Taxation, by its very nature, can appear burdensome. Yet within its intricate framework lies a powerful mechanism designed to alleviate liability—tax credits. For individuals and businesses alike, understanding What is a Tax Credit is essential for optimizing financial outcomes and ensuring efficient compliance.

A tax credit directly reduces the amount of tax owed, unlike deductions which merely lower taxable income. This distinction is pivotal. While deductions operate indirectly, credits provide a more immediate and impactful reduction, often making them a cornerstone of effective US Tax planning.

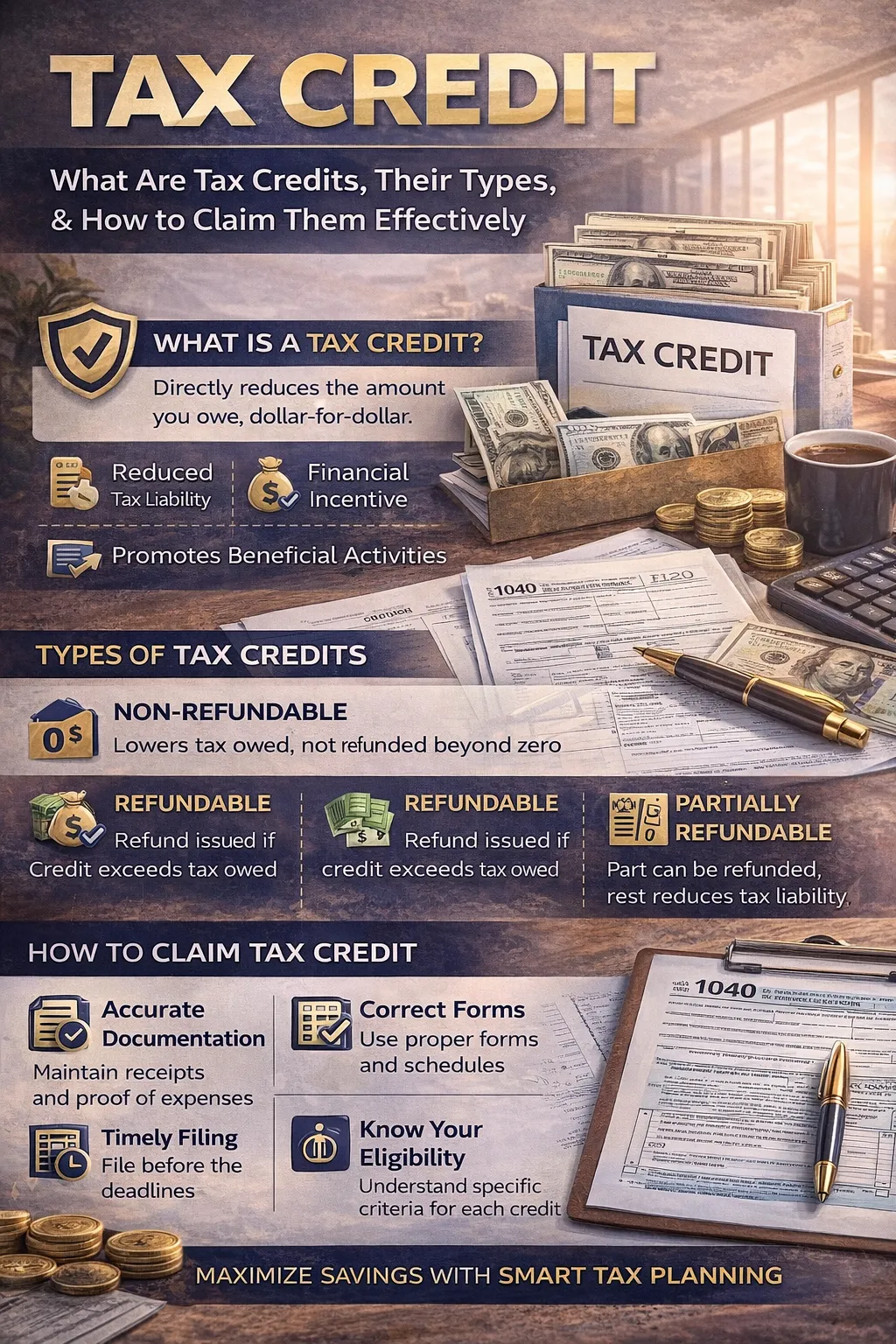

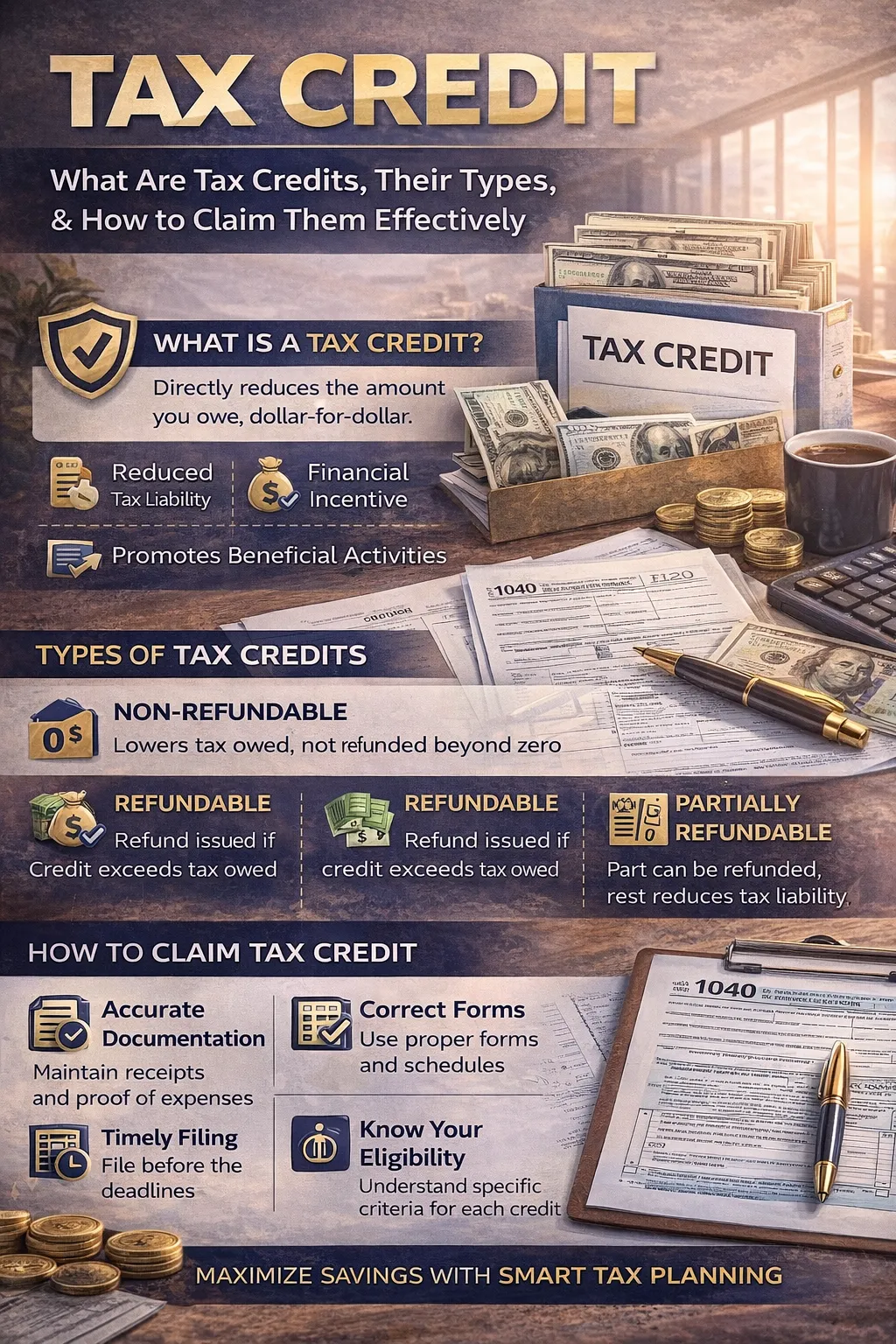

What is a Tax Credit?

At its core, a tax credit is a fiscal incentive granted by the government to encourage specific economic behaviors. These may include education, energy efficiency, childcare, or investment activities. When applied, a tax credit diminishes the taxpayer’s liability dollar-for-dollar.

For example, if an individual owes $5,000 in taxes and qualifies for a $1,000 credit, the final liability reduces to $4,000. Simple. Potent. Financially advantageous.

Understanding What is a Tax Credit is not merely academic—it is a practical necessity for those seeking to minimize tax exposure while remaining compliant with regulatory frameworks.

Types of Tax Credits

Not all tax credits are created equal. They vary in structure, applicability, and financial impact. Exploring the Types of Tax Credits reveals how diverse and nuanced these instruments can be.

1. Non-Refundable Tax Credits

These credits can reduce a taxpayer’s liability to zero but not beyond. If the credit exceeds the tax owed, the excess is forfeited. Common examples include education-related credits and certain energy-efficient home improvements.

2. Refundable Tax Credits

More advantageous in many scenarios, refundable credits allow taxpayers to receive a refund even if the credit surpasses their total tax liability. This makes them particularly beneficial for lower-income individuals.

3. Partially Refundable Credits

These occupy a middle ground, where a portion of the credit may be refunded while the rest functions as non-refundable. Such hybrid structures add complexity but also flexibility.

Understanding the Types of Tax Credits enables taxpayers to strategically align their financial decisions with available benefits, thereby enhancing overall tax efficiency.

How to Claim Tax Credit Effectively

The process of claiming tax credits is not inherently difficult, but it demands precision. Knowing How to Claim Tax Credit properly can mean the difference between legitimate savings and costly errors.

Accurate Documentation

Every claim must be substantiated with verifiable records. Receipts, invoices, and official statements serve as the evidentiary backbone of a valid claim.

Correct Form Selection

Different credits require specific forms and schedules. Filing the wrong form, or omitting a required one, can invalidate the claim entirely.

Timely Filing

Deadlines matter. Missing filing timelines can result in the forfeiture of eligible credits, regardless of qualification.

Understanding Eligibility Criteria

Each credit comes with its own set of conditions—income thresholds, expenditure categories, and residency requirements. Misinterpreting these can lead to disallowed claims or audits.

Mastering How to Claim Tax Credit involves a blend of diligence, awareness, and procedural accuracy.

The Role of Tax Credits in US Tax Planning

Tax credits are not isolated benefits; they are integral to a broader financial strategy. Within the domain of US Tax planning, they serve as tactical instruments to reduce liabilities while aligning with long-term objectives.

For instance, investing in renewable energy systems not only contributes to sustainability but also unlocks valuable tax credits. Similarly, educational pursuits or dependent care expenses can be structured to maximize available credits.

Strategic planning ensures that taxpayers do not merely react to tax obligations but proactively shape them. In this context, tax credits function as levers—subtle yet powerful—within a well-orchestrated financial plan.

Common Mistakes to Avoid

Despite their advantages, tax credits are often underutilized or misapplied. Common pitfalls include:

- Overlooking eligible credits due to lack of awareness

- Claiming credits without proper documentation

- Misinterpreting eligibility requirements

- Failing to coordinate credits with overall US Tax planning

Such errors can lead to missed opportunities or, worse, compliance issues. A meticulous approach is essential.

Conclusion

Tax credits represent one of the most effective tools for reducing tax liability in a lawful and strategic manner. By understanding What is a Tax Credit, exploring the various Types of Tax Credits, and mastering How to Claim Tax Credit, taxpayers can significantly enhance their financial efficiency.

When integrated thoughtfully into US Tax planning, these credits transform from simple incentives into powerful financial instruments. Precision, awareness, and strategic foresight remain the keys to unlocking their full potential.

Sign in to leave a comment.