Every day, professionals at an insurance firm open a spreadsheet. They type in a policy number, cross-check it against various databases, make a note on a sticky tool, and move on to the next task. This process repeats hundreds of times across thousands of insurance enterprises, consuming hours that could be spent on strategy, customer relationships, or policy innovation.

The difference between insurance carriers that flourish and those that hinder increasingly comes down to one aspect: how efficiently they manage the operations. Automated insurance management software solutions transform repetitive workflows into autonomous operations that function in the background, enabling teams to focus on what matters for business growth.

The Silent Cost of Manual Operations

Insurance carriers face a hidden drain on profitability that never appears on balance sheets. Manual processes consume time, introduce errors, and keep skilled employees doing work a system could handle in seconds.

What Manual Operations Actually Cost

Consider the typical workflow for policy renewal at a mid-sized carrier:

- An underwriter pulls data from the policy management system.

- They export it to Excel for calculations and adjustments.

- A coordinator manually enters updates back into the system.

- The second person verifies the entries.

A notice gets printed, physically signed, and mailed to the customer.

This process takes three to five days. Multiply that by hundreds of policies monthly, and you're talking about thousands of wasted hours annually. Employees capable of analyzing risk and building relationships instead spend their time as data entry clerks.

The financial impact extends beyond labor costs.

Manual data entry creates inaccuracies. A policy data typed inaccurately in your system can lead to errors in billing, compliance, and customer services.

For insurance startups, this challenge is even more acute. An insurtech firm with a few workforce can't afford to have even one person organizing spreadsheets and manual data transfers. They require every team member focused on product development, customer acquisition, or underwriting innovation.

The Efficiency Gap Between Leaders and Laggards

It is evident that carriers using legacy systems spend most of their operational budget on back-office functions. Carriers using automated insurance management software systems reduce these expenses. That difference translates directly to reinvestment capacity, competitive pricing power, and profit margins.

The top-performing carriers understand this equation. They invest in insurance software systems that handle repetitive, rule-based work automatically. Their teams focus on exceptions and strategy. Their customers experience faster responses and fewer errors.

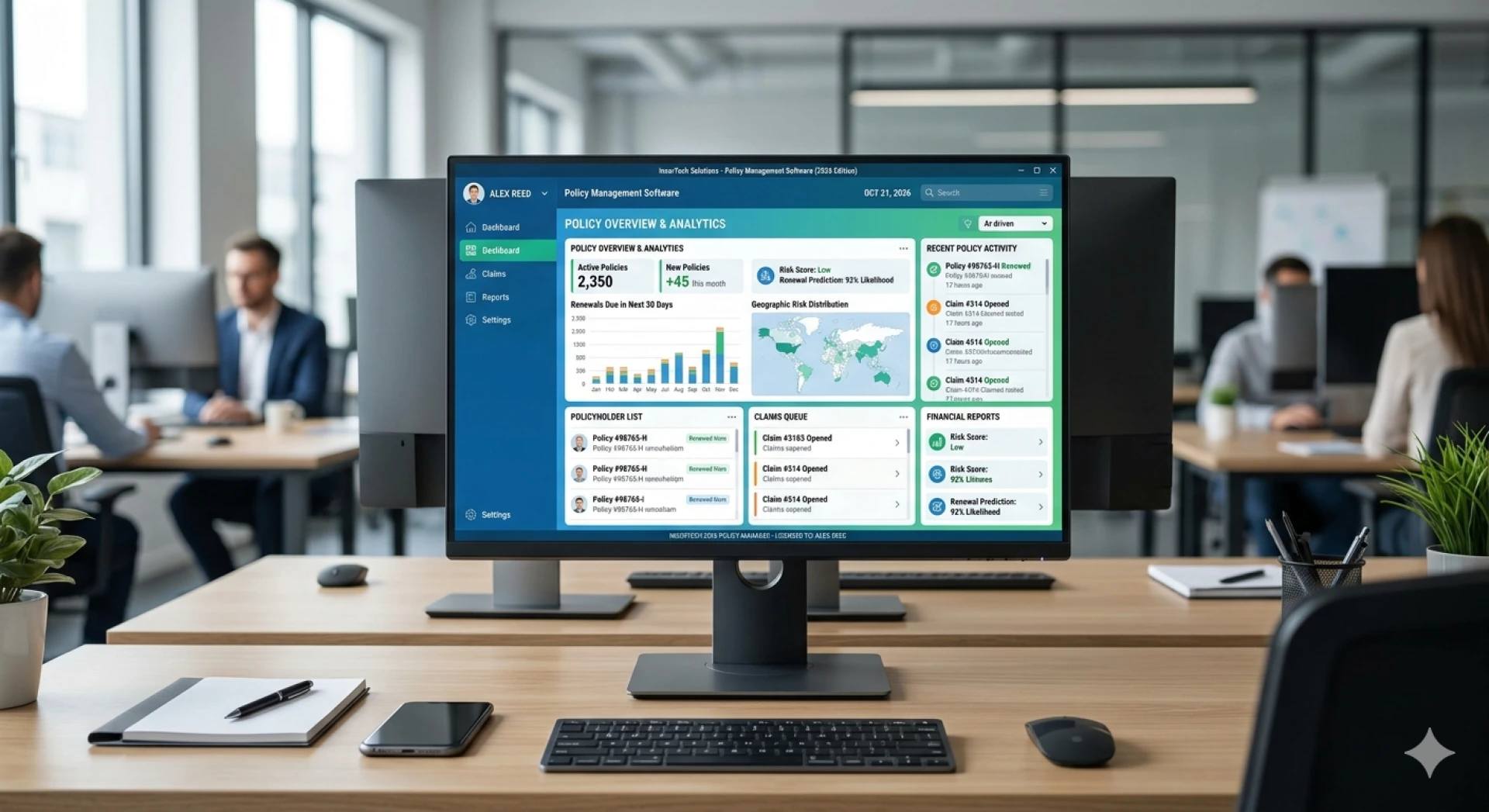

The Operational Backbone: Key Workflows Automated by Insurance Management Systems

An insurance software system coordinates six operational workflows that determine how efficiently carriers quote, bind, service, and settle policies.

1. Policy Administration and Lifecycle Management

The insurance policy management journey spans years, from underwriting through renewal and cancellation. Each stage involves diverse touchpoints and data upgrades that must travel seamlessly across systems. Insurance management systems automate the entire policy lifecycle management without manual handoffs.

Automated components include:

- Policy issuance with automatic document generation and delivery.

- Endorsement processing triggered by exposure changes or customer requests.

- Renewal quote generation based on current ratings and risk adjustments.

- Reinstatement handling for lapsed policies.

- Cancellation processing with proper notice and refund calculations.

- Policy status tracking accessible to customers and agents.

- Digital document storage and retrieval.

Consider a commercial lines policy that runs for years. Without implementing automation solutions, an underwriter manually reviews every policy change: a new location included, equipment upgrades, name changes on the business. These modifications require manual entry, verification, and documentation. A modern insurance management software system flags these changes through integration with customer data and automatically initiates appropriate processing workflows.

The financial impact compounds across your portfolio. More importantly, policyholders experience faster, more consistent handling. A location change processes automatically rather than sitting in someone's queue. Customers receive accurate renewal quotes promptly. Errors decline because machines apply rules consistently without human fatigue or oversight.

2. Claims Processing Pipeline

Claims represent the moment customers discover whether your company delivers on its promises. Fast, accurate claims handling builds loyalty. The slow claims processing leads to cancellations and negative reviews from policyholders. Automated insurance management systems speed up claim processes without compromising precision.

A modern claims pipeline operates in stages, with automation handling the routine work:

- First notice of loss intake via online portal, phone, or email.

- Automatic data extraction and policy verification.

- Coverage determination using policy language and business rules.

- Fraud detection through pattern analysis and external data sources.

- Medical bill review and network pricing for health and workers compensation.

- Settlement recommendation with itemized calculations.

- Payment processing and claimant notification.

A claims team processing hundreds of claims monthly might require four full-time adjusters under manual procedures. Automated triage and routine processing reduce the adjuster’s workload. Genuine claims route directly to payment. Complex cases escalate for human review and negotiation.

The customer experience transforms as well. Manual claims processing typically requires a week. Automated systems settle the genuine claims within 3 to 5 business days. Claimants receive money sooner. Litigation risk declines because customers see prompt, professional handling.

3. Underwriting and Risk Assessment

Underwriting drives profitability. Better risk selection means lower claims costs. Faster underwriting means winning business before competitors. Modern insurance software systems enable both simultaneously.

- Insurance company software accelerates underwriting through:

- Automated data gathering from industry databases and public sources.

- Risk assessment using configured business rules and historical loss data.

- Quote generation with appropriate pricing for identified risk characteristics.

- Exception flagging for cases requiring human judgment.

- Rate comparison against competitive benchmarks.

- Documentation assembly for audit and compliance purposes.

Faster underwriting creates a competitive advantage. A carrier answering quote requests within a few hours wins more deals than competitors requiring two business days. An insurtech startup that leverages automated underwriting capabilities can capture huge market share and remain ahead of the competitors.

4. Premium Billing and Collections

Revenue does not appear until customers pay. Billing and collections processes determine cash flow timing and collection rates. Automation improves both metrics substantially.

An insurance management system automates the entire billing cycle:

- Premium calculation incorporating all endorsements and adjustments.

- Bill generation with payment options and due dates.

- Electronic delivery via email, portal, or print mail.

- Automatic payment processing for customers with stored payment methods.

- Payment allocation across multiple policies.

- Renewal billing is triggered automatically based on policy dates.

- Collection workflows for overdue accounts.

- Dunning sequences and cancellation processing for non-payment.

More importantly, automation accelerates cash collection. Electronic delivery and online payment options reduce payment time for the average customer. Collections improve as well. Automated dunning sequences reach customers before policies lapse. Proactive outreach helps insurers retain substantial revenue and improve cash position.

5. Customer Communication

Smart insurance company software offers instant, event-based messaging support across various communication channels. Automated systems distribute instant claim confirmation messages, payment reminders, and policy updates to policyholders, eliminating manual outreach activities. The intelligent customer service agents in insurance software address policy upgrades and billing queries of customers without human intervention. Communication tools integrate with CRM and policy administration platforms to generate messages reflecting each policyholder's actual situation rather than generic templates.

6. Compliance & Regulatory Reporting

Software for insurance companies automates statutory reporting across various jurisdictions including NAIC, OSFI, EIOPA, and FCA requirements. The software systems link data across reports in secure cloud environments where policy updates sync across documents and minimize errors while speeding up submission timelines. Automated compliance engines in insurance software monitor transactions consistently, flag discrepancies, and generate audit-ready reports. This minimizes compliance penalties while freeing insurance operations teams from manual regulatory tracking.

Why Evaluating Your Vendor Matters More Than Evaluating the Software

Most insurance enterprises begin their selection process by comparing software features. They build spreadsheets listing functionality: does this system do claims automation, policy renewals, customer portals? They score each feature and declare a winner based on checklist completeness.

This approach overlooks a critical reality: software is static, but vendor relationships are dynamic. You will live with this vendor for a decade or longer. The software will change, be updated, require customization, encounter problems, and need support. Your vendor partnership determines whether those experiences frustrate your team or energize them.

How to Choose an Automated Insurance Software Vendor

Traditional request for proposal processes creates false confidence in insurance software vendor selection. What appears suitable on paper often underperforms in practice. Carriers who succeed don't just purchase software solutions. They build partnerships that accelerate long-term value.

I. Functional Fit and Product Maturity

Vendors must demonstrate transparency about what their platform can and cannot do. Insurance-specific expertise matters because providers familiar with policy administration and claims workflows adapt faster to operational requirements. Product maturity shows through proven implementations with similar carriers.

II. Vendor Stability and Financial Health

Financial stability ratings highlight an insurance software vendor's capacity to survive economic downturns and meet obligations. Review years in operation and client retention rates along with growth trajectory.

III. Strategic Alignment and Organizational Change

Insurance transformations fail when organizations underestimate the people side of change. Successful implementations require leadership arrangement and structured training programs. Make sure that insurance software vendors provide adequate change management and training support. Change management integrated into delivery makes the difference.

The Path Forward: Building a Resilient Insurance Business Using Automation

Automated insurance management software delivers measurable returns that manual operations cannot match. Carriers who compress settlement cycles and redirect underwriter time toward risk review gain competitive ground against peers still locked into legacy workflows. The technology exists, and proven implementations demonstrate ROI. Before selecting a vendor, carriers should review technical architecture and implementation support rather than just feature checklists. Organizations that treat automation as a partnership rather than a purchase position themselves for growth in a digital world that changes constantly.

Sign in to leave a comment.