Managing finances in a legal practice requires precision, compliance, and strategic planning. Law firm accounting is more than just bookkeeping — it ensures regulatory compliance, improves profitability, and helps firms make informed business decisions. Whether you’re a solo practitioner or a large firm, understanding accounting fundamentals is essential for long-term success.

What Is Law Firm Accounting?

Law firm accounting refers to the specialized financial management processes tailored specifically for legal practices. It includes tracking client trust accounts, managing billing, handling expenses, ensuring tax compliance, and producing financial reports.

Unlike other businesses, law firms must follow strict ethical and regulatory rules, especially when managing client funds, making proper accounting practices critical.

Why Is Law Firm Accounting Important?

Proper accounting helps law firms:

- Maintain compliance with legal and trust accounting regulations

- Track profitability by practice area or client

- Improve cash flow management

- Prepare accurate financial statements

- Avoid penalties and financial mismanagement

- Make strategic growth decisions

Without a structured accounting system, firms may face compliance risks and financial inefficiencies.

Key Components of Law Firm Accounting

1. Trust Accounting (IOLTA Management)

Law firms often hold client funds in trust accounts. Proper tracking and reconciliation are essential to ensure funds are used correctly and comply with regulations.

2. Legal Billing and Invoicing

Accurate time tracking and billing ensure firms get paid for their work. This includes hourly billing, flat fees, contingency billing, and automated invoicing systems.

3. Expense Tracking

Tracking operational expenses like salaries, office rent, software, and court fees helps firms understand their cost structure and manage budgets effectively.

4. Financial Reporting

Regular financial reports such as profit and loss statements, balance sheets, and cash flow statements provide insights into the firm’s financial health.

5. Tax Planning and Compliance

Law firms must comply with local tax regulations and plan strategically to minimize liabilities while staying compliant.

Common Challenges in Law Firm Accounting

Many firms struggle with:

- Managing complex trust account rules

- Tracking billable hours accurately

- Handling multi-client expenses

- Maintaining compliance with changing regulations

- Integrating accounting with practice management software

These challenges often lead firms to seek professional accounting support.

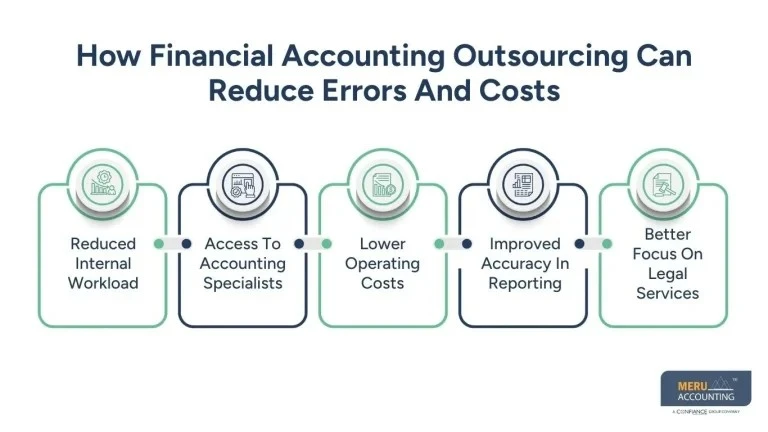

Benefits of Professional Law Firm Accounting Services

Outsourcing or working with specialized accountants can provide several advantages:

- Expertise in legal industry compliance

- Reduced administrative workload

- Accurate financial reporting

- Better cash flow management

- Scalable accounting solutions as the firm grows

- Improved financial transparency

Best Practices for Effective Law Firm Accounting

To maintain strong financial management, law firms should:

- Use dedicated legal accounting software

- Separate operating and trust accounts

- Perform regular reconciliations

- Monitor key performance indicators (KPIs)

- Maintain clear billing policies

- Work with experienced accounting professionals

Choosing the Right Accounting Solution for Your Law Firm

When selecting accounting support, consider:

- Experience with legal industry regulations

- Technology and automation capabilities

- Scalability for future growth

- Transparent pricing

- Strong reporting and analytics

The right partner can significantly improve efficiency and profitability.

Conclusion

Effective law firm accounting is essential for maintaining compliance, improving financial performance, and supporting sustainable growth. By implementing structured processes, leveraging technology, and working with experienced professionals, law firms can focus more on serving clients while maintaining strong financial health.

Sign in to leave a comment.