Buying a 2 BHK under 50 lakhs in Navi Mumbai can feel like striking gold in today’s real estate landscape, especially for first-time homebuyers or young families looking to settle in a well-connected, developing part of the Mumbai Metropolitan Region. But once you spot the right property, the next big question usually is: How do I finance it smartly?

Here’s a human-friendly, easy-to-understand guide to help you make informed decisions about loans and EMIs, because buying a home shouldn’t feel like solving a complicated puzzle.

Understanding The Budget: What Does 50 Lakhs Cover?

Before diving into home loan options, it’s important to understand what a budget of ₹50 lakhs includes. Typically, the quoted price of a 2 BHK under 50 lakhs in Navi Mumbai may cover the base price of the flat, but buyers should factor in:

- Stamp duty & registration (approx. 6-7% of property value)

- GST (only on under-construction properties)

- Maintenance deposit & society formation charges

- Parking (if applicable)

Assuming ₹45–₹47 lakhs goes toward the actual flat price, the remaining ₹3–₹5 lakhs should ideally be reserved for these additional expenses.

Home Loan Basics: How Much Can You Borrow?

Most banks and housing finance companies offer home loans covering up to 75%–90% of the property’s value, depending on your income, credit score, and existing liabilities.

- For salaried individuals: The eligibility usually depends on your net monthly income. As a general thumb rule, banks consider up to 40–50% of the monthly income for EMI payments.

- For self-employed individuals: Loan eligibility is assessed based on average annual income, business stability, and repayment capacity.

Example:

If the flat costs ₹47 lakhs, you might need to make a down payment of ₹7–₹9.5 lakhs, and take a loan of around ₹37.5–₹40 lakhs.

EMI Breakdown: What Will You Pay Monthly?

Your EMI (Equated Monthly Instalment) depends on three factors:

- Loan amount

- Interest rate

- Loan tenure (in years)

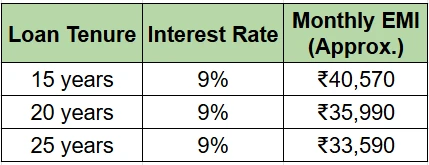

Here’s a simple table to give you a rough idea of the EMI on a ₹40 lakh loan:

(EMIs are indicative. Check exact rates with your preferred bank.)

To ease the monthly burden, many homebuyers choose longer tenures, but keep in mind, a longer tenure means more interest paid over time.

Choosing The Right Bank Or Lender

When picking a home loan provider, don’t just go for the lowest interest rate. Also, look at:

- Processing fees

- Prepayment or foreclosure charges

- Loan portability (in case you want to switch lenders later)

- Customer service and turnaround times

Pro tip: If you already have a salary account with a bank, they may offer you better rates or faster processing.

Tips For Getting Loan Approval Faster

Maintain a good credit score (above 750) – A clean repayment history helps.

Reduce existing liabilities – Lower EMIs from other loans mean higher eligibility.

Keep documents ready – Salary slips, ITRs, bank statements, ID/address proof.

Apply jointly – Adding a co-applicant (like a spouse) can increase your loan eligibility.

Tax Benefits You Can Avail

Buying a home also opens doors to income tax benefits:

- Section 80C: Deduction up to ₹1.5 lakh on principal repayment

- Section 24(b): Deduction up to ₹2 lakh on interest paid annually

- First-time buyers may get additional deductions under Section 80EEA (subject to conditions)

These benefits help reduce overall loan cost, especially in the initial years.

Final Thoughts: Plan Smart, Buy Stress-Free

Owning a 2 BHK under 50 lakhs in Navi Mumbai is very achievable today, especially with flexible loan options and government-backed affordable housing schemes. What matters is planning your finances wisely, don’t overstretch your budget, consider future expenses, and always compare before you commit.

Whether you're looking for peace of mind, a better lifestyle, or just a solid long-term investment, getting the loan part right will make your home buying journey smoother and more secure.

Sign in to leave a comment.