Legacy policy administration systems in insurance environment function like outdated equipment on a modern production floor. The siloed data architectures and manual processes associated with legacy policy systems create operational hindrances that drain resources and hinder growth potential. Insurers who depend on legacy infrastructures experience slow policy issuance cycles, ineffective workflows, and rising maintenance expenses that consume budgets meant for process innovation.

The shift to modern insurance policy management software helps carriers resolve basic operational hindrances. The legacy solutions lack the architectural resilience required to leverage advanced technologies. Insurance firms that attempt to launch new products or respond to regulatory variations struggle with rigid code structures that necessitate extensive developer intervention. This obstacle translates to missed market opportunities and competitive disadvantages as more agile insurance competitors acquire market share.

Why Insurers Should Track Policy Management System Predictions

Market dynamics in insurance change faster than underwriting models can adapt. Insurance firms that function without knowledge of advanced insurance policy management system trends risk strategic mistakes that escalate over various quarters. Understanding the policy software trends and predictions enables insurance business leaders to allocate budgets wisely, prioritize technology investments, and eliminate major platform migrations.

Predictive insights are valuable for strategic intelligence for stakeholders who manage competitive pressures. Leadership departments that learn how artificial intelligence, embedded insurance models, and immediate pricing engines will transform policy management can position their firms ahead of disruption. This foresight enables proactive planning cycles that arrange technology roadmaps with market development.

The benefits of tracking insurance policy management software predictions extend across multiple operational dimensions:

- Precise Resource Allocation: Understanding the standard capabilities that transform policy management enables insurers to invest in scalable solutions rather than implementing incremental fixes to legacy systems.

- Market Positioning: Insurance firms that forecast customer expectations for hyper-personalized products can determine experiences that competitors struggle to replicate.

- Risk Mitigation: By understanding regulatory compliance trends, insurers can eliminate major infrastructure updates when new mandates are announced.

- Partnership Strategies: The change toward API-driven distribution informs decisions about ecosystem partnerships and platform integrations.

Platforms purchased without thinking about emerging standards to become liabilities when they cannot support next-generation capabilities. Insurers who invest in insurance policy management system software lacking AI readiness or cloud-native architectures face pricey rework cycles that drain innovation budgets.

What Are the Policy Management System Software 2026 Predictions?

The insurance sector stands at an inflection point where artificial intelligence transitions from experimental tooling to operational infrastructure. Several prediction patterns emerge as insurance policy management software vendors and carriers prepare for fundamental changes in how policies get created, priced, serviced, and distributed.

1. Agentic AI is the New Operating Model

Automated AI agents that execute diverse tasks rather than just performing data analysis will become the operating model of policy management systems.

- The AI agents in policy management software manage claims adjudication, direct complex cases to human adjusters, and resolve claims under zero human intervention.

- Trained fraud detection agents evaluate patterns in transaction data and trigger investigation workflows when anomalies are present.

- Smart underwriting agents recommend pricing and coverage options, extracting data from disparate sources to develop complete risk profiles.

AI moves from advisory dashboards to action layers that make decisions throughout the value chain.

2. Hyper Personalization Through Data and Analytics

Insurance firms can tailor coverage options depending on individual behaviors acquired through telematics, wearables, and connecting devices. Analytics modules for usage-based motor insurance validate premiums depending on actual driving patterns rather than demographic conditions. Health insurers deliver discounts for lifestyle choices monitored through fitness devices. Smart AI algorithms assess customer data and generate tailored risk profiles. Coverage reflects specific needs rather than broad segment assumptions. Static policy structures change into dynamic products that evolve with policyholder circumstances.

3. Zero-Touch Policy Processing and Automation

Advanced policy management systems with automation workflows eliminate manual intervention and ensure smooth policy lifecycle management. The automation workflows streamline policy issuance, endorsements, renewals, and simple claims settlements without human intervention. Insurance policy management system software discovers deviations and resolves issues through troubleshooting mechanisms. Complex policy cases are routed to experts with better context, while automation manages volume. This approach balances policy processing scale with administration and eliminates errors.

4. Embedded Insurance and API-Driven Distribution

Insurance policy issuance software integrates directly into partner platforms through standardized APIs.

- Coverage purchases happen at transaction points.

- Retailers incorporate product warranties at checkout, travel platforms deliver trip insurance during bookings, and automotive platforms bundle insurance coverage with vehicle purchases.

- The API architectures enable insurers to distribute products through diverse channels without custom integrations for different partners.

The connected platform architecture minimizes implementation timelines from months to weeks.

5. Regulatory Compliance and Explainable AI

The insurance regulators necessitate transparency in algorithmic decisioning and compel insurers to demonstrate the way AI systems function and maintain fairness. Documentation must monitor data inputs, decision logic, and model variations with extensive audit trails. Explainable AI becomes an essential infrastructure rather than optional functionalities. Governance frameworks necessitate bias testing and human administration for high-stakes decisions impacting coverage and pricing options.

6. Instant Pricing and Underwriting

The incorporation of pricing engines in policy management software replaces static valuation. Pricing engines assess claims trends, telematics data, and macroeconomic indicators with greater precision. The algorithms simulate thousands of pricing scenarios to optimize profitability and competitiveness at once. Underwriting decisions that took days are now accomplished in minutes as AI extracts data from IoT devices, public records, and credit portals. Insurance policy management systems adjust to market conditions faster than competitors, depending on quarterly updates because of this responsiveness.

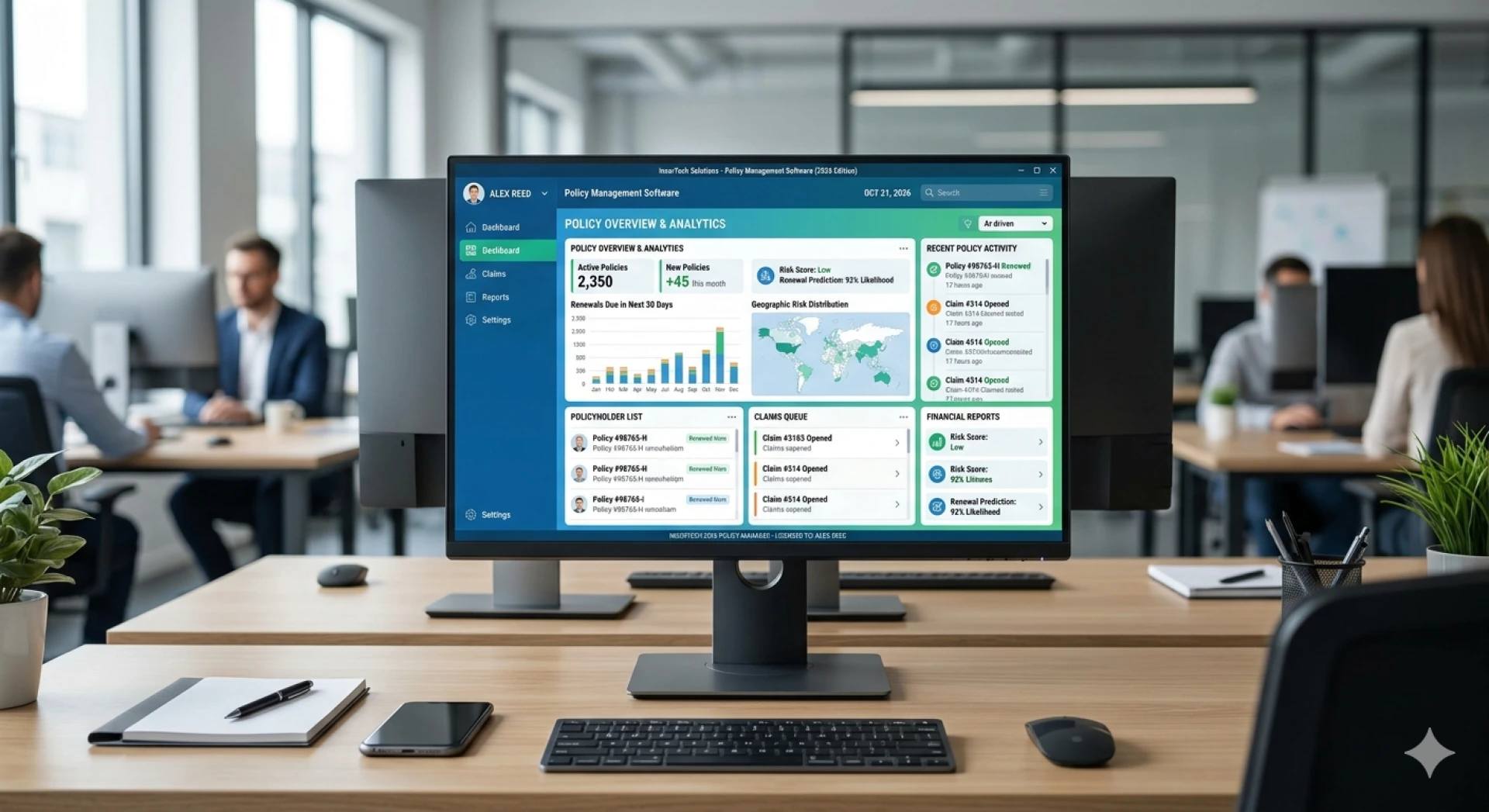

Feature Validation for Insurance Policy Management Software Selection

Selecting insurance policy management software without rigorous feature validation resembles purchasing infrastructure based on vendor promises rather than operational requirements. Insurers face costly implementation failures when platforms lack core capabilities needed for modern operations. Feature assessment separates marketing claims from actual functionality that drives business outcomes.

I. Intelligent Policy Lifecycle Management

End-to-end lifecycle capabilities manage policies from quote generation through cancelation.

- Systems automate policy issuance, premium calculations, renewals, endorsements, and documentation while minimizing manual intervention.

- Rule-based engines accelerate underwriting by automating risk assessment and premium determination.

- Workflow automation will give accurate policy processing and reduce errors that compromise customer satisfaction.

Version control tracks policy changes across the whole lifecycle and maintains complete historical records.

II. Integration with External Platforms

API capabilities enable different systems to communicate without custom development overhead. Cloud-based architectures provide scalability and immediate data access while reducing infrastructure costs. Integration with third-party data sources supports accurate underwriting through credit reports, telematics, and health data connections. Legacy system compatibility will give smooth transitions without operational disruption. Connections to CRM platforms, accounting systems, billing tools, and analytics platforms eliminate data silos and manual entry.

III. Customer Experience Management

Self-service portals allow policyholders to view coverage details, make payments, file claims, and update information independently. Omnichannel delivery will give consistent experiences across web, mobile, and agent interactions. Digital tools reduce friction in routine transactions while preserving human touchpoints for complex decisions.

IV. Regulatory Compliance and Audit Management

Built-in compliance frameworks in insurance policy issuance software autonomously update with regulatory changes in jurisdictions of all types. Audit trails track all transactions, policy modifications, and system access for accountability. Automated reporting generates required regulatory filings without manual compilation. Role-based access controls and multi-factor authentication protect sensitive data while meeting security standards.

Final Words

Modern insurance operations just need platforms built for AI-driven automation and live processing. Insurers must then confirm core functionalities before committing to policy management systems. Those who select platforms with agentic AI capabilities and detailed compliance frameworks position themselves ahead of competitors dependent on legacy systems. The right software choice changes operational bottlenecks into strategic advantages. Firms can meet evolving customer expectations while maintaining competitive pricing and risk precision.

Sign in to leave a comment.