Hey, entrepreneurs! When your business is ready to grow, finding the right cash is crucial. You might have heard about traditional Term Loans, but there's a modern powerhouse gaining serious traction: Revenue-Based Financing (RBF). Choosing between the two means deciding how much risk, speed, and flexibility you need.

This choice is huge because it impacts your daily cash flow and future growth potential. We’re diving deep to compare these two powerful financial tools. We will explore why RBF often provides far more agility, making it the preferred choice for businesses looking for same day business funding without the rigid demands of a bank.

Term Loans: The Traditional, Fixed Way 🏦

A traditional Term Loan is what most people picture when they think of business borrowing. A bank or lender gives you a fixed lump sum of cash up front, and you agree to pay it back over a set period—the term—with regular, fixed monthly payments.

Therefore, this model requires consistency. Every month, rain or shine, success or slow season, you owe the same principal and interest payment. This structure works well for businesses with highly predictable, stable revenues, but it can be devastating for companies dealing with seasonal dips.

Defining RBF: Flexibility in Repayment 💡

Revenue-based business loans (RBF) turn the lending model on its head. Instead of a fixed monthly payment, the advance is repaid using a small, agreed-upon percentage of your daily or weekly sales. It's truly financing that moves at the speed of your business.

This is critical because when your sales are up, you pay down the advance faster. When sales dip (say, during January if you're a retail store), your actual payment automatically drops, protecting your vital working capital and preventing cash flow crises.

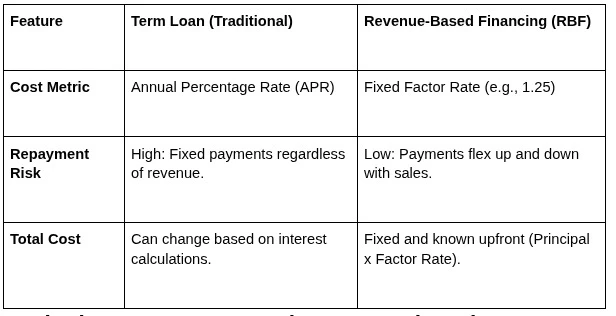

Cost Comparison: APR vs. Factor Rate 💰

The cost structure is the biggest difference between the two products. Term Loans use an Annual Percentage Rate (APR), which compounds interest over time. This can make the total cost seem lower initially, but the fixed repayment schedule adds pressure.

Conversely, RBF uses a Factor Rate—a fixed multiplier. If you borrow $100,000 at a 1.25 Factor Rate, your total repayment is a fixed $125,000. That cost ($25,000) does not change, regardless of whether you repay it in six months or twelve months.

Comparing Loan Cost Structures

Cash Flow Management: The Seasonal Business Story 🌊

Let's imagine you own a landscaping company. Your peak season is spring and summer; your slow season is winter. A Term Loan requires a $5,000 payment in December, even if your revenue is only $15,000. That’s a massive 33% hit to cash flow.

However, RBF payment flexibility shines here. If your contract states a 10% retrieval rate, and your December revenue is $15,000, your payment is only $1,500. This adaptive structure ensures you retain more working capital when you need it most.

The Speed Factor: Why RBF Offers Same Day Business Funding ⚡

When you need capital for a sudden opportunity—like acquiring inventory at a huge discount—timing is everything. Traditional Term Loans require extensive underwriting, collateral appraisal, and committee approval, often taking weeks or even months.

In stark contrast, RBF providers focus entirely on your cash flow data (bank statements and sales history). Because they don't need to value collateral, they can approve your application and often deliver same day business funding, turning a fleeting opportunity into immediate profit.

The Risk Factor: Collateral and Personal Guarantees 🛡️

Term Loans are usually secured, demanding fixed collateral like real estate or heavy equipment. If your business defaults, the bank has the right to seize those assets. Furthermore, many traditional lenders require a personal guarantee, putting your home or savings at risk.

Conversely, RBF is generally unsecured. Lenders rely on the strength and consistency of your revenue stream. This means you avoid placing liens on your business assets or risking your personal finances, making RBF a lower-risk option for personal liability.

Understanding BCAs and the Merchant Cash Advance Calculator 🧮

A Business Cash Advance (BCA) is a common form of revenue based business loans. It works exactly like RBF, but it’s specifically focused on high-volume, short-term funding needs. This is where tools become invaluable.

Before signing any agreement, you need clarity on costs. An online merchant cash advance calculator allows you to input the advance amount and the Factor Rate to instantly project your total repayment amount. This transparency ensures you make a fully informed decision about your financing.

Resources for Further Clarity

If you need to understand the nuances of this specific type of funding, we have a detailed resource that explains all the terms: What Is a Business Cash Advance? Costs, Terms & How It Works. This tool is essential for anyone considering flexible financing options.

The Approval Hurdle: Credit Score vs. Cash Flow 💳

Traditional Term Loans place immense weight on your business's and owner’s credit score. A less-than-perfect score can immediately disqualify you, regardless of how strong your sales are today.

RBF providers, however, prioritize cash flow consistency over a perfect credit history. If you have been operating for a minimum of 6 months and have steady, predictable revenue, you are likely eligible. This focus democratizes funding access for growing businesses that might have faced past financial challenges.

Ideal Use Cases: RBF vs. Term Loan 🎯

When should you use which product? A Term Loan is best for large, long-term capital investments that generate slow, steady returns, such as purchasing commercial real estate or expensive production machinery.

Alternatively, RBF is perfectly suited for opportunities requiring speed and flexibility. This includes purchasing seasonal inventory, funding a sudden marketing push, covering an unexpected repair, or bridging temporary cash flow gaps.

The Bigger Picture: Why RBF Is Rising 🚀

The rise of revenue based business loans is part of a larger market correction. Traditional banks are fundamentally failing to meet the financing needs of modern, dynamic small businesses—especially those that are asset-light or highly seasonal.

The reality is that banks are too risk-averse and structurally rigid to serve the innovative SMB market effectively. For a deeper understanding of why this gap exists, you can read our guide: Why Banks are Failing SMBs and Revenue-Based Funding is Rising.

Choose Agility and Control 🏁

For the savvy small business owner, the choice between RBF and a Term Loan often comes down to control and agility. While the Term Loan offers a fixed cost (APR), RBF offers a flexible payment schedule that aligns perfectly with the unpredictable nature of running a business.

Ultimately, RBF ensures that your debt doesn't become a burden when business is slow, while also offering the same day business funding needed to seize profitable opportunities instantly. Embrace the financing that moves at your speed!

FAQs on RBF and Term Loans

- Q: Is RBF an interest-bearing loan?

- A: No, it is a fee calculated via a fixed Factor Rate, not compounding interest.

- Q: Do I need collateral for RBF?

- A: No, revenue based business loans are typically unsecured.

- Q: Which option is faster?

- A: RBF is significantly faster, often providing same day business funding.

- Q: How can I calculate the RBF daily payment?

- A: Use a merchant cash advance calculator with your Factor Rate and average sales.

- Q: When should I choose a Term Loan?

- A: For purchasing long-term assets like real estate or large equipment.

- Q: Can my credit score stop an RBF application?

- A: Rarely; cash flow consistency is far more important to RBF lenders.

Sign in to leave a comment.