In the evolving world of digital finance, businesses are constantly looking for faster, safer, and more cost-effective ways to move money. Two of the most important payment systems today are ACH transfers and real-time payments (RTP). While both serve the same fundamental purpose—transferring money electronically—they operate very differently and are suited for different business needs.

Understanding how these payment methods work, their advantages, and how they fit into a broader fintech ecosystem can help businesses streamline operations, improve cash flow, and deliver a better customer experience.

What Are ACH Transfers?

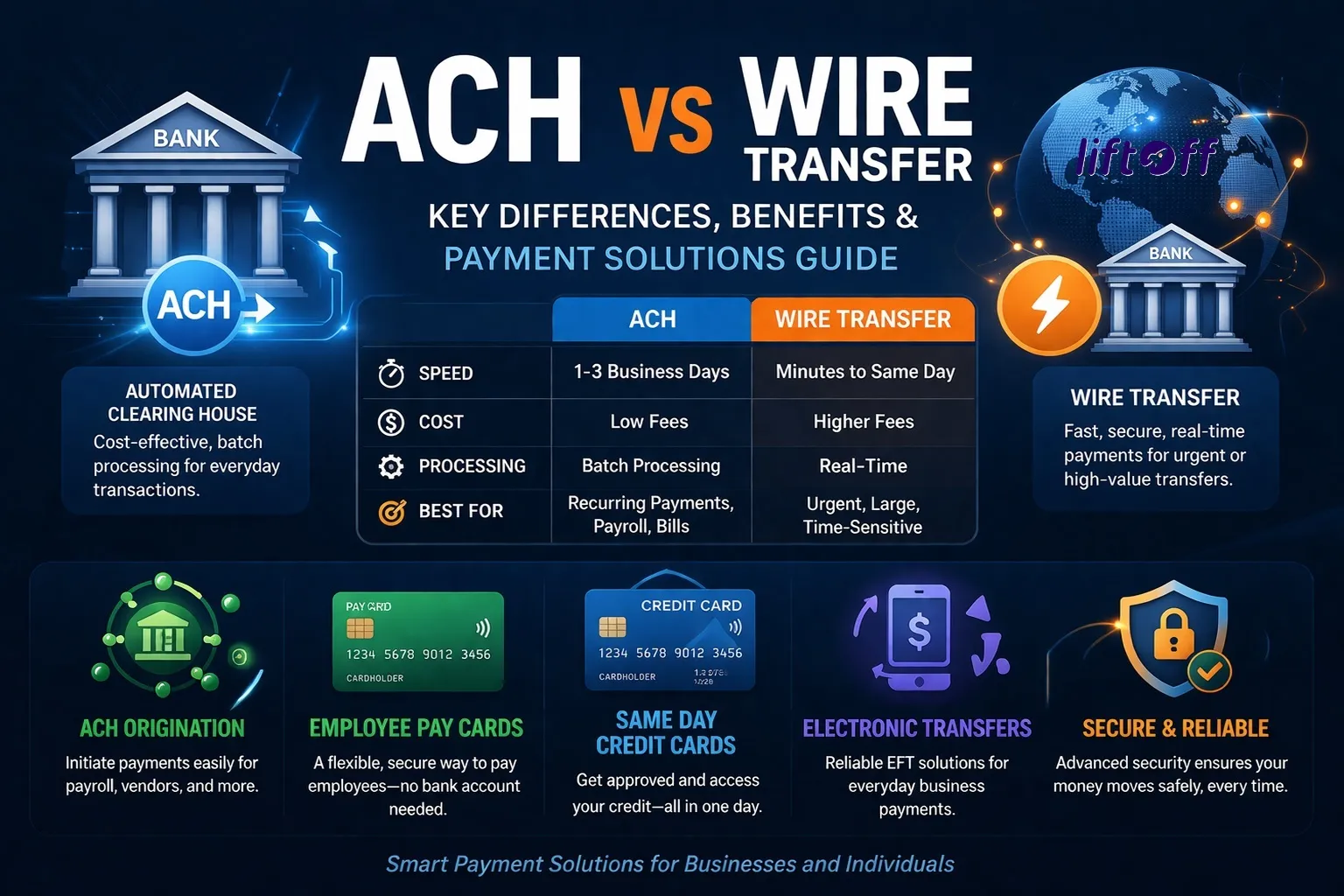

ACH (Automated Clearing House) transfers are electronic payments processed through a centralized network that connects banks and financial institutions. These payments are typically processed in batches, meaning transactions are grouped together and settled at specific intervals during the day.

ACH transfers are widely used for:

- Payroll processing

- Vendor and supplier payments

- Subscription billing

- Direct deposits and withdrawals

How ACH Transfers Work

When a payment is initiated, it is sent to the ACH network, where it is grouped with other transactions. These batches are then processed and cleared, usually within one to three business days.

Advantages of ACH Transfers

- Cost-Effective

ACH payments are significantly cheaper than wire transfers or card payments, making them ideal for high-volume transactions. - Reliable and Secure

The ACH network is regulated and has strong security protocols, reducing the risk of fraud. - Ideal for Recurring Payments

Businesses can automate payments such as subscriptions or salaries, saving time and effort. - Wide Adoption

Almost all banks support ACH transfers, making them accessible for most businesses and customers.

Limitations of ACH Transfers

- Slower processing times compared to instant payment methods

- Limited availability on weekends and holidays

- Less suitable for urgent or time-sensitive payments

What Are Real-Time Payments (RTP)?

Real-time payments are a newer innovation that allows funds to be transferred instantly between bank accounts, 24/7. Unlike ACH transfers, RTP systems process transactions individually and settle them within seconds.

How Real-Time Payments Work

When a payment is initiated, it is immediately verified, processed, and settled. The recipient gets access to the funds almost instantly, regardless of the time or day.

Advantages of Real-Time Payments

- Instant Transactions

Funds are transferred and available within seconds, improving efficiency. - 24/7 Availability

Payments can be made anytime, including weekends and holidays. - Improved Cash Flow Management

Businesses can access funds immediately, helping with better financial planning. - Enhanced Customer Experience

Customers appreciate faster transactions, especially for refunds or payouts.

Limitations of Real-Time Payments

- Higher transaction costs compared to ACH

- Not universally available in all regions

- Some banks may have transaction limits

ACH Transfers vs Real-Time Payments: Key Differences

| Feature | ACH Transfers | Real-Time Payments |

|---|---|---|

| Processing Time | 1–3 business days | Instant |

| Cost | Low | Higher |

| Availability | Business hours | 24/7 |

| Transaction Type | Batch processing | Individual processing |

| Best Use Case | Recurring & bulk payments | Urgent & instant payments |

Choosing the Right Payment Method for Your Business

Selecting between ACH and RTP depends on your operational needs and priorities.

When to Use ACH Transfers

- Payroll and employee payments

- Monthly subscriptions or billing cycles

- Bulk vendor payments

- Situations where cost savings are a priority

When to Use Real-Time Payments

- Instant customer refunds

- Emergency or time-sensitive transactions

- Marketplace payouts

- Situations where speed is critical

For many businesses, the best approach is to use a combination of both systems. This allows you to balance cost efficiency with speed and flexibility.

The Role of Fintech in Modern Payment Systems

Modern fintech platforms go beyond simple payment processing. They integrate advanced tools that help businesses manage risk, improve decision-making, and enhance customer trust.

1. Underwriting Tools

Automated underwriting tools help businesses assess credit risk quickly and accurately. By analyzing financial data, these tools enable faster approvals and reduce manual work.

2. Credit Monitoring

Credit monitoring systems track changes in credit profiles and alert users to potential risks. This is especially useful for lenders and financial service providers.

3. Credit Builder Accounts

Credit builder accounts are designed to help individuals improve their credit scores. These accounts encourage responsible financial behavior and expand access to credit.

4. Rent Reporting

Rent reporting services allow tenants to report their rent payments to credit bureaus. This helps build a positive credit history and improves financial inclusion.

Chargebacks can be costly for businesses, especially in eCommerce. Advanced tools help detect fraudulent transactions, reduce disputes, and protect revenue.

Why Payment Strategy Matters More Than Ever

In a competitive market, having the right payment strategy can make a significant difference. Businesses that adopt modern payment solutions can:

- Improve operational efficiency

- Reduce transaction costs

- Enhance customer satisfaction

- Minimize financial risks

By combining ACH transfers for cost efficiency and real-time payments for speed, businesses can create a balanced and effective payment ecosystem.

Future Trends in Digital Payments

The payment landscape is continuously evolving, driven by technology and changing consumer expectations.

1. Increased Adoption of Real-Time Payments

As infrastructure improves, more businesses and banks will adopt RTP systems.

2. Integration of AI and Automation

AI-powered tools will enhance fraud detection, underwriting, and financial decision-making.

3. Greater Focus on User Experience

Seamless and fast payment experiences will become a key differentiator for businesses.

4. Expansion of Open Banking

Open banking will enable better data sharing and more innovative financial solutions.

Conclusion

ACH transfers and real-time payments are both essential components of modern financial systems. While ACH offers affordability and reliability for recurring transactions, real-time payments provide speed and convenience for urgent needs.

The most successful businesses are those that understand the strengths of each system and use them strategically. By integrating advanced fintech tools such as underwriting systems, credit monitoring, and chargeback prevention, companies can go beyond basic payments and build a robust financial infrastructure.

In the end, the goal is not just to move money—but to do it smarter, faster, and more securely.

Sign in to leave a comment.