If you are over the age of 18 then you’ve probably heard about Tax-Free Savings Accounts (TFSAs). Maybe a friend mentioned they were “maxing out their TFSA,” or you noticed the option in your online banking app but never clicked on it. If that’s so, then you might have wondered: How does a TFSA work? And is it really as good as people say?

Find the truth in this guide. Understand what it is and how it is one of the most powerful financial tools available to Canadians.

What Is a TFSA in Canada?

Let’s start with the basics. TFSAs, or Tax-Free Savings Accounts are registered accounts that allow Canadian residents aged 18 or older to save and invest money. They need not pay taxes on the growth or withdrawals. Interesting, isn’t it!

Think of it as a bucket you can fill with almost any type of investment. Once inside, whatever you earn, say, interest, dividends, or capital gains: it is completely tax-free. And when you withdraw the money, you don’t owe a cent to the Canada Revenue Agency (CRA).

The freedom of tax-free growth and withdrawals makes it one of the most flexible savings vehicles Canada offers.

How Does a TFSA Work?

Let’s understand this way: suppose you set aside $500 a month in your TFSA. You invest in a broad-market ETF (Exchange-Traded Fund), and over time, your savings grow thanks to dividends and market returns. An ETF is a fund that help you buy a tiny piece of hundreds of top companies at once, all in one low‑cost investment.

Now, five years later, you decide to use $20,000 for a down payment on your first home. You withdraw it tax-free. Here comes the best part: the following year, that $20,000 contribution room comes back, ready for you to use again!

Here’s the step-by-step breakdown of how it works:

- Opening a TFSA: Any Canadian resident who is aged 18+ (or age of majority in your province) with a valid Social Insurance Number (SIN) can open one through a bank, credit union, or online platform.

- Contributing: In 2025, the annual limit is $7,000. If you haven’t contributed since TFSAs were introduced in 2009, you may have up to $102,000 in available room.

- Withdrawals: You can take out money at any time, for any reason. There will be no taxes, or penalties.

- Re-contribution: Any money you withdraw is added back to your TFSA room the following year.

- Penalties: Over-contributing triggers a 1% monthly penalty on the excess, so keeping track is crucial.

To gain deeper understanding of how TFSA works you can contact the best insurance consultants who can guide you thoroughly.

TFSA is designed to be simple yet the benefits can be life-changing. Let’s talk about the benefits next.

TFSA Benefits That Canadians Love

- Tax-Free Growth: Your money works harder without taxes eating into your returns.

- Tax-Free Withdrawals: Whether it’s for a car, tuition, or a medical emergency, your money is yours to use with no strings attached.

- No Impact on Government Benefits: Unlike RRSP withdrawals, TFSA withdrawals don’t affect eligibility for benefits like Old Age Security (OAS) or the Guaranteed Income Supplement (GIS).

- No Expiry: Your TFSA doesn’t end at 71, unlike RRSPs. You can keep it for life.

- For Any Goal: Emergency fund, travel, home renovations, or retirement — the TFSA adapts to your needs.

In short, it’s one of the most flexible and forgiving accounts available to Canadian savers.

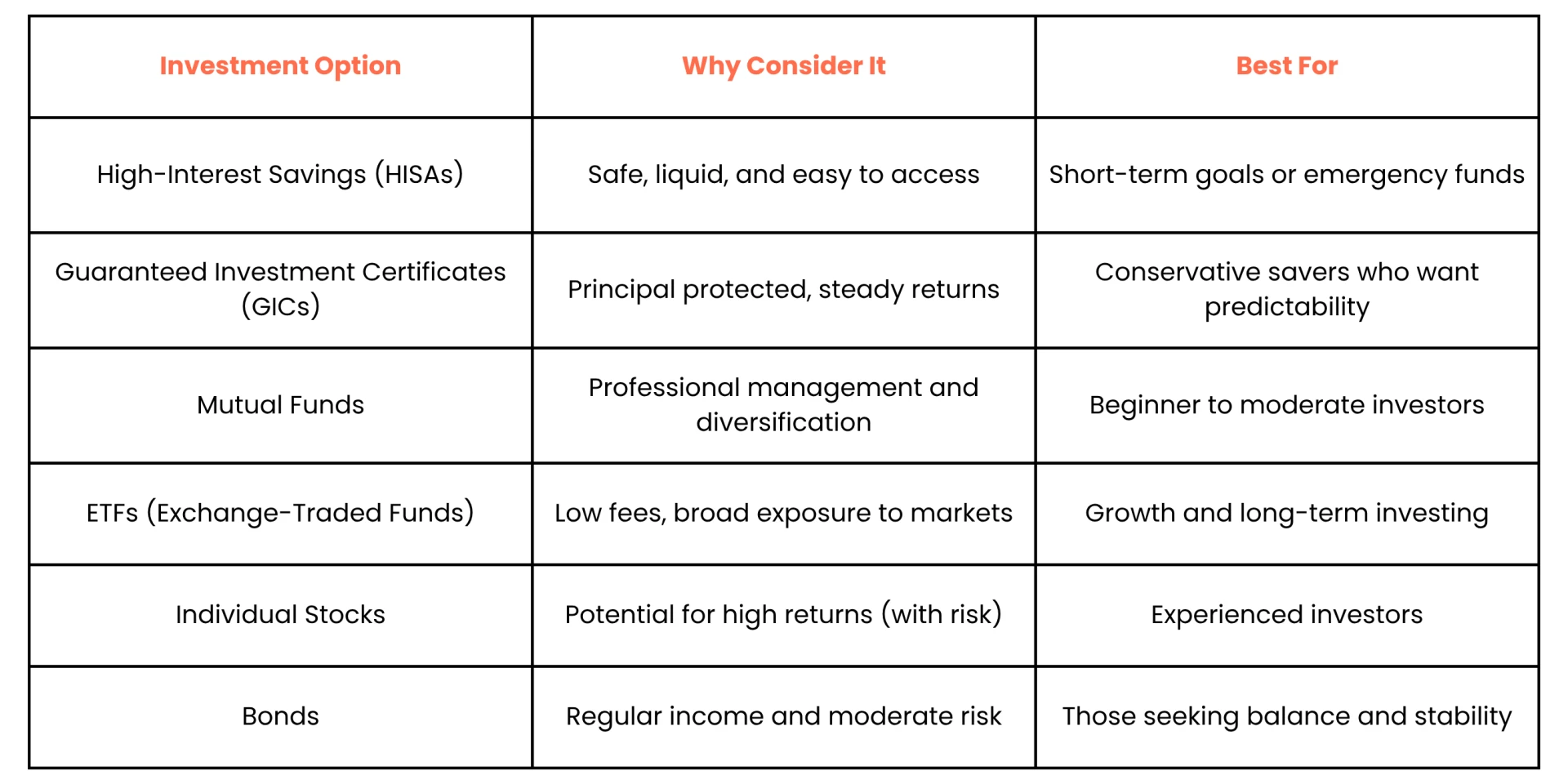

Best TFSA Investments for 2025

Here’s where many Canadians get tripped up. Despite the name “savings account,” your TFSA doesn’t have to sit idle earning a few cents of interest. It can hold a wide variety of investments, tailored to your goals and risk comfort.

Top Picks for 2025 include broad-market ETFs that track Canadian and global indices, blue-chip Canadian stocks known for reliable dividends, and all-in-one ETF portfolios (like Vanguard VEQT) for instant diversification without complexity.

How to Use Your TFSA Strategically

The flexibility of a TFSA means there’s no single “right” way to use it. But there are smart strategies that can maximize its value:

- Start Early: The sooner you begin, the more time compounding has to work.

- Match Investments to Your Goal: Use HISAs or GICs for short-term savings; ETFs or mutual funds for long-term growth.

- Avoid Over-Contributing: Check your CRA My Account regularly to track your contribution room.

- Use It as a Retirement Supplement: Combine your TFSA with an RRSP to balance tax-free and tax-deferred savings.

- Reinvest Withdrawals Next Year: If you take out money, plan to replace it once your room resets.

Common Mistakes to Avoid

Even with its flexibility, there are pitfalls Canadians often fall into:

- Leaving It as Just a Savings Account: A TFSA can be much more powerful when invested.

- Over-Contributing: This mistake leads to avoidable penalties. Hence, it better to always know your limit.

- Not Coordinating with RRSPs: Many overlook how TFSAs and RRSPs can complement each other.

- Ignoring Contribution Room: Assuming your bank tracks it perfectly can backfire. Always double-check with CRA.

- Waiting for ‘Later’: The earlier you start, the bigger the benefits. Don’t let procrastination cost you years of growth.

Final Thoughts

Tax-Free Savings Accounts aren’t just another line on your banking dashboard, they are one of the most effective, flexible, and empowering ways to build wealth in Canada. Whether you’re saving for a near-term purchase or planning for retirement decades away, the TFSA gives you control, tax-free growth, and freedom from penalties when you need your money most.

The best TFSA investments are the ones that align with your goals. The most important step is to start using it, even with small contributions. Over time, those dollars can compound into something significant.

Because when it comes to building financial security, the TFSA isn’t just about saving: it’s about giving yourself choices, opportunities, and peace of mind.

Sign in to leave a comment.