In U.S. insurance, we obsess over external risk.

We model hurricanes.

We stress-test casualty reserves.

We recalibrate pricing for social inflation.

Yet many carriers are exposed to a different kind of risk—one that never appears in catastrophe models or actuarial projections.

It’s the internal risk created by hidden underwriting capacity loss.

This isn’t about poor underwriting skill or weak strategy. It’s about the operational drag that quietly consumes one-third of your underwriting and claims workforce before a single risk decision is even made.

The Everyday Friction No One Measures

Across commercial and personal lines, underwriters routinely:

- Re-key broker submission data into multiple systems

- Toggle between rating tools and policy admin platforms

- Track down missing documentation

- Clarify inconsistencies through email chains

- Manually reconcile system-generated outputs

Individually, each task feels minor. Collectively, they create structural inefficiency.

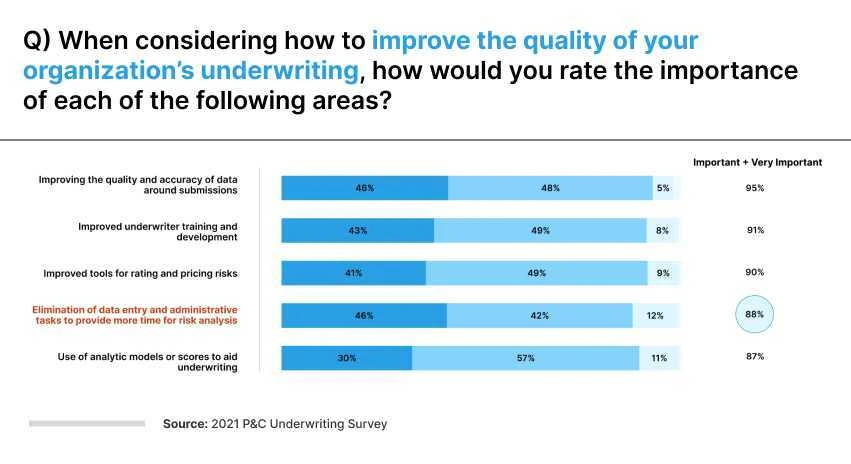

Research from Accenture indicates that property and casualty underwriters spend approximately 35% of their time on non-core tasks. Despite years of digital investment, the improvement curve has been modest.

If a carrier employs 120 underwriters with an average total compensation of $100,000, roughly $4.2 million in annual capacity may be absorbed by non-core activity.

But salary cost is only the surface-level impact.

The deeper issue is strategic.

Hidden Underwriting Capacity Loss Slows Competitive Speed

In today’s U.S. market, brokers and agents value speed almost as much as price.

When underwriters are burdened by administrative drag:

- Quote turnaround extends

- Broker follow-ups increase

- High-quality submissions may sit idle

- Binding authority decisions are delayed

The carrier may believe it has a distribution problem. In reality, it may have a capacity allocation problem.

Hidden underwriting capacity loss reduces an insurer’s effective market velocity.

In competitive middle-market and small commercial segments, velocity often determines market share.

A New Insight: Administrative Drag Distorts Risk Appetite

There’s another overlooked consequence.

When underwriters are overloaded with non-core tasks, cognitive bandwidth shrinks. Under pressure, professionals naturally gravitate toward simpler, lower-friction risks.

Complex, nuanced submissions—those requiring deeper analysis—may receive less enthusiasm or slower response.

Over time, this can subtly reshape portfolio composition:

- Simpler risks get prioritized.

- Complex risks are declined or delayed.

- True underwriting differentiation diminishes.

Hidden underwriting capacity loss doesn’t just reduce output—it can gradually alter risk selection behavior.

That’s a portfolio management issue, not just an operational one.

Claims Operations Reflect the Same Pattern

The same structural drag exists in claims.

Adjusters often spend significant time:

- Reviewing unstructured documents

- Reconciling medical bills

- Navigating multiple claims platforms

- Revalidating previously entered information

According to 2025 U.S. operational research from Accenture, breaking down claims silos could unlock over $100 billion in efficiency gains nationwide.

When adjusters spend disproportionate time on administrative reconciliation, policyholder communication suffers.

And in a social media-driven environment where service failures escalate quickly, that becomes a reputational risk.

The Workforce Dimension

Hidden underwriting capacity loss also impacts talent sustainability.

The next generation of insurance professionals expects streamlined digital workflows. When 30–40% of their day is consumed by system navigation and data duplication, engagement declines.

This contributes to:

- Burnout in high-volume underwriting units

- Increased claims turnover

- Difficulty attracting analytical talent

Operational friction becomes a cultural liability.

Making the Invisible Visible

Most carriers track output. Few track time allocation by task category.

To address hidden underwriting capacity loss, leadership must:

- Conduct structured workflow mapping from submission intake to bind.

- Categorize tasks into core vs. non-core activities.

- Quantify time spent in data entry, search, reconciliation, and exception handling.

- Identify repeat friction patterns across regions and product lines.

Only then can investments in integration, AI-driven document processing, or workflow redesign be precisely targeted.

Without measurement, transformation budgets risk solving symptoms instead of root causes.

The Strategic Imperative

In a U.S. market defined by margin pressure, climate volatility, and distribution competition, insurers cannot afford to let 30–40% of underwriting and claims capacity disappear into operational shadows.

Hidden underwriting capacity loss is not a minor inefficiency.

It is a structural constraint on growth.

It is a subtle driver of portfolio distortion.

It is a contributor to talent fatigue.

The carriers that lead over the next decade will not just invest in better models or smarter pricing algorithms.

They will eliminate the invisible work that prevents their underwriting and claims professionals from operating at full strength.

Because sometimes the most significant risk exposure isn’t in your book of business.

It’s in your workflow.

Sign in to leave a comment.