You finally have the money to pay off your business loan ahead of schedule. Maybe your sales have been exceptional this year. Maybe you just closed a big deal. Maybe you are refinancing to lock in a better rate. Whatever the reason, you are ready to get out from under that debt and move forward.

But before you make that call to your lender, there is something you need to know. Paying off an SBA loan early is not always as simple or as cheap as it sounds. Hidden fees called prepayment penalties can cost you thousands of dollars if you move without understanding the rules first.

This article breaks down everything you need to know in plain language so you can make the smartest financial decision for your business.

The Fee Nobody Warns You About

When most business owners take out an SBA loan, their focus is on getting approved. They look at the interest rate, the monthly payment, and the loan term. Very few people spend time reading the prepayment penalty clauses buried in their loan documents.

That oversight can be expensive.

A prepayment penalty is a fee your lender charges when you pay off a significant portion of your loan before the scheduled term ends. The logic is straightforward. When your lender approved your loan, they built their business model around receiving interest payments over the full term. When you pay early, they lose that future income. The penalty is their way of recovering some of that loss.

The SBA Standard Operating Procedures govern exactly how these penalties are structured across all participating lenders, which means the rules are consistent regardless of which bank or credit union originated your loan.

Two Programs, Two Very Different Penalty Structures

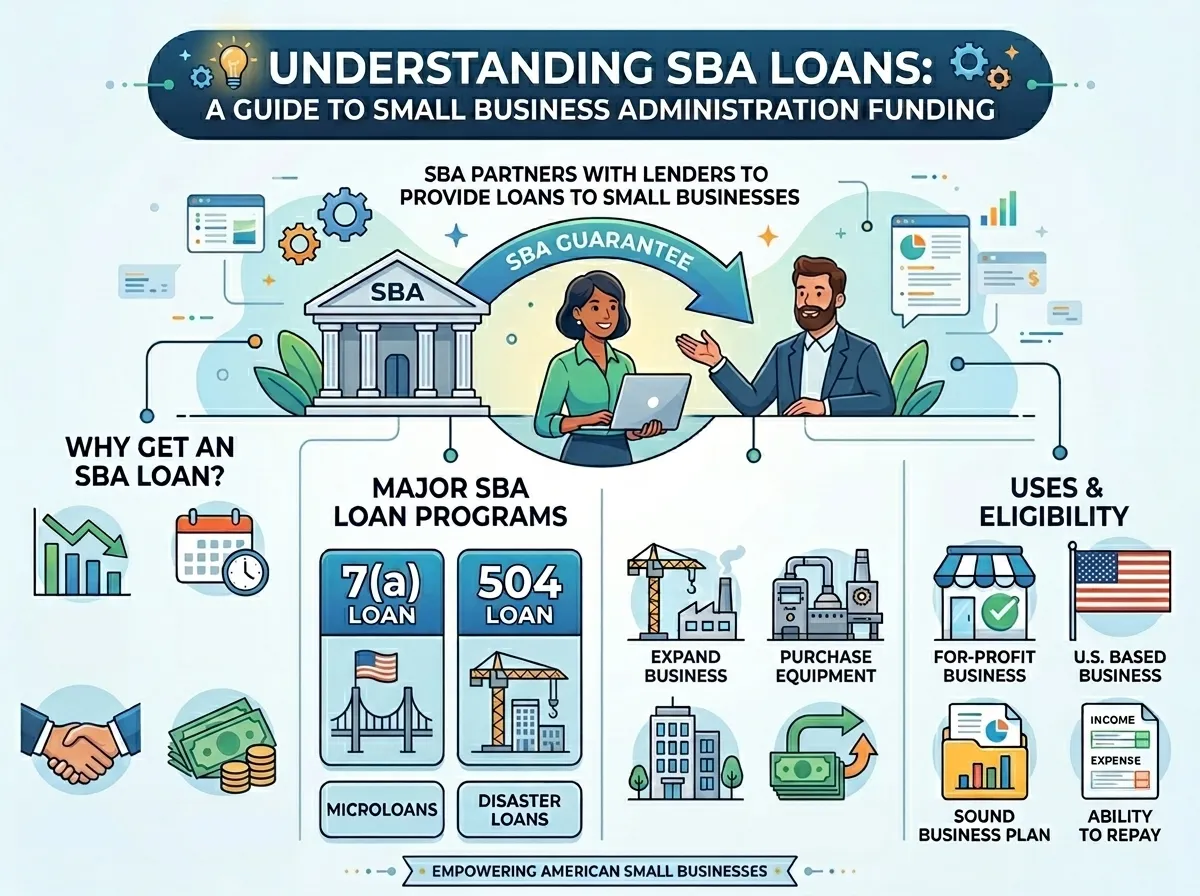

The SBA offers multiple loan programs but the two most commonly used are the 7(a) and the 504. Each has its own prepayment rules and understanding the difference between them is critical before making any early payoff decision.

The SBA 7(a) loan is the most flexible and widely used program. It covers working capital, equipment, business acquisitions, and commercial real estate. The prepayment penalty on a 7(a) loan is limited and relatively short-lived.

The penalty only kicks in when three things are true at the same time. Your loan term must be 15 years or longer. You must be paying off 25% or more of the outstanding balance in a single transaction. And you must be doing this within the first three years of receiving the funds.

If all three conditions apply, you pay 5% of the prepayment amount in year one, 3% in year two, and 1% in year three. After year three, there is no penalty regardless of how much you pay off or how quickly you do it.

The SBA 504 loan is a different story entirely. This program is designed specifically for commercial real estate and heavy equipment purchases. It involves a first mortgage from a conventional lender and a second loan from a Certified Development Company backed by the SBA.

The prepayment penalty on the CDC portion of a 504 loan runs for a full 10 years. It follows a declining schedule that starts at its highest point in year one and decreases by roughly 10% each year until it reaches zero after year ten. The exact penalty amount is calculated using the remaining CDC balance, the debenture rate on your specific bond, and the year factor corresponding to where you are in the loan timeline.

For a detailed breakdown of how each calculation works with real numbers, the official SBA 504 loan program page provides the foundational framework that all lenders are required to follow.

A Real World Example That Changes How You Think About This

Here is a scenario that plays out regularly for business owners across the country.

A restaurant owner in year two of a 500,000 dollar SBA 7(a) loan sees interest rates drop. A new lender offers a rate that is one full percentage point lower. The owner gets excited about the savings and moves quickly to refinance.

What the owner did not calculate before pulling the trigger is the prepayment penalty. Paying off the full remaining balance of around 470,000 dollars in year two triggers the 3% penalty. That comes out to approximately 14,100 dollars paid upfront just to exit the original loan.

The interest savings from the new lower rate amount to about 4,700 dollars per year. That means the owner needs to keep the new loan for at least three full years just to break even on the refinancing decision. If the business is sold or refinanced again before that three-year mark, the whole move was a net financial loss.

This is not an unusual outcome. It is a predictable one that proper planning can easily avoid.

The Strategies That Actually Work

Knowing the rules opens up a range of practical strategies that can help you minimize or completely avoid prepayment penalty exposure.

The single most effective strategy for 7(a) borrowers is timing. If you are in year one or year two and you are considering paying off or refinancing, running the numbers on waiting is almost always worth the exercise. In many cases, waiting 12 to 18 additional months to clear the three-year penalty window saves more money than the benefit of the early payoff or refinance.

For borrowers who want to aggressively pay down their 7(a) loan without triggering the penalty threshold, keeping each voluntary prepayment under 25% of the outstanding balance is a useful tool. The penalty is only triggered when a single payment equals or exceeds that threshold. Spreading your extra payments over multiple transactions throughout the year can accomplish the same debt reduction goal without any penalty cost.

For 504 borrowers who are selling their commercial property, exploring loan assumption with your lender is worth the conversation. When a qualified buyer assumes the existing 504 loan rather than paying it off, no prepayment penalty is triggered. Both buyer and seller can benefit from this structure, especially in the early years of the loan when the penalty would otherwise be highest.

The Consumer Financial Protection Bureau resource on prepayment penalties provides helpful general guidance on how these clauses work across different loan types and what questions every borrower should ask before signing any financing agreement.

When Flexibility Matters More Than Rate

SBA loans earn their reputation for a reason. The interest rates are competitive, the terms are long, and the down payment requirements are lower than most conventional commercial financing. For business owners who plan to hold their property or maintain their loan for the full term, SBA programs are often the best tool available.

But flexibility has value too. And SBA loans are not built for business owners who want the freedom to pivot quickly, refinance opportunistically, or pay down debt aggressively without consequence.

If you anticipate selling your commercial property within five years, if you expect your business cash flow to allow large paydowns within the first few years, or if you simply want the freedom to exit your loan without penalty at any time, there are alternative financing options worth considering seriously.

Bridge loans, DSCR loans, stated income loans, and hard money programs offered through private lenders are typically structured with much more flexible prepayment terms. Some carry no prepayment penalty at all. The tradeoff is usually a higher interest rate, but for borrowers who value flexibility over rate, that tradeoff is often worth making from the beginning rather than discovering its value the hard way after an expensive penalty.

Consulting a commercial lending specialist who understands both the SBA framework and the private lending landscape gives you the clearest picture of which option actually serves your business goals. The SCORE financial planning resources for small business owners are also a useful starting point for building the kind of financial model that helps you evaluate these decisions with real numbers rather than gut feeling.

One Step You Must Take Before Anything Else

Regardless of which path you choose, there is one action that must happen before any early payoff or refinancing decision is finalized. Request an official payoff quote from your lender.

A payoff quote is a formal document that shows the exact total amount required to close out your loan on a specific date. It includes the remaining principal, accrued interest, any administrative fees, and the prepayment penalty if one applies. The number in this document is the only number that matters when evaluating your decision.

Never rely on your own back-of-envelope calculation of the penalty. The debenture rate, accrued interest timing, and fee structure can produce a different final number than even a careful estimate. The official quote eliminates that uncertainty.

Give your lender 21 to 30 days notice when requesting a payoff quote. Keep written records of all communication. And once you receive the quote, compare the total cost of exiting against the total financial benefit of doing so before making any final commitment.

For business owners who want expert guidance navigating these decisions, working with a lender who specializes in both SBA and alternative commercial financing ensures you have the full picture before committing to any path. Understanding all available SBA and business loan options side by side is the most reliable way to make a decision you will not regret later.

Final Word

SBA loans are powerful tools. The prepayment penalty is not a flaw in the program. It is a disclosed feature that exists for legitimate reasons and that works fine for business owners who plan accordingly.

The business owners who get hurt by it are almost always the ones who moved too fast without running the numbers first. Take the time to understand exactly where you stand in your loan term, calculate the real cost of any early exit, and compare that against the real benefit of the move you are considering.

Sometimes the smartest financial decision is the one you wait to make.

Sign in to leave a comment.