to leave a comment.