Every personal loan application in India starts with the same first step: KYC verification. Before a lender even looks at your income or credit score, it needs to confirm who you are and where you live. Getting this part right saves you from delays later in the process, so understanding exactly what counts as valid KYC and how each document is used makes your application smoother from the very first form you fill.

This guide breaks down the KYC essentials, the role each specific document plays, and practical tips to make sure your paperwork clears verification without hiccups.

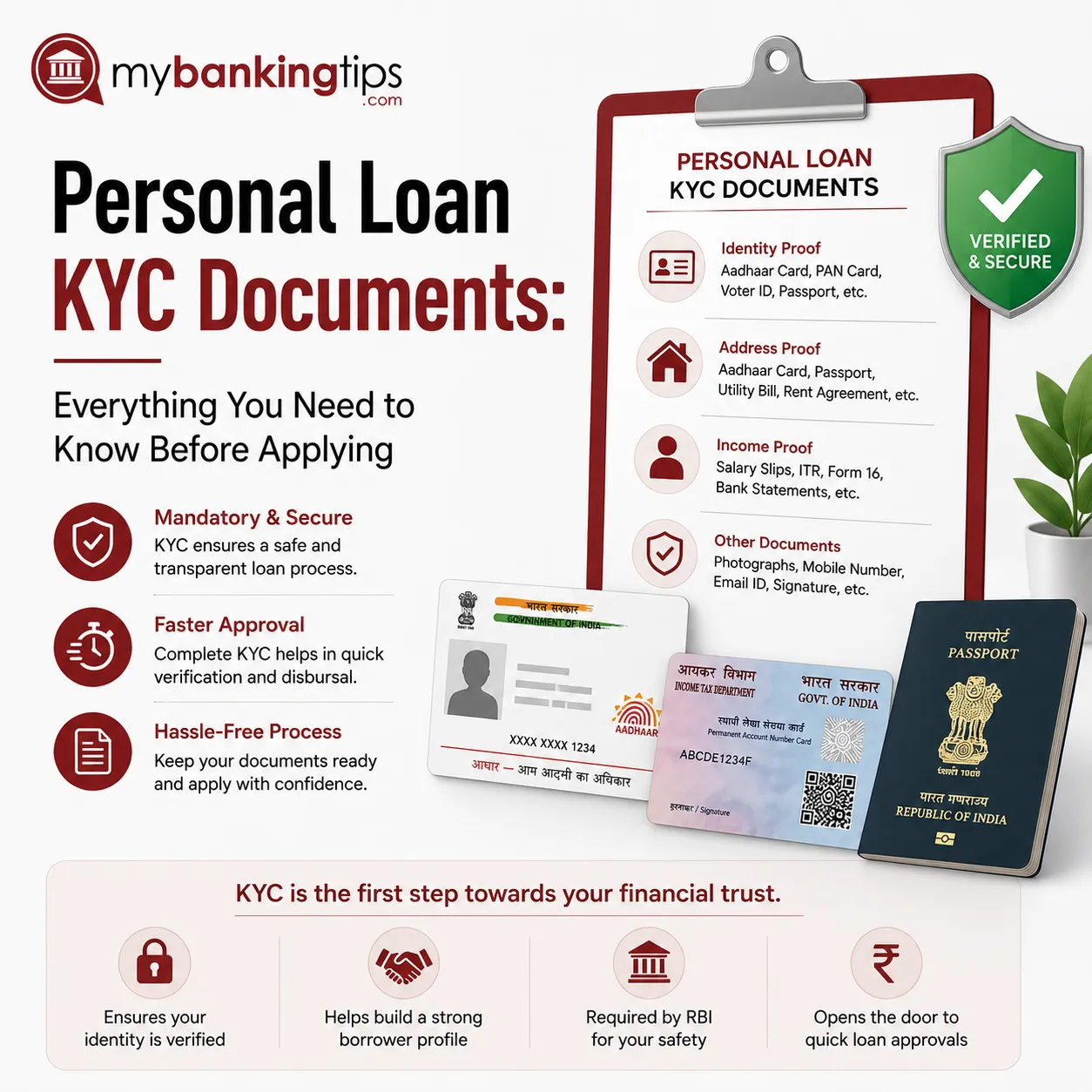

What Counts as Valid Personal Loan KYC Documents

Under RBI guidelines, personal loan KYC documents are split into two categories: proof of identity and proof of address. Most lenders accept a fixed list that includes PAN card, Aadhaar card, Voter ID, passport, and driving licence. Among these, PAN and Aadhaar together cover almost every requirement, which is why nearly all digital lenders ask for these two first before requesting anything else.

KYC exists to prevent fraud and comply with anti-money laundering regulations, not just to slow down your application. Lenders are legally required to verify your identity independently, which is why photocopies or scanned images need to be clear and unedited. Blurry uploads or mismatched details are one of the most common reasons digital applications get stuck in manual review.

The Role of Aadhaar Card for Personal Loan Applications

An Aadhaar card for personal loan approval plays a dual role, since it serves as both identity and address proof simultaneously. This is precisely why most online lenders prioritise Aadhaar-based e-KYC, which uses your registered mobile number to verify your identity within minutes rather than requiring physical document submission.

The catch is that your Aadhaar address must be current. If you have moved cities or changed your residence recently without updating Aadhaar, lenders may flag a mismatch during address verification. Updating your Aadhaar online before applying is a quick fix that prevents this issue from delaying your loan altogether.

Why PAN Card for Personal Loan Is Non-Negotiable

There is no version of a personal loan application in India that skips PAN. A PAN card for personal loan requirement exists because PAN links directly to your income tax records and your CIBIL report, giving lenders a single reference point to pull your credit history and verify your financial background accurately.

Beyond identity verification, PAN is also how lenders report your loan account to credit bureaus once it is disbursed. If your PAN details do not match your name exactly as it appears on other documents, this discrepancy can create friction during the final underwriting stage, even after your application has otherwise been approved.

How a Salary Slip for Loan Applications Is Evaluated

For salaried applicants, a salary slip for loan approval carries significant weight, since it confirms your monthly take-home income directly from your employer. Most lenders ask for the last three months of salary slips, and they specifically check your net salary after deductions, not your gross figure, since that reflects what you actually have available to repay an EMI.

Consistency matters here too. If your salary has fluctuated significantly month to month, or if your slips show irregular deductions, lenders may ask for additional clarification or an employer letter. Keeping your salary slips organized and easily accessible in digital format speeds up this part of the verification considerably.

What Lenders Look for in a Bank Statement for Personal Loan

A bank statement for personal loan review goes far beyond simply confirming that your salary is credited on time. Lenders typically request the last six months of statements for salaried applicants, sometimes twelve for self-employed borrowers, because a longer window reveals patterns that a single pay slip cannot show.

Specifically, underwriters look at three things: whether your income credits are regular and match your declared salary, how many existing EMIs or credit card payments are already being deducted from your account, and whether there are any bounced cheques or failed auto-debit attempts. A clean statement with no bounced payments and manageable existing obligations significantly improves your approval odds and can even help you negotiate a better interest rate.

Bringing It All Together for a Smooth Application

Each of these documents works together rather than independently. Your Aadhaar and PAN establish who you are, your salary slips show your current earning capacity, and your bank statement validates that both of these are accurate over time. When all four align consistently, verification moves quickly because there is nothing for the lender to question.

Before submitting your application, it helps to review your own documents the way an underwriter would. Check that your name, address, and date of birth match exactly across every document, that your salary slips reflect the same employer mentioned in your bank statement credits, and that there are no unexplained gaps or bounced transactions in your recent banking history.

Practical Tips to Avoid KYC Rejection

Keep digital copies of every document ready in PDF format before you start your application, since most online lenders require immediate upload rather than allowing you to submit later. Update your Aadhaar address if you have moved recently, and make sure your mobile number linked to Aadhaar is active, since e-KYC depends entirely on OTP verification through that number.

My Banking Tips recommends applying only once your documents are fully consistent across every category, since repeated applications with mismatched paperwork can trigger multiple hard inquiries and lower your credit score unnecessarily.

Final Thoughts

KYC and document verification form the foundation of every personal loan application, and getting them right the first time is far more efficient than fixing errors mid-process. Keep your PAN, Aadhaar, salary slips, and bank statements consistent and current, and your application will move through verification with minimal friction.

FAQs

- Can I complete personal loan KYC without visiting a bank branch?

Yes, most digital lenders now offer Aadhaar-based e-KYC, which verifies your identity through an OTP sent to your registered mobile number, completing the process entirely online within minutes.

- What happens if my Aadhaar address doesn't match my current residence?

Lenders may flag this as a mismatch during address verification. It's best to update your Aadhaar address online before applying to avoid delays or requests for additional address proof.

- How many months of bank statements do lenders usually require?

Salaried applicants typically submit six months of statements, while self-employed applicants often need twelve months, since business income patterns require a longer observation period for accurate assessment.

- Does a low salary slip amount always lead to rejection?

Not necessarily. Lenders assess your net salary against your existing EMI obligations. A lower salary can still qualify for a smaller loan amount if your repayment capacity remains adequate.

- Why is PAN card mandatory even if I already submitted Aadhaar?

PAN links directly to your credit bureau report and tax records, which Aadhaar does not cover. Lenders need PAN specifically to pull your CIBIL history and verify your financial background.

Sign in to leave a comment.