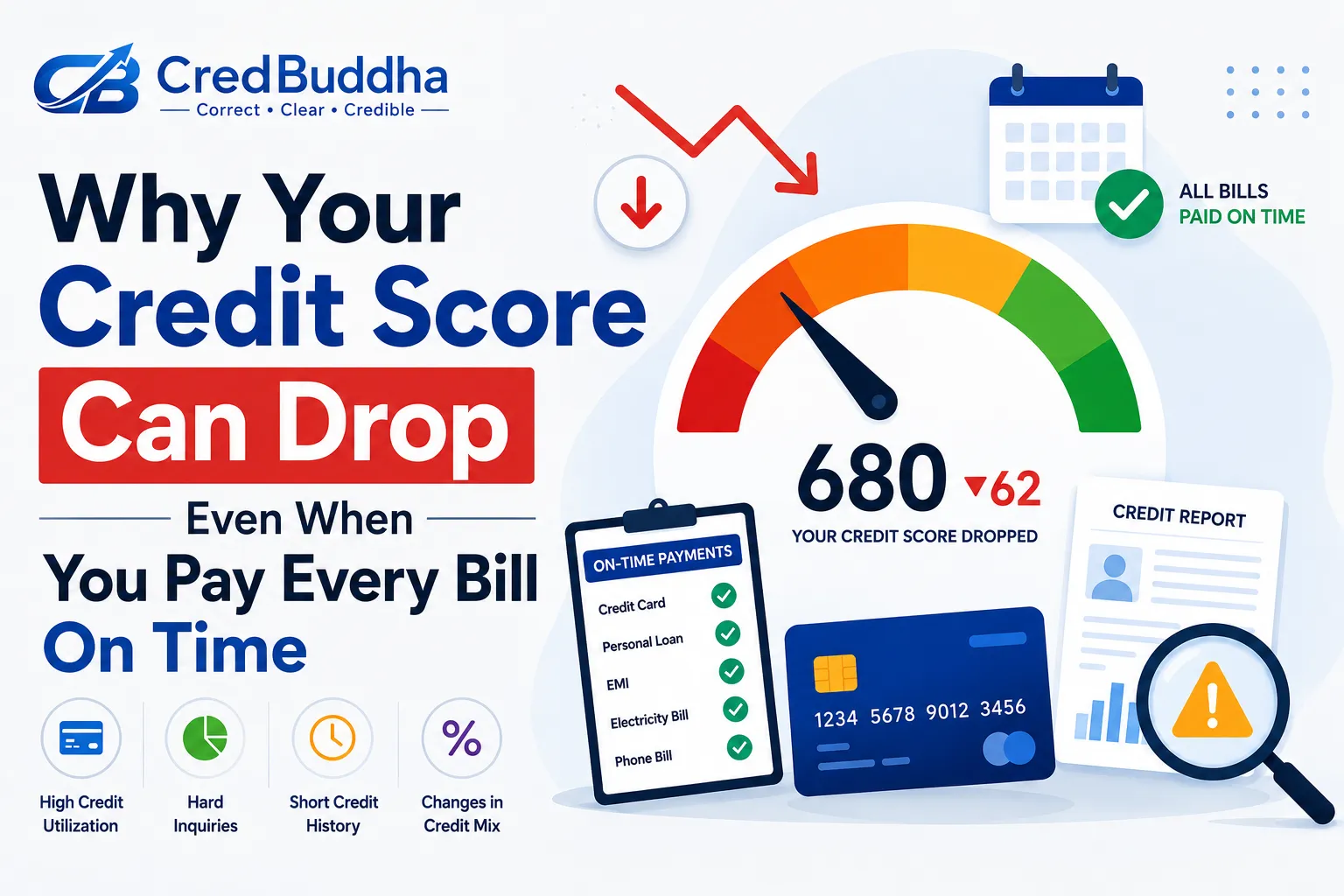

You've done everything right. Every EMI cleared before the due date, every credit card bill paid in full, no defaults, no missed payments. And yet your credit score dips a few points, or worse, drops sharply after a big loan approval. If this has happened to you, you're not imagining it and it's not a system error either. On-time payment is the single biggest factor in your score, but it isn't the only one, and a few of the others work in ways that catch even careful borrowers off guard.

Here are the real reasons this happens and what to actually do about each one.

1. Your credit utilisation jumped, even briefly

Credit utilisation: how much of your total available credit you're using at any given moment — usually carries the second-highest weight after payment history. The tricky part: bureaus often pick up your utilisation on the date your statement is generated, not the date you pay it off.

So if you put a large expense (a flight booking, a gadget, a medical bill) on your card and pay it off in full two weeks later, your statement may still have gone out showing 70-80% utilisation. That snapshot gets reported, your score dips, and it recovers only after the next lower-utilisation statement is reported usually a cycle or two later.

What helps: if you know a big expense is coming, either pay it down before the statement date rather than the due date, or split it across two cards so no single one spikes.

2. You closed an old card

Closing a credit card you no longer use feels like tidying up, but it can quietly hurt two things at once: your average age of credit history, and your total available credit limit (which raises your utilisation percentage even if your spending hasn't changed). A card sitting unused at zero balance is usually doing you more good open than closed unless it charges a fee you're trying to avoid.

3. A hard inquiry landed right when you applied elsewhere

Every time you apply for a new credit card or loan, the lender pulls a hard inquiry, and each one shaves a few points off your score. One inquiry alone is minor. Several in a short window, say, you applied to three banks while comparing offers, reads to the algorithm as a signal of credit hunger, even if you were rejected by none of them.

What helps: compare pre-approved offers and eligibility checks (which use soft inquiries and don't affect your score) before formally applying anywhere.

4. Your credit mix shifted

Bureaus give a small amount of weight to having a mix of credit types — cards, personal loans, and secured loans like car or home loans rather than relying on just one kind. If you closed your only loan account and now carry cards alone, or vice versa, that shift alone can move the needle slightly, even with a perfect payment record.

5. An authorised user or co-applicant's behaviour is dragging you down

If you're an add-on cardholder or a co-applicant on a joint loan, the primary borrower's missed payment or high utilisation can show up on your report too even if you've never missed a payment on your own accounts. This one is easy to miss because the trigger isn't anything you did.

6. There's an error in your credit score report

This is more common than most people assume: a loan that was closed still showing as open, a payment marked late by mistake, or someone else's account attached to your file due to a data-matching error. These don't fix themselves they need to be formally disputed with the bureau.

What helps: pull your report every few months rather than only when you're about to apply for something. Catching an error early means it's resolved well before it affects a loan application you actually care about. Most free credit report checks use a soft inquiry, so reviewing your report regularly won't ding your score.

The pattern behind all of this

None of these six things is about missing a payment. They're about timing and reporting mechanics when a snapshot was taken, how many inquiries landed in a short window, whether an account got closed at the wrong moment. Once you know the mechanics, most of the mystery disappears, and a small, temporary dip stops feeling like something went wrong.

If your score drops and you can't explain it after checking these six, the next step isn't to panic it's to pull your full report and look line by line for what actually changed since the last one.

Sign in to leave a comment.