Restricted stock loans can play an important role for home buyers who hold equity compensation, especially those considering a new home in high-cost housing markets.

Many tech employees receive restricted stock units as part of their compensation package, yet few understand how these shares can support a home purchase. When used correctly, RSUs can give buyers access to liquidity without being forced to sell stock or wait years to save cash.

This article explains how RSUs work, why lenders consider them differently from other assets, and how they connect to financing strategies that help buyers move sooner.

The foundation of any RSU-based strategy starts with understanding what an RSU is.

RSUs are a promise from an employer to deliver company shares in the future once certain conditions are met. These conditions usually include staying employed for a set period or meeting performance goals. Because RSUs are tied to company stock, their value changes with market conditions, which affects how useful they are when buyers explore restricted stock loans.

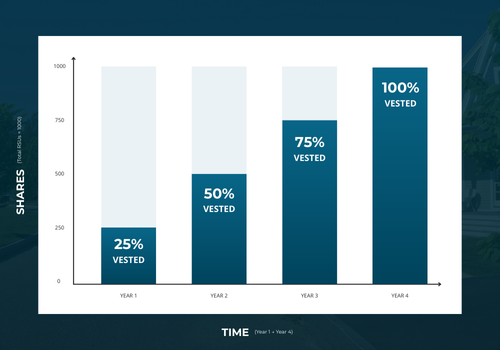

Every RSU grant follows a vesting schedule, and this schedule determines when you legally own the shares. Unvested shares cannot be sold or pledged, which limits liquidity. Once shares vest, they become yours and are typically taxed as ordinary income at that time.

This vesting process directly affects how much collateral you have available when applying for financing or preparing for mortgage pre-approval. Buyers who understand their vesting timeline can make clearer and more informed decisions about when to apply for a loan.

RSUs differ from regular stock options in several important ways.

Stock options give employees the right to buy shares at a set strike price. RSUs require no purchase and convert directly into shares at vesting.

This difference matters for homebuyers because RSUs carry more predictable value. That predictability makes them stronger candidates for use in restricted stock loans, where lenders rely on vested shares to determine how much liquidity they can issue.

How Lenders Evaluate RSUs When Assessing Borrowing Capacity

Lenders approach RSU-backed financing with careful analysis because the value of vested stock can rise or fall with market conditions.

When buyers include restricted stock loans in their assets, lenders need to understand both the strength of the collateral and the stability of the borrower. This evaluation determines how much a lender is willing to offer and what loan structure makes sense. RSUs can support borrowing power, but lenders follow specific guidelines to manage risk.

What Lenders Look For

Lenders review several parts of the borrower’s financial profile. They look at credit strength, employment stability, and the overall mix of income sources as part of the process for deciding whether the borrower can manage future payments even if markets change.

Part of this consideration includes access to restricted stock loans and the outcomes of that analysis influences how easily a buyer can secure mortgage pre-approval.

Borrower Profile

As you’re no doubt aware, lenders review credit scores, job stability, and past borrowing behavior. This helps them understand how reliable a borrower will be over the full term of the loan.

Income Consistency

Stable income helps offset the volatility of RSU values. Lenders look for predictable earnings and consistent year-over-year income patterns.

Existing Debt and Job History

Lenders review current obligations and employment length. Strong work history supports the case for using RSUs as collateral.

These factors work together to show whether a borrower can manage payments while using stock-backed collateral.

Loan-to-Value Limits for RSU-Based Loans

Loan-to-value limits define how much a borrower can access through restricted stock loans.

Because stock prices move with market conditions, lenders lend only a portion of the vested value. This limit protects lenders while still giving buyers access to needed liquidity. The final LTV depends on the borrower’s credit profile and the lender’s risk guidelines.

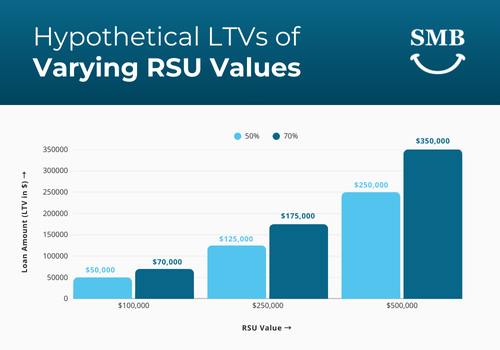

Typical LTV Ranges (50%–70%)

Most lenders offer between 50% and 70% of vested RSU value. Borrowers with stronger credit profiles may receive higher limits.

Why Lenders Discount RSU Value

RSUs fluctuate with the stock market. Lenders discount the value to protect against sudden price drops.

This structure ensures a safe balance between available liquidity and risk protection.

RSUs and Jumbo Loan Considerations

Jumbo loans matter in cities with higher home prices. And Seattle is definitely one of those markets.

Buyers relying on RSUs often explore jumbo loans because standard loan limits do not cover many local home prices. Lenders review RSUs differently in this context because larger loans require stricter guidelines.

Why Jumbo Loans Matter in Seattle

Home prices often exceed standard limits. Jumbo loans help buyers access the funding needed in a competitive environment.

Stricter Underwriting Requirements

Jumbo loan lenders require stronger credit, steady income, and reliable RSU documentation. These requirements help lenders manage risk on larger loan amounts.

Jumbo loan rules make preparation essential when combining RSUs with traditional mortgage financing.

Documentation Needed for RSU Qualification

Lenders need evidence to verify the value of vested shares and confirm future vesting schedules. Accurate documents help lenders determine borrower strength and available collateral. This documentation affects both restricted stock loans and early pre-approval stages.

RSU Grant Letters

Grant letters provide the structure of the RSU award and outline vesting terms.

Vesting History

Lenders check past vesting to confirm the borrower’s access to vested shares.

Brokerage Statements

Statements show the number of vested shares and the current market value.

Preparing these documents early simplifies the lending process and helps buyers move faster once they choose a property.

Using RSUs to Strengthen Your Down Payment Strategy

RSUs can play a practical role in strengthening your down payment strategy when traditional savings are not enough.

Many buyers hold significant equity value in their vested stock but do not want to sell shares or trigger taxes. This is where restricted stock loans become useful. They offer a way to access liquidity without disrupting long-term investments or delaying your home search. When structured correctly, RSU-backed financing can shorten timelines, improve loan options, and support buyers navigating competitive markets.

Accessing Liquidity Without Selling Shares

Borrowing against vested RSUs gives buyers access to cash without selling shares. Lenders evaluate vested stock and issue financing based on approved loan-to-value limits. This provides immediate liquidity that supports a stronger down payment.

How do restricted stock loans supply cash

Restricted stock loans use vested RSUs as collateral to issue cash that can be used toward home financing. These loans give buyers access to capital without the need to liquidate their holdings.

Why does this help with a down payment?

Using RSUs expands buying power and reduces reliance on long-term savings. This helps buyers secure a home sooner and prepare for mortgage pre-approval with stronger funds in place.

Faster Path to Homeownership

RSU-backed financing helps buyers move earlier than expected. Traditional saving timelines can take years, especially in high-cost markets. RSUs provide access to funds that support immediate action.

How RSUs accelerate purchase timelines

Borrowers can convert vested shares into usable financing more quickly than saving cash over time. This helps them enter the market when the right home appears.

Impact on buying a home in Seattle

Because Seattle home prices change quickly, RSUs help buyers secure property before prices rise further. This supports faster and more confident decisions when buying a home in Seattle.

Flexibility in Loan Structure

Lenders can structure RSU-backed loans to fit borrower needs. This flexibility helps align monthly payments with cash flow and investment goals.

Interest rate variations

Rates vary depending on loan type, borrower strength, and market conditions. Buyers can choose structures that match their financial comfort.

Payment options

Some loan types offer interest-only periods or adjustable repayment terms. These choices help buyers manage cash flow during the early years of homeownership.

Potential Tax Efficiency

Using RSUs as collateral allows buyers to borrow instead of selling. This reduces immediate tax exposure and leaves long-term investment potential intact.

Borrowing vs selling

Borrowing against vested RSUs avoids triggering tax events that come with selling shares at a gain. This can preserve investment value while still providing liquidity.

Impact on capital gains

Deferring sales helps delay capital gains tax. Buyers can time future sales with a more thoughtful financial strategy instead of selling under pressure.

Leveraging RSUs through restricted stock loans gives buyers a more flexible and efficient path toward securing their home. With careful planning and early preparation, RSUs help strengthen financial readiness and support a smoother homebuying process.

Loan Types Supported by RSUs

RSUs can support different lending structures when buyers explore restricted stock loans.

These loan types offer access to liquidity without needing to sell vested shares.

Understanding how each option works helps buyers plan their down payment strategy and prepare for mortgage pre-approval with clarity.

Non-Recourse Loans

Non-recourse loans let buyers borrow against vested RSUs without risking personal assets. If the loan defaults, the lender can only claim the pledged shares, which provides strong borrower protection.

What they are

Non-recourse loans use vested RSUs as the only collateral for financing. If the stock value drops, the lender cannot go after your home, income, or savings.

Pros and cons

Borrowers gain strong liability protection, but lenders offset this risk with higher interest rates and lower borrowing limits.

This loan type works well for buyers who want predictable liability and are comfortable with smaller loan amounts. It offers safety in exchange for stricter borrowing limits.

%2520in%2520Seattle%2520(1).png)

Margin Loans

Margin loans offer quicker access to liquidity and may come with lower interest rates. They are attractive to buyers who want speed and flexibility when leveraging vested RSUs.

When they work

Margin loans suit buyers who want fast financing and understand how stock price changes affect available collateral.

Risks and suitability

If the stock price drops, a margin call may require more collateral or early repayment. This makes margin loans better for buyers with strong financial reserves.

Margin loans can support homebuyers who value flexibility and fast financing. They require careful monitoring and enough liquidity to handle market swings.

Choosing the Right Structure

Selecting the right RSU-backed loan depends on income stability, vesting schedules, and long-term financial goals.

Each structure affects cash flow and repayment expectations.

Cash flow impact

Non-recourse loans may require higher payments, while margin loan costs shift with market changes. Buyers should understand potential adjustments before committing.

Long-term alignment

Borrowers should choose a loan that fits future vesting, investment plans, and homeownership goals. Proper alignment helps avoid financial strain later.

A well-matched loan structure helps RSUs support your homebuying strategy smoothly. With thoughtful planning, these options can create a clear and efficient path to homeownership.

Work With A Broker Who Can Guide You Through Equity Compensation

Working with a broker who understands equity compensation is essential when exploring restricted stock loans. A specialized broker can explain how lenders evaluate RSUs, help structure terms that match your income and vesting schedule, and identify risks that general lenders may overlook.

This level of guidance helps buyers avoid early repayment surprises and ensures that loan terms remain manageable even if markets shift.

As we established throughout this article, early preparation strengthens your financing strategy. Aligning RSU-backed options with long-term goals makes the borrowing process smoother, and preparing for pre-approval early helps you act quickly when the right home appears.

With the right planning and the right expert, restricted stock loans can support a clear, confident path to homeownership.

Frequently Asked Questions

Can I use RSUs or RSAs as income when applying for a mortgage?

Yes. Many lenders allow vested RSUs or RSAs to count as income, but they review the vesting history to confirm consistency. Lenders also assess how long you have received equity compensation and whether future vesting is likely to continue.

What documentation do lenders require to accept restricted stock as income?

Lenders typically require RSU or RSA grant letters, vesting schedules, brokerage statements, and recent pay records. These documents help verify the number of vested shares, their value, and the consistency of equity-based compensation.

How do lenders calculate income from restricted stock for loan qualification?

Lenders usually average the value of vested shares over a defined period and may apply a discount to account for stock volatility. They also confirm ongoing vesting to ensure the income source is stable enough to support approval for restricted stock loans.

Do I need the stock to be publicly traded to use it for income qualification?

In most cases, yes. Lenders prefer publicly traded stock because the market price is transparent and easier to verify. Private-company RSUs may be restricted or harder to value, making them less likely to be accepted for loan qualification.

What happens if my stock price drops after qualification but before closing?

A significant price drop may reduce the value of vested shares used for qualification. This can lead some lenders to re-evaluate your approval or adjust loan terms if the collateral no longer meets their requirements, especially when using restricted stock loans.

Sign in to leave a comment.