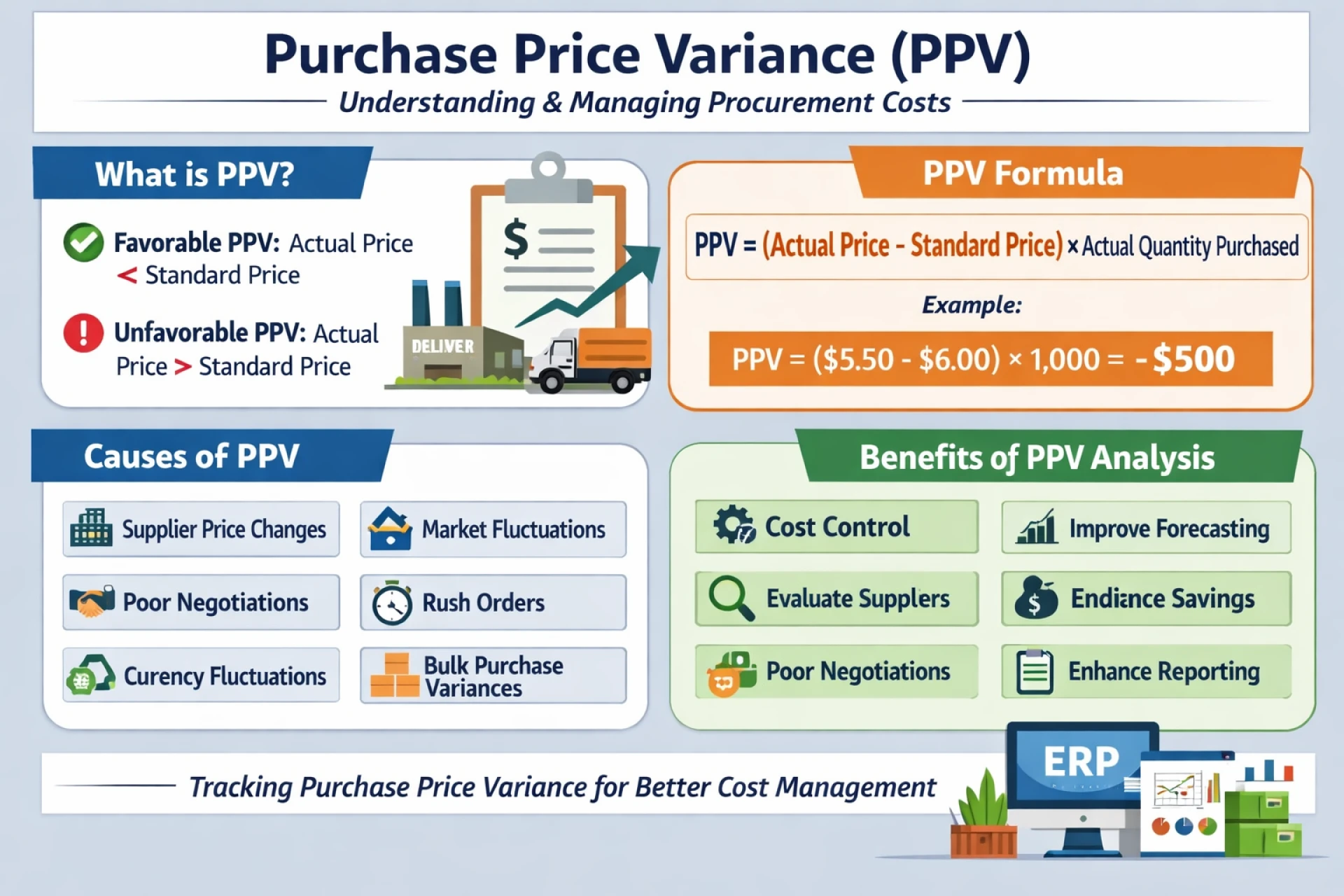

One of the cost control measures commonly used in cost accounting and management accounting is Purchase Price Variance (PPV) which determines the difference between the price paid actually to material and standard price or expected price, times by the quantity of goods purchased. PPV can assist the companies to know how well they are controlling the procurement cost and the supplier costs.

What Is Purchase Price Variance?

Purchase Price Variance takes place when the actual price that a firm pays in buying the raw material is lower or higher than the set standard price. This deviation may be good or bad:

Favourable PPV- here the real purchase price is not the standard price.

Unfavorable PPV is the scenario whereby the actual purchase price is higher than the standard price.

The monitoring of PPV is crucial within such organizations which highly depend on inventory and the purchasing of raw materials like manufacturing, retail and supply chain-based companies.

Purchase Price Variance Formula.

The normal equation of calculating Purchase Price Variance:

PPV = (Actual Price- Standard Price) x Actual Quantity Purchased.

It is a calculation that separates price variances and eliminates variances associated with quantities to enable procurement and finance departments to concentrate on the efficiency of prices.

Reasons of Purchase Price Variance.

Purchase price variance may occur due to a number of factors, and they include:

Supplier price-up or price-down.

Alterations in the market conditions or the price of commodities.

Inadequate negotiating or good contract terms.

Rush orders/emergency purchases.

The fluctuations in the exchange rates.

Differences in volume based pricing.

By pinpointing the source of PPV, it assists the organizations in making remedial action and leading to better next time purchasing choices.

Significance of Analysis of Purchase Price Variance.

The purchase price variance analysis is important in cost management and profitability management. It allows businesses to:

Measure performance of suppliers.

Enhance budgeting and accuracy of forecasting.

Enhance procurement capabilities.

Determine cost-cutting prospects.

Improve inventory and cost accounting.

Unfavorable PPV in a consistent manner could show that there is poor supplier negotiations or ineffective purchasing procedures and positive PPV shows that there is good procurement practices.

ERP system and Accounting Purchase Price Variance.

PPV in a normal costing system is normally charged when an item is purchased and charged to a purchase price variance account. The new ERP systems such as SAP, Oracle and NetSuite can automatically compute and monitor PPV and therefore to provide real-time reporting and based decisions.

Conclusion

Purchase Price Variance is an effective financial tool that offers tremendous information regarding the effectiveness of purchasing as well as the cost control. The frequent analysis of PPV by the organizations will enable them to manage the material costs, enhance supplier relationship and guard the profit margins in a competitive business world.

Visit us: accountinglads.com

Sign in to leave a comment.