The United Kingdom continues to be a giant in the international education system, boasting some of the oldest and most innovative institutions in the world. But for many aspiring students, the challenge of realizing their dream of a Masters degree in the UK can come with a major setback: funding.

With international tuition fees ranging from £20,000 to over £50,000 for the most prestigious courses, knowing your financing options is as crucial as your academic credentials.

Navigating the Financial Landscape of UK Higher Education

In 2026, the financial aid environment for international students has changed. Although UK government-backed loans are primarily available to local students, a strong market of private and international lenders has emerged to fill the gap. For students targeting the best MBA colleges in the UK, the financial outlay is even higher, often requiring a combination of savings, scholarships, and specialized credit.

The Specialized Route: MBA Student Loan for UK

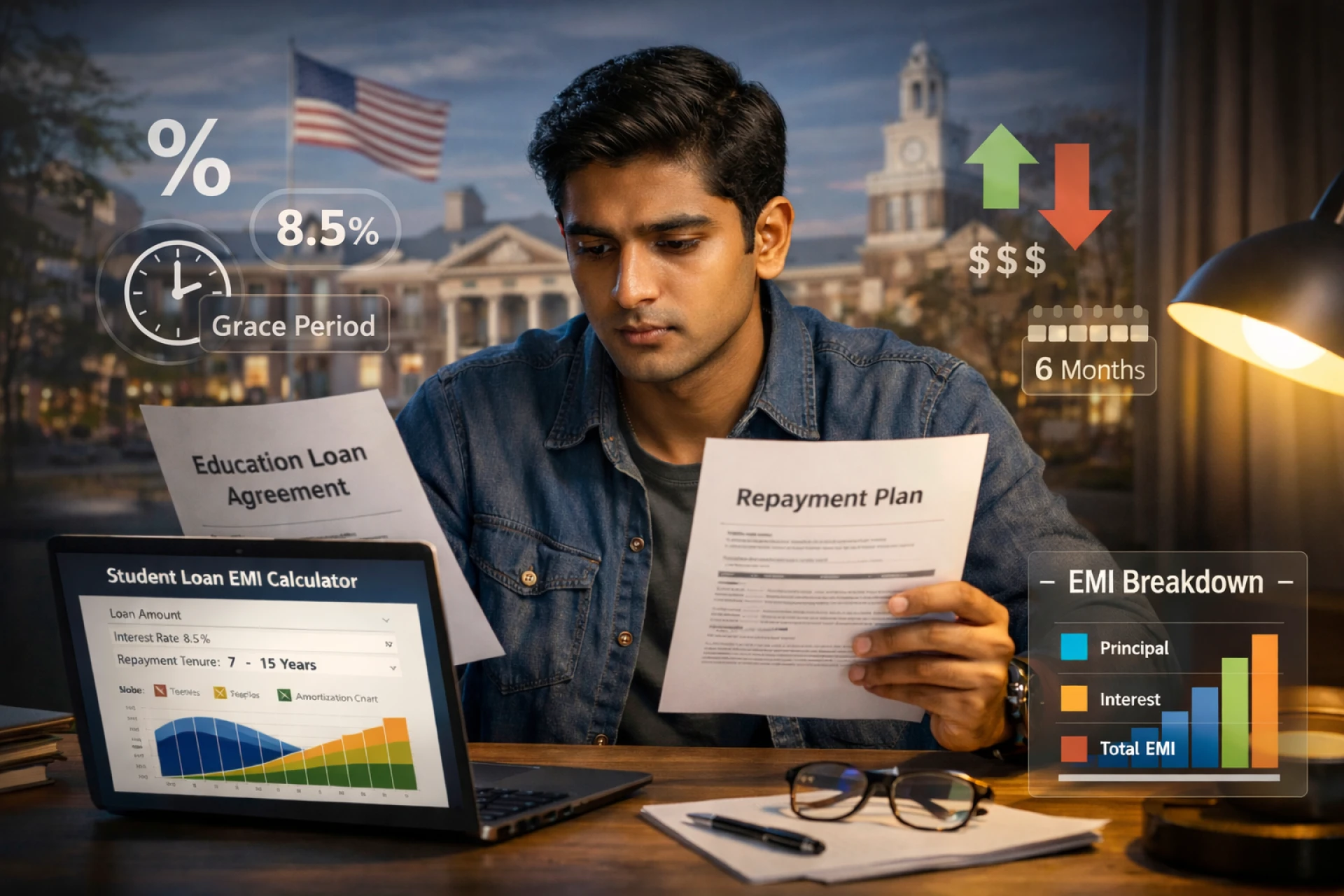

An MBA is a high-yield investment, and lenders treat it as such. An MBA Student Loan for UK often comes with higher borrowing limits and specialized grace periods. Because graduates from top UK business schools see significant salary jumps—often upwards of 45%—lenders are more willing to offer competitive terms based on the prestige of the institution.

Standard Requirements for International Borrowers

While every lender has a unique checklist, most will require:

- A Confirmed Offer: You will need a letter of admission from an accredited UK university.

- Academic Transcripts: Documentation of your success in your undergraduate studies.

- Valid Passport & Visa: You would need your loan sanction letter to apply for your Student Route visa.

- KYC Documents: Normal identity and address checks.

Types of Postgraduate Education Loans for the UK

Students looking for a Study Masters Education Loan UK will find two primary options:

- Home Country Loans: Most students find loans from banks in their home country. These loans are secured by tangible collateral (such as real estate) and must be co-signed.

- International Private Lenders: These fintech lenders evaluate you on the basis of your "future earning potential," not your present assets.

These are especially popular with students seeking no co-signer loans for study in the UK, as they eliminate the need to find a guarantor with a particular credit profile.

Interest Rates and Repayment Terms

In today’s 2026 scenario, the interest rates for international post-grad loans usually range between 9% and 14% APR, depending on the lender and the currency of the loan (USD vs. GBP).

Pro-Tip: Check out “Grace Periods.” Specialized lenders enable you to put off full payments until 6 months after graduation, allowing you to find a job through the UK’s Graduate Route (Post-Study Work Visa).

Why "No Co-Signer" Options are Game Changers

The biggest hurdle for middle-class students is the co-signer requirement, which is always a parent with a high income or assets.

No co-signer loans for studying in the UK have made education more accessible. These lenders assess the “RoI” (Return on Investment) of your particular degree program and university, enabling you to take complete control of your financial destiny.

Conclusion: Plan Early, Study Better

You should also be able to secure your funding when you are making your applications to universities. It is not the time to wait until the visa deadline and you start searching the loan. This is because by comparing rates and knowing the needs of the various lenders, you will be able to remain in your studies and not just in the bank account.

Sign in to leave a comment.