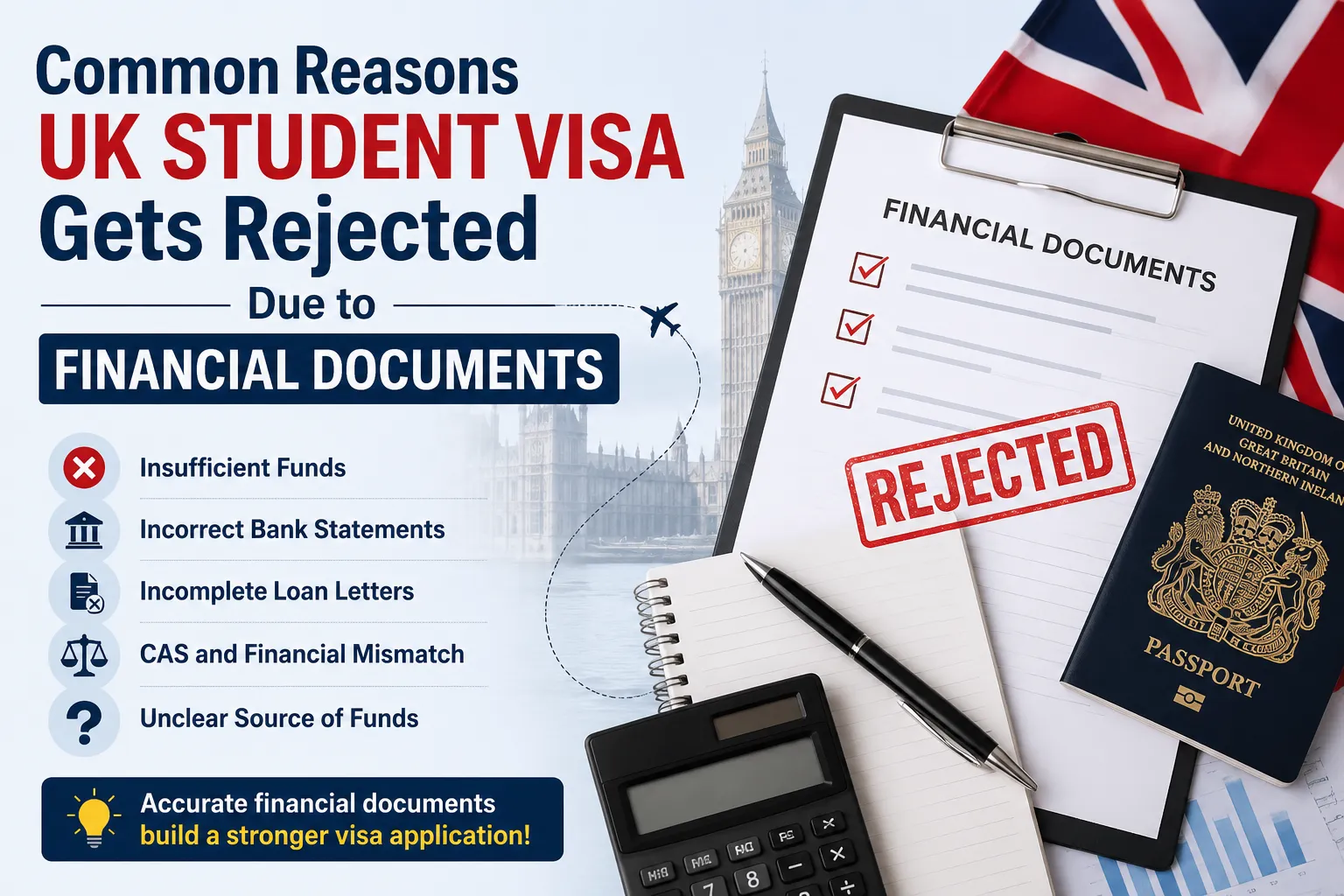

A UK Student visa application depends heavily on accurate financial documentation. Even when a student has admission from a UK university, a valid CAS, and genuine study plans, mistakes in financial documents can lead to visa refusal. This is especially important for students arranging an overseas study loan for Masters in UK, because the loan documents must clearly meet visa requirements.

Financial proof is not just a formality. UK Visas and Immigration checks whether the applicant has enough money to pay tuition fees and living costs during their stay in the UK. If the financial evidence is incomplete, unclear, outdated, or does not match the official requirements, the visa application may be rejected.

Why Financial Documents Matter in a UK Student Visa Application

When applying for a UK Student visa, students may need to show that they have enough funds for:

- Unpaid course fees mentioned on the CAS

- Living expenses in the UK

- Additional funds for dependants, if applicable

The money can usually be shown through personal savings, parent or guardian funds, official sponsorship, or an approved education loan. However, the format, timing, and details of these documents are very important. A small error in the bank statement or loan letter can create doubts about fund availability.

1. Not Maintaining Funds for the Required Period

One of the most common reasons for rejection is not maintaining the required funds for the correct period. If a student is using bank savings, the funds usually need to be held for a continuous 28-day period.

The balance should not fall below the required amount at any point during this period. Even if the account balance is high on the final day, the application can face problems if the amount dropped below the required level during the 28 days.

2. Submitting an Old Bank Statement

Financial documents must be recent. Students often make the mistake of using an outdated bank statement or a statement that does not fall within the accepted timeline.

A bank statement should be close to the visa application date and should clearly show the account holder’s name, account number, financial institution details, transaction history, and closing balance. If the statement is too old or incomplete, UKVI may not accept it.

3. Showing Less Money Than Required

Another major reason for refusal is showing insufficient funds. Students must calculate the required amount carefully. This includes unpaid tuition fees plus living costs.

If part of the tuition fee has already been paid, it should be reflected correctly on the CAS. If the CAS does not show the payment, the student may still need to prove the full unpaid fee amount separately.

4. Mismatch Between CAS and Financial Documents

Your CAS contains important financial details, including course fees and any amount already paid to the university. If the financial documents do not match the CAS, it can create confusion.

For example, if you paid a tuition deposit but the CAS does not mention it, UKVI may calculate your financial requirement based on the full tuition fee. Students should check their CAS carefully before applying and request corrections from the university if needed.

5. Using an Unacceptable Source of Funds

Not every source of money is accepted as financial evidence. Funds from unsupported third parties, business accounts, cryptocurrency, property valuation, or informal borrowing may not be accepted.

If funds are held in a parent or legal guardian’s account, the student may need to provide relationship proof and a consent letter. If these supporting documents are missing, the visa application may be at risk.

6. Education Loan Letter Does Not Meet Requirements

Students using Study in UK Education Loans must be extra careful with the loan sanction letter. A loan approval letter should clearly confirm that the loan is for education, mention the approved amount, identify the student, and state that the funds are available for studying in the UK.

A weak or incomplete loan letter can lead to rejection. Common issues include:

- The letter does not mention the student’s full name

- The loan is not clearly described as an education loan

- The approved amount is missing or unclear

- The lender details are incomplete

- The letter includes conditions that make fund release uncertain

- The letter is not dated properly

- The loan is in someone else’s name instead of the student’s name

7. Using a Personal Loan Instead of an Education Loan

A personal loan is not the same as an education loan. Even if a student plans to use a personal loan for studies, it may not be accepted as a student loan document for visa purposes.

If the money from a personal loan has already been transferred into an accepted bank account and maintained according to the required rules, it may be considered as personal funds. However, a personal loan approval letter itself may not work as education loan evidence.

8. Missing Bank Details or Incorrect Statement Format

UKVI expects financial documents to be clear and verifiable. A bank statement may create problems if it does not include essential details such as:

- Account holder’s name

- Account number

- Bank name or logo

- Transaction dates

- Balance information

- Currency

- Official stamp or digital verification, if required

Screenshots, edited PDFs, or informal account summaries can be risky. Students should always use official bank documents.

9. Sudden Large Deposits Without Explanation

A sudden large deposit in the bank account may raise questions if it is not clearly explained. UKVI may want to see that the money genuinely belongs to the student or their parent/legal guardian and is available for education.

If there are large deposits close to the visa application date, students should keep proper supporting documents, such as sale receipts, fixed deposit closure proof, salary records, or transfer explanations.

10. Currency Conversion Mistakes

Students applying from outside the UK often submit documents in local currency. If the amount is close to the minimum requirement, currency fluctuations can create a problem.

It is safer to maintain a buffer amount above the required minimum. This reduces the risk of falling short due to exchange rate changes at the time of assessment.

11. Fixed Deposits or Savings Products Without Proper Proof

Fixed deposits may be accepted in some cases if they are easily accessible and the document clearly shows the amount, account holder, maturity details, and availability of funds. However, if the money is locked, inaccessible, or cannot be withdrawn when needed, it may not support the application properly.

Students should confirm whether their type of savings document is acceptable before relying on it.

12. Missing Parent or Guardian Consent Documents

If funds are held in a parent or legal guardian’s account, the student must usually prove the relationship and provide written consent to use the money.

Common mistakes include submitting only the parent’s bank statement without:

- Birth certificate or legal relationship proof

- Parent or guardian consent letter

- Parent or guardian identity document, where needed

Without these documents, the funds may not be linked properly to the student.

13. Relying on Verbal Assurances from the Bank or University

Students sometimes rely on verbal confirmation from banks, agents, or university representatives. However, UKVI decisions are based on written evidence.

Every claim about money, tuition payment, scholarship, sponsorship, or loan approval should be supported by proper documentation.

14. Submitting Documents With Name or Date Errors

Simple spelling or date errors can create serious issues. The name on the passport, CAS, bank statement, and loan letter should be consistent. If there is a difference, students should provide clarification or corrected documents before submitting the application.

Date errors are also risky. A loan letter or bank statement outside the accepted timeline may not be valid.

15. Not Checking the Latest Visa Guidance

Financial rules can change. Students should not rely only on old blogs, social media posts, or advice from previous applicants. Before applying, they should check the latest official UK visa guidance and confirm the requirements with their university’s international student support team.

How to Avoid Rejection Due to Financial Documents

To reduce the risk of refusal, students should:

- Start preparing financial documents early

- Check the exact financial requirement from the CAS

- Maintain a safe buffer above the minimum amount

- Use official bank statements or valid loan letters

- Avoid unexplained last-minute deposits

- Make sure loan letters clearly mention education purpose and fund availability

- Check that names, dates, and amounts match across documents

- Keep parent consent and relationship proof ready if using parent funds

- Review the latest UKVI financial guidance before applying

Final Thoughts

Financial document errors are one of the most avoidable reasons for UK Student visa rejection. Most refusals happen not because students do not have funds, but because they fail to prove those funds in the correct format.

Whether you are using savings, family funds, sponsorship, or an education loan, the documents must be complete, recent, consistent, and acceptable under UK visa rules. Careful preparation can make your visa application stronger and reduce the risk of unnecessary delays or refusal.

FAQs

1. Can a UK Student visa be rejected due to bank statement mistakes?

Yes. If the bank statement does not meet the required format, does not show enough funds, or does not cover the required period, the visa can be refused.

2. Is an education loan accepted for a UK Student visa?

Yes, an education loan may be accepted if it meets UKVI requirements and the loan letter clearly confirms the approved amount, education purpose, lender details, and fund availability.

3. Can I use my parent’s bank account for UK visa financial proof?

Yes, but you may need to provide proof of relationship and written consent from your parent or legal guardian.

4. What if my CAS does not show the tuition fee I already paid?

You should contact your university and request a corrected CAS before applying. If the CAS does not reflect the payment, UKVI may treat the amount as unpaid.

5. Should I keep extra money above the required amount?

Yes. Keeping a buffer is recommended because exchange rates and calculation errors can affect whether your funds meet the requirement.

Sign in to leave a comment.