What Is the 4% Rule? The Retirement Withdrawal Strategy Explained And Why Many Retirees Misunderstand It

If you search "what is the 4% rule" most articles give the same basic definition. Withdraw 4 percent of your retirement savings in your first year of retirement, adjust that amount upward for inflation each year afterward, and your savings may last approximately 30 years.

That explanation is technically accurate. It is also incomplete.

Most of what you find online fails to explain why the rule was originally created, when it tends to break down, how inflation and poor market timing can affect it, what sequence of returns risk actually means in practice, why many retirees never actually follow it the way it was designed, and how retirement income thinking has evolved well beyond it in recent years.

At Apex Retirement Services in Stoneham, we believe retirement education should cover all of those gaps rather than just the headline. This guide walks through what the 4% rule actually is, where it came from, what its real limitations are, and how it fits into a broader conversation about building a retirement income strategy designed for your specific situation.

What Is the 4% Rule in Retirement?

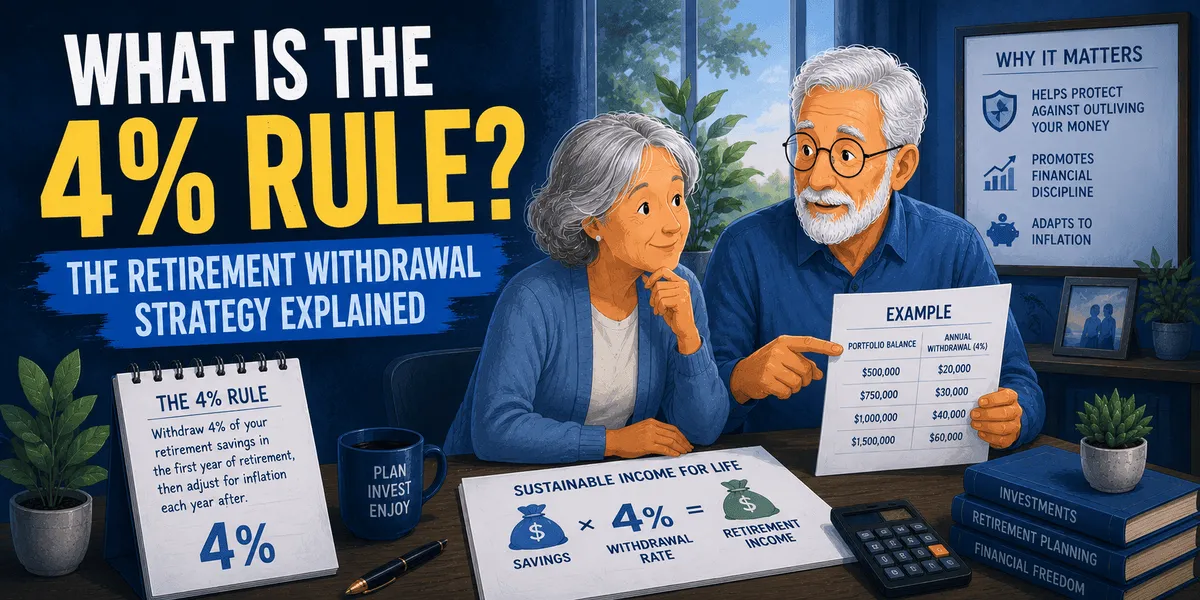

The 4% rule is a retirement withdrawal guideline developed through the research of William Bengen, a financial researcher, in 1994. The core idea is straightforward. In your first year of retirement, you withdraw 4 percent of your total retirement savings. In each following year, you take that same dollar amount and adjust it upward to account for inflation. The goal is for this approach to support your spending needs across an approximately 30-year retirement.

As a simple illustration, if you retire with $1,000,000 in retirement savings, your first year withdrawal under this approach would be $40,000. If inflation in year two runs at 3 percent, you would not recalculate 4 percent of your current balance. Instead you would take last year's $40,000 and add 3 percent, bringing your year two withdrawal to $41,200. The year after that the same adjustment applies to $41,200, and so on.

This inflation-adjusted dollar amount approach is what makes the 4% rule meaningfully different from simply withdrawing 4 percent of whatever your balance happens to be each year. The withdrawal amount follows inflation, not your portfolio value.

Where the 4% Rule Came From

One of the most important things missing from most explanations of the 4% rule is an honest account of its origins and what it was actually designed to do.

Bengen analyzed decades of U.S. market history and tested how different withdrawal rates held up across a wide range of historical conditions including recessions, high-inflation periods, major market downturns, and varying start dates for retirement. His research found that retirees using a diversified portfolio approach could historically withdraw around 4 percent in their first year, with inflation adjustments each year after, without exhausting their savings over a 30-year retirement in most historical scenarios. This research later influenced what became known as the Trinity Study, which further examined and popularized the concept.

But what most summaries leave out is what the original research assumed. It was built around a roughly 30-year retirement timeframe, U.S. historical market performance, disciplined investing behavior, and consistent withdrawal patterns. It was never intended to be universal, guaranteed, or immune to changing conditions. It was a planning benchmark grounded in historical data, and like all historical benchmarks, it carries important caveats when applied to individual situations.

The Most Common Misunderstanding

Many people who have heard of the 4% rule incorrectly believe it means withdrawing 4 percent of whatever their portfolio is worth each year. That is not how the original approach works and the distinction matters considerably.

The actual strategy calls for withdrawing 4 percent only in year one and then continuing to withdraw that same inflation-adjusted dollar amount in subsequent years regardless of what the portfolio is doing. So even in a year when the market declines and your portfolio balance is lower, the withdrawal amount continues to adjust upward for inflation rather than downward to match portfolio performance.

This is precisely why poor market timing in the early years of retirement can create serious problems. You are withdrawing an inflation-adjusted amount from a balance that may already be declining, which can permanently affect how much your savings have the opportunity to recover from.

The Real Risk: Sequence of Returns

This is the most important concept in the entire 4% rule conversation and the one most commonly glossed over.

Sequence of returns risk refers to the danger of experiencing poor market returns early in retirement when you are actively drawing income from your savings. Two retirees can share identical average long-term returns over a 20-year retirement and end up in dramatically different financial positions simply because of the order in which those returns arrived.

Consider a simplified illustration. Two retirees, call them Carol and David, both retire with $600,000 and both experience the same average annual return over 20 years. Carol's early retirement years happen to coincide with a period of market growth. Even as she withdraws, her balance has an opportunity to build. David retires into a downturn. His early withdrawals come from a declining balance, and even when markets recover in later years he is recovering from a significantly smaller pool than where he started.

After 20 years, despite identical average returns, David's retirement savings may be substantially depleted compared to Carol's or potentially exhausted entirely. The sequence of returns, not the average, made all the difference. This is why a retirement income strategy built entirely around market-dependent withdrawals may benefit from additional income sources that do not depend on market performance.

Why the 4% Rule Is Being Reconsidered Today

Retirement researchers and planning professionals have raised a number of concerns about whether the original 4% benchmark remains as reliable under today's conditions as it was historically.

Retirements are lasting longer than they did when the original research was conducted. Many people today retire in their late 50s or early 60s and may live well into their 80s or 90s, creating retirement timelines of 35 to 40 years or more. The original research was built around a 30-year window, and extending that significantly changes the sustainability picture.

There are also ongoing discussions among researchers about whether future market returns may be lower than the historical averages the original rule was built on. If the growth environment is more modest going forward, portfolios may face more pressure supporting the same level of inflation-adjusted withdrawals over time.

Healthcare costs represent another variable the original rule did not fully account for. Medicare premiums, supplemental coverage, prescription expenses, and the potential cost of long-term care can all increase significantly in later retirement years, adding meaningful pressure to a withdrawal plan that was not designed around those realities.

Perhaps most practically, the original rule assumes relatively consistent year-to-year spending. In reality most retirees spend more actively in their early retirement years when they are traveling and pursuing long-deferred goals, spend somewhat less in the middle years, and then often see costs spike again later in retirement due to healthcare. A retirement income strategy built around real spending patterns may serve some retirees better than one built on a straight-line assumption.

Flexible Approaches to Retirement Income Planning

Because of these limitations, retirement income planning has moved increasingly toward flexibility rather than rigid formulas. Several approaches have developed that may address some of the 4% rule's weaknesses.

A guardrails approach adjusts spending when the portfolio rises or falls significantly, allowing for a modest increase in withdrawals during strong periods and a temporary reduction during difficult ones. This kind of dynamic adjustment may improve the long-term durability of a retirement income plan compared to holding rigidly to a fixed inflation-adjusted dollar amount.

A bucket strategy separates retirement assets into different pools with different time horizons, keeping near-term spending needs in more stable, accessible accounts while longer-term assets remain positioned for growth. This approach is designed to reduce the pressure of drawing from growth-oriented assets during a downturn.

An income floor strategy builds a foundation of reliable income from sources that are not dependent on market performance, things like Social Security, pension income where applicable, and insurance-based annuity solutions, and then uses market-linked savings for discretionary and lifestyle spending above that floor. Any guarantees associated with insurance-based income products are backed by the claims-paying ability of the issuing insurance company.

Does the 4% Rule Include Social Security?

This is a question that most explanations of the 4% rule barely address. In most cases, no. The 4% rule as originally conceived applies specifically to investment withdrawals. Additional income sources including Social Security, pension income, part-time work, and insurance-based annuity solutions are generally treated separately.

This is actually one of the most important planning opportunities many retirees overlook. If a meaningful portion of your essential monthly expenses can be covered by income sources that are not tied to market performance, the portion of your savings that needs to support a 4 percent-style withdrawal may be significantly smaller. That can reduce sequence of returns risk and improve the overall durability of the plan.

Social Security timing in particular is one of the most powerful levers available to retirees. Optimizing when you claim, and how that timing coordinates with your spouse's situation and your other income sources, can meaningfully reduce the pressure on your retirement savings year after year.

The 25x Rule: A Related Planning Benchmark

Closely connected to the 4% rule is a savings target concept sometimes called the 25x rule. It works simply. If you take your expected annual retirement expenses and multiply them by 25, the result is a rough estimate of the savings target that might support a 4 percent-style withdrawal over a 30-year retirement.

As a general illustration, if your expected annual retirement expenses are $80,000, the 25x calculation suggests a savings target of approximately $2,000,000. This is a useful planning benchmark for thinking about whether you are on track, though like the 4% rule itself it does not account for Social Security income, pension benefits, tax considerations, or the specific shape of your retirement spending. Please consult a CPA or independent tax professional for guidance specific to your situation.

Where the 4% Rule May Be Useful and Where It May Fall Short

As a general planning benchmark for estimating sustainable withdrawal levels, the 4% rule can be a helpful starting point. It tends to be most applicable as a guideline for retirees who retire near traditional retirement age, have access to other income sources beyond their savings, are willing to remain flexible with spending during difficult market periods, and are not carrying unusually high fixed expenses.

The guideline may be less reliable as a standalone approach for people retiring significantly earlier than traditional retirement age, where the time horizon extends well beyond 30 years. It may also be more challenging for those with large fixed healthcare expenses, those planning retirements that depend entirely on investment withdrawals without any other income sources, or those who are less comfortable with the possibility of adjusting spending during difficult market periods.

What Many Retirees Actually Do

Something that rarely comes up in discussions of the 4% rule is how real retirees actually behave. In practice, most people do not follow a rigid inflation-adjusted fixed withdrawal formula indefinitely. When markets decline, many retirees naturally reduce discretionary spending, delay larger purchases, or temporarily work part-time. When conditions are good they may spend more freely. This kind of natural flexibility is one reason some retirees navigate retirement successfully even when the mathematical projections might suggest otherwise.

The lesson is not that the 4% rule is wrong. It is that retirement income planning works best when it is built around flexibility, multiple income sources, and a structure that does not require perfect market conditions to hold together.

How Apex Retirement Services Thinks About This

At Apex Retirement Services, we think the 4% rule is one of the most useful educational concepts in retirement planning, and one of the most misapplied. Its greatest value is as a starting point for a larger conversation, not as a plan in itself.

Ryan Skinner works with individuals and families throughout Stoneham, Woburn, Cohasset, Tyngsboro, and the broader Greater Boston area to help build retirement income structures that go beyond any single formula. That means looking at Social Security timing, insurance-based income solutions that may provide a reliable retirement paycheck regardless of market conditions, and coordination with independent investment advisors and CPAs who can address the full picture.

The Apex Retirement Blog is built on the belief that better-informed retirees make better decisions. This is that information, as clearly and honestly as we can put it.

▶ Schedule a Complimentary Retirement Income Consultation

Frequently Asked Questions

What is the 4% rule and how does it work?

The 4% rule is a guideline for retirement withdrawals, suggesting retirees withdraw 4% of their savings in the first year and adjust that amount for inflation in subsequent years. For example, if you have $1,000,000 saved, you would withdraw $40,000 in the first year and increase that amount based on inflation each year thereafter.

What are the limitations of the 4% rule?

The 4% rule is based on historical market performance and assumes a 30-year retirement timeline, which may not apply to everyone today. It does not account for factors like extended retirement periods, healthcare costs, or changes in market conditions, meaning it can be less reliable for those facing different circumstances.

What is sequence of returns risk?

Sequence of returns risk refers to the potential negative impact on retirement savings when poor market performance occurs early in retirement. If retirees withdraw funds from a declining balance, it can significantly deplete their savings, making recovery difficult even when markets improve later on.

Does the 4% rule include Social Security benefits?

Typically, the 4% rule does not include Social Security benefits; it focuses solely on investment withdrawals. However, integrating Social Security and other income sources can reduce the amount you need to withdraw from savings, potentially minimizing the risks associated with market fluctuations.

Is the 4% rule still relevant for today's retirees?

While the 4% rule can still serve as a useful starting point, many retirement planners advocate for more flexible strategies considering longer life expectancies and fluctuating market conditions. Personalized retirement income analysis is essential to determine the best approach for individual circumstances.

How can retirees adapt the 4% rule to their needs?

Retirees can adapt the 4% rule by incorporating flexible withdrawal strategies, such as adjusting spending based on market performance or using a bucket strategy to separate assets by time horizon. This adaptability can help manage risks and align withdrawals with personal spending patterns.

What is the 25x rule in relation to the 4% rule?

The 25x rule is a related concept suggesting that to support a 4% withdrawal rate, retirees should aim to have 25 times their expected annual expenses saved. For instance, if you anticipate needing $80,000 annually in retirement, you should strive for a $2,000,000 savings target.

Sign in to leave a comment.