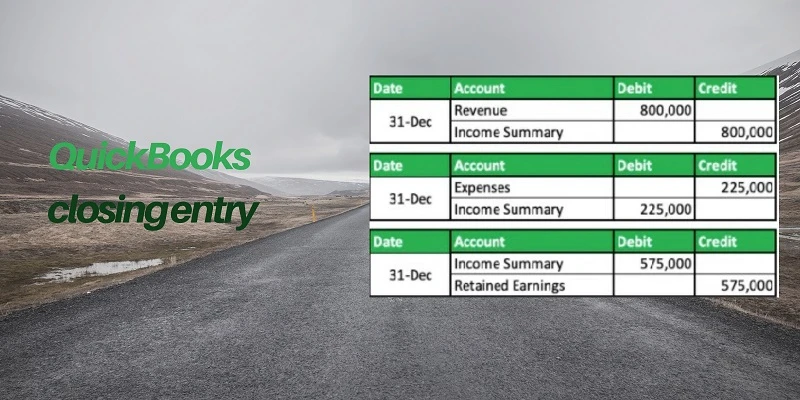

The QuickBooks closing entry is used in QuickBooks to transfer income and expense bills for retired profits. It is also used as an audit trail mechanism as it assures that the accounting records are correct and consistent each year. The transactions involving transactions before, during and after which entries of accounts are transferred are called forward system transactions.

What Is QuickBooks closing entry

The QuickBooks closing entry is used to consolidate transient accounts at the end of the year to transfer income and expense bills for retired profits. If you use QuickBooks to manage your finances, this task can be time-consuming.

When you close your QuickBooks file, you consolidate all the items that have been paid or settled during the year into one single account. This includes:

Income items such as sales commissions, interest on savings deposits and other income received during the period.

Expense items such as payment of salaries and wages, expenses for vehicles and other expenditures that were incurred during the year.

How to closing entry in quickbooks

conclusion

To process the closing entries under different subheadings, we require full working knowledge of each category / subheading. For example, if you sell on credit and make payment to a supplier after 30th June, no payment is incurred at the end of the financial year. To transfer this expense to Profit & Loss account, the customer account will be credited and the Supplier Ledger Account will be debited. We will learn how to enter in such a situation through QuickBooks Closing entry. The same way, there will be many other examples or scenarios wherein we will have to use QuickBooks Closing entries for transferring transient accounts that really belong in Profit & Loan loss Account for Financial Purposes.

0

Sign in to leave a comment.