If you took out a small business loan in the last several years, chances are you have thought about paying it off early. Maybe your revenue has grown faster than expected, or you want to refinance at better terms. Either way, there is an important cost that catches many business owners off guard: the prepayment penalty.

Before you make any early payoff decisions, understanding how these fees work can save you thousands of dollars and help you plan smarter.

What Is a Prepayment Penalty on a Business Loan?

A prepayment penalty is a fee charged by lenders when a borrower pays off a loan ahead of its scheduled term. The logic is simple: lenders earn money through interest over the life of a loan. When you pay early, they lose that future income. The penalty is designed to recover some of that loss.

Prepayment penalties are not unique to government-backed loans. They appear across commercial real estate loans, auto financing, and personal business loans. However, many borrowers are surprised to find them in SBA loan agreements because they assume government-backed programs are more flexible. In reality, the rules vary significantly depending on which SBA program you used, the loan amount, and when you decide to pay it off. A detailed breakdown of exactly how these fees work is covered in this guide on SBA Loan Prepayment Penalty, including specific calculations for both SBA 7(a) and 504 programs.

How the SBA 7(a) Prepayment Penalty Works

The SBA 7(a) loan is the most commonly used government-backed business loan in the United States. According to the U.S. Small Business Administration, these loans can be used for working capital, equipment purchases, business acquisition, and real estate.

The prepayment penalty on an SBA 7(a) loan only kicks in under specific conditions. First, the loan must have a term of 15 years or longer. Second, you must prepay 25 percent or more of the outstanding balance in a single payment. If both conditions are met during the first three years of the loan, the following penalty schedule applies:

Year 1: 5 percent of the prepayment amount

Year 2: 3 percent of the prepayment amount

Year 3: 1 percent of the prepayment amount

After year three, or for loans with terms shorter than 15 years, there is no prepayment penalty at all. So if you can wait, the cost disappears entirely.

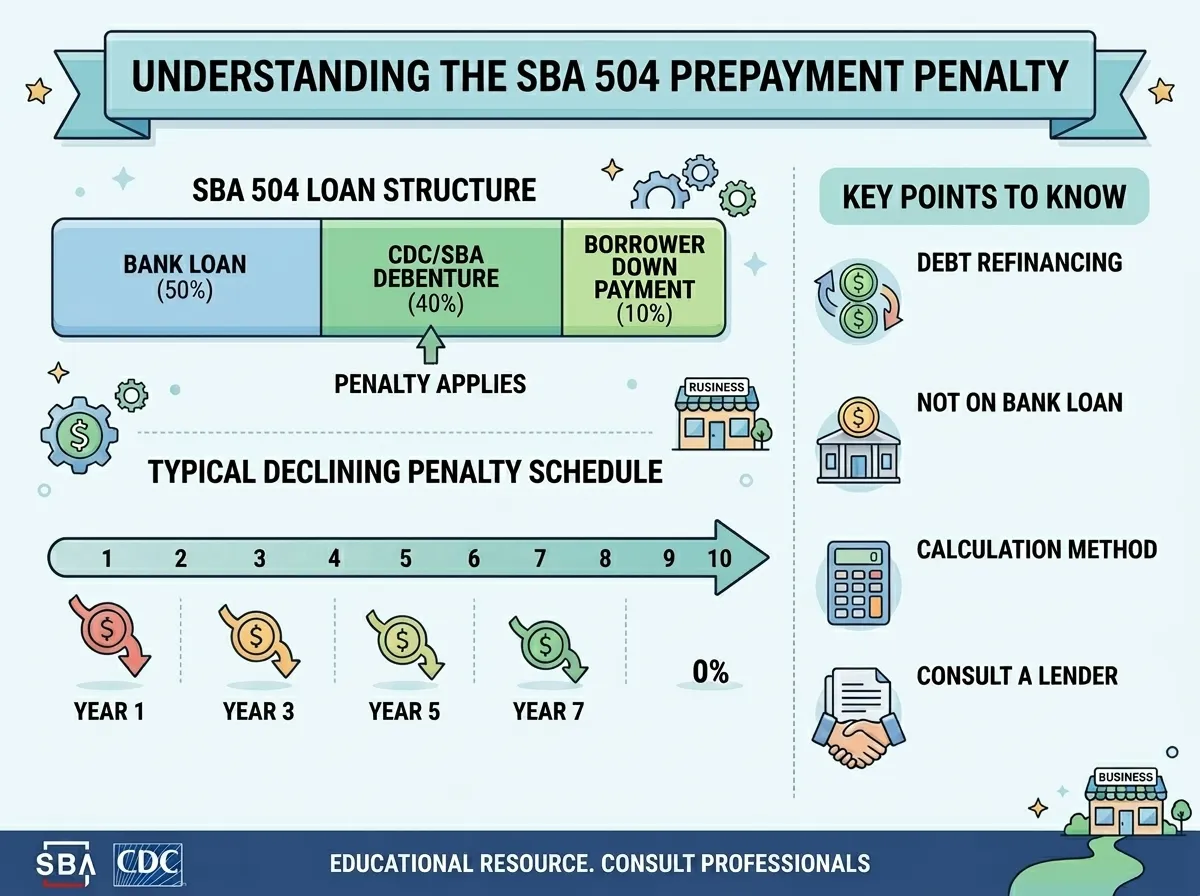

How the SBA 504 Prepayment Penalty Works

The SBA 504 loan program is designed primarily for fixed asset purchases like commercial real estate and large equipment. The Consumer Financial Protection Bureau notes that fixed-rate loan products commonly carry prepayment fees because lenders use bond funding to back them, and early repayment disrupts those structures.

The SBA 504 prepayment penalty is stricter than the 7(a) version. It applies to the CDC portion of the loan, which is typically 40 percent of the total project cost, and it can last up to 10 years. The penalty follows a declining schedule sometimes called the 10-9-8 method, where the penalty factor decreases by one point each year based on the debenture rate and remaining balance.

For example, if you have $400,000 remaining on the CDC portion of a 504 loan at a 4 percent debenture rate and you pay it off in year three, the calculation would look like this: $400,000 multiplied by 4 percent, multiplied by the year-three factor of 0.80, equals a $12,800 penalty. This is why SBA 504 loans require careful long-term planning before signing.

Who Gets Hurt Most by Prepayment Penalties?

Business owners who are most exposed to prepayment penalty costs typically fall into one of three categories.

The first group includes owners who refinance shortly after closing. When interest rates drop or a better financing option becomes available, the instinct is to refinance quickly. But doing so within the penalty window can eliminate the financial benefit entirely.

The second group includes sellers. When a business changes hands and the new owner does not want to assume the existing debt, the seller may be forced to trigger a payoff that comes with a significant penalty during the transfer.

The third group includes real estate investors who used SBA 504 financing for property purchases and later want to refinance into conventional or private lending products. The 10-year penalty window on the 504 program makes this a costly move if done too early.

According to SCORE, one of the most common financial mistakes small business owners make is failing to read the full terms of their loan agreements, particularly around early repayment costs.

How to Reduce or Avoid Prepayment Penalties

There are several practical ways to manage or avoid these costs. The Federal Reserve's small business credit survey consistently shows that borrowers who compare loan terms before signing are far less likely to face unexpected costs during repayment.

Here are some strategies worth considering:

Wait out the penalty period. For SBA 7(a) loans, you only need to wait three years. For 504 loans, the window is longer, but the penalty shrinks each year.

Make smaller partial payments. For 7(a) loans, the penalty only applies if you prepay 25 percent or more of the balance in a single payment. Strategic smaller payments below that threshold can reduce your balance without triggering the fee.

Request a formal payoff quote. Before making any decision, always get an official payoff figure from your lender or CDC. The exact penalty amount depends on your specific loan documents and current rates.

Explore loan assumption. If you are selling a property, the buyer may be able to assume the existing loan rather than forcing a full payoff.

Consider alternative loan products from the start. If you anticipate needing flexibility, bridge loans, hard money loans, stated income loans, and DSCR programs typically carry no prepayment penalties and close much faster than SBA products.

The National Federation of Independent Business advises small business owners to always evaluate the total cost of financing, not just the interest rate, when comparing loan products.

When a Non-SBA Loan Makes More Sense

SBA loans are excellent tools for the right borrower in the right situation. But they are not the best fit for everyone. If you value speed, flexibility, or anticipate paying off the loan early, other commercial lending products may be a better match.

Bridge loans, for example, are designed for short-term needs and rarely carry prepayment penalties. Hard money loans are asset-based, closing quickly and offering more flexibility around payoff timing. No-doc and stated income programs skip the heavy documentation requirements of SBA applications and often offer more straightforward exit terms.

The right loan depends on your timeline, your property or business type, and how long you plan to hold the debt. Understanding prepayment penalty structures across all your options is the first step toward making a decision that actually works in your favor.

Sign in to leave a comment.