Real estate has always been a popular way to build wealth. People are drawn to property investing because it’s seen as safer than stocks, and it often comes with the bonus of owning something physical and tangible. But when it comes to making money in real estate, investors often face one big question: Should I rent out a property, or should I flip it?

Both renting and flipping can bring profits, but they work in very different ways. The right choice depends on your financial goals, risk tolerance, and long-term plans. In this article, we’ll break down both strategies, explore the pros and cons, and help you decide which one might fit your situation best.

What Does Flipping a Property Mean?

Flipping means buying a property, improving it, and then selling it for a profit. Most investors focus on homes that are undervalued, outdated, or need repairs. After renovations, they put the property back on the market at a higher price.

The goal is speed. Flippers want to move quickly—usually within a few months—so they can cash out and move on to the next project.

Benefits of flipping:

- Quick returns: If done well, flipping can bring in large profits in a short amount of time.

- No long-term management: Unlike being a landlord, you don’t deal with tenants or ongoing property issues.

- Flexibility: You can flip properties when the market is hot and step back when conditions cool.

Challenges of flipping:

- High risk: If the market slows down or renovation costs go over budget, profits shrink quickly.

- Taxes: Short-term capital gains taxes can eat into profits.

- Constant hustle: Flippers need to keep finding new deals, contractors, and buyers.

Flipping can be exciting, but it’s also demanding and risky, especially for beginners.

What Does Renting a Property Mean?

Renting means buying a property and keeping it as a long-term investment. Instead of selling, you lease it to tenants who pay rent every month. The goal here is steady, ongoing income, plus long-term appreciation as the property value rises over time.

Benefits of renting:

- Steady income: Rent checks can provide reliable cash flow.

- Long-term growth: Over the years, property values usually rise, adding to your wealth.

- Tax perks: Landlords often get deductions for mortgage interest, repairs, and other expenses.

- Leverage: A rental property can be financed with a mortgage, allowing you to control a large asset with less upfront cash.

Challenges of renting:

- Tenant issues: Late payments, property damage, or high turnover can be stressful.

- Maintenance costs: Roof leaks, plumbing issues, and other repairs are part of the deal.

- Patience required: Unlike flipping, wealth builds slowly over years.

Renting tends to suit investors who want steady, long-term financial growth rather than fast profits.

Key Factors to Consider

When deciding between flipping and renting, think about these important factors:

1. Your Financial Goals

- If you need quick cash and are comfortable with higher risk, flipping might be better.

- If you’re looking for passive income and long-term stability, renting is usually the smarter move.

2. Risk Tolerance

- Flipping is riskier because profits depend on timing, renovations, and market demand.

- Renting is generally safer, though it comes with the hassle of being a landlord.

3. Market Conditions

- In a seller’s market, flipping can be more profitable since buyers compete for homes.

- In a slower market, rentals might perform better because people need affordable housing regardless of home prices.

4. Time Commitment

- Flipping requires intense focus for a short period—finding, fixing, and selling.

- Renting requires ongoing commitment but can be managed with property managers.

Real-Life Example

Imagine you buy a small house for $150,000.

- If you flip it: You spend $30,000 on renovations and sell it for $230,000. After costs, you pocket about $40,000. Quick and rewarding, but also dependent on everything going smoothly.

- If you rent it: You lease it for $1,500 a month. After paying the mortgage, taxes, and repairs, you clear $400 monthly. That’s $4,800 a year, plus the property might be worth $250,000 in 10 years.

Both strategies can make money—the difference is timing and risk.

The Middle Ground: Creative Approaches

Some investors combine both strategies. For example, they might buy a fixer-upper, live in it while renovating, then either rent it out or sell it depending on market conditions. Others build rental portfolios by starting with flips and using profits to buy long-term properties.

This flexible mindset can help investors adapt to changing markets and personal financial needs.

In some places, investors are even exploring newer ideas, like tiny homes communities New Jersey, where affordable housing demand is rising. These unique opportunities can offer steady rental income or quick flips depending on how the investor approaches the deal.

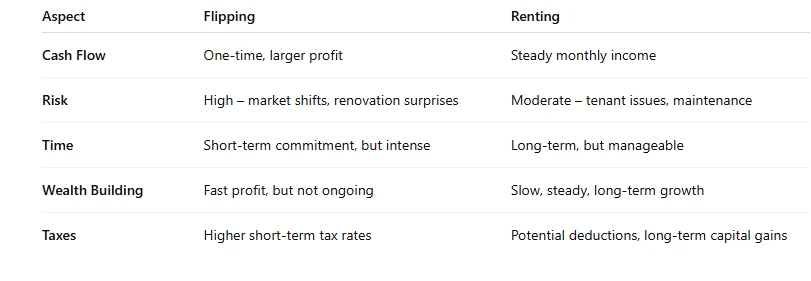

Renting vs. Flipping: Pros and Cons Side by Side

Which Strategy Is Right for You?

There’s no single right answer. It all comes down to your situation.

- Choose flipping if: you enjoy projects, can handle risk, and want fast profits.

- Choose renting if: you prefer steady income, value long-term wealth, and don’t mind dealing with tenants or hiring property managers.

- Mix both if: you want the best of both worlds and are willing to adapt.

Some investors start out flipping because it requires less patience, then shift to rentals for stability. Others dive straight into rentals for the long-term benefits.

Final Thoughts

Flipping and renting are both proven paths to profit in real estate, but they serve different investor personalities and goals. Flipping is like sprinting—fast, intense, and high risk. Renting is more like a marathon—slower, steadier, and reliable over time.

If you’re just starting out, think carefully about your finances, your time, and your appetite for risk. Real estate can change your financial future, but success depends on choosing the strategy that matches you.

Whether you decide to flip, rent, or mix the two, the most important step is to take action, learn as you go, and keep building your knowledge. Over time, the right choices will pay off.

Sign in to leave a comment.