If you've ever been in a car accident, even a minor one, you've probably dealt with repairs, insurance adjusters, and maybe even a rental car or two. But there's one part of the post-accident puzzle most people overlook: the diminished value claim. It sounds like something straight out of a legal textbook, yet it could mean thousands of dollars in your pocket. So, why is it so uncommon?

First, What Is a Diminished Value Claim?

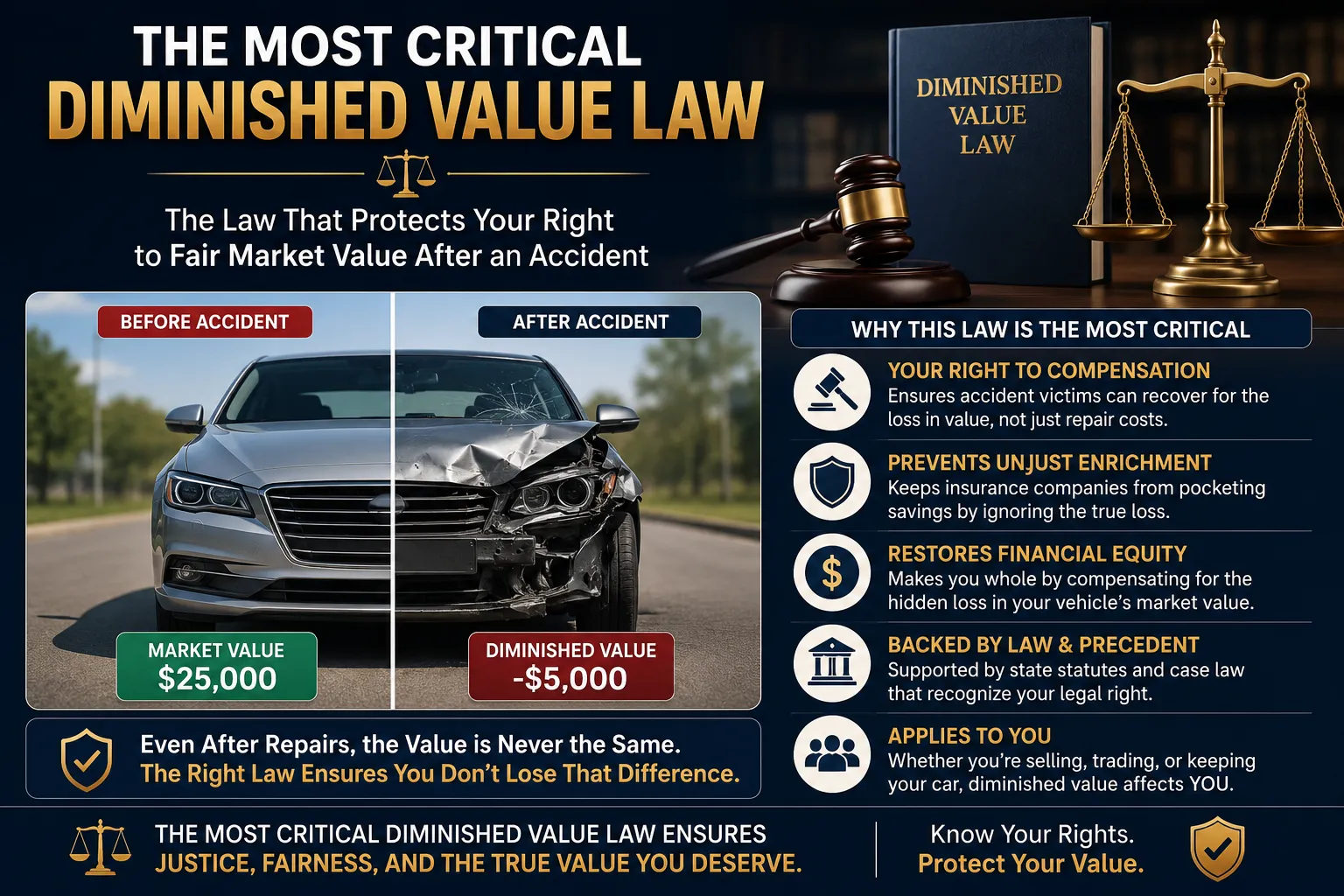

A diminished value claim allows you to recover the difference in your car’s value before and after an accident — even after it’s been fully repaired. Think about it: if you were buying a used car and discovered it had been in a crash, would you still pay top dollar for it? Probably not. That’s the loss in value — and that’s what a diminished value claim seeks to recover.

Not All Insurance Policies Are Created Equal

One reason diminished value claims are rare is because not all insurance companies make it easy. In fact, your own insurer often won’t cover diminished value if you're at fault in the accident. You typically have to go after the at-fault driver's insurance company. That alone makes the process more complex and discourages people from even trying.

Lack of Awareness

Ask the average driver about diminished value, and you'll probably get a blank stare. This type of claim isn’t advertised or explained well by insurers. Many people don’t even know they have the right to file for diminished value in some cases — especially if they weren't at fault in the accident. That lack of awareness plays a huge role in why these claims are so underutilized.

It’s Not Automatic — You Have to Ask

Unlike medical payments or car repairs, diminished value isn't something an insurance adjuster brings up. You have to specifically request it — and often, you need to provide evidence like appraisals, market comparisons, or expert opinions. This extra effort deters people who may already be overwhelmed with the accident itself.

It Requires Proof and Patience

A diminished value claim isn’t just about saying, “My car is worth less now.” You’ll likely need to get an independent appraisal to prove the loss in value. That could cost a few hundred dollars, and there’s no guarantee the insurer will agree with the appraisal. Many people weigh the effort versus the possible payout and simply opt not to pursue it.

State Laws Vary… A Lot

Not every state recognizes diminished value claims, and the laws that do exist vary wildly. Some states limit who can file them. Others don’t allow you to file at all unless certain conditions are met. So even if you’re entitled to file, the process can be confusing depending on where you live.

Insurance Companies Aren’t in a Hurry to Pay

Let’s be honest — insurance companies aren’t jumping to write checks they aren’t legally required to. Since diminished value claims aren’t as cut-and-dried as repair costs, insurers often push back hard. They may lowball the offer or deny the claim altogether. That’s a frustrating experience for policyholders who don’t know how to fight back.

It Can Turn into a Legal Battle

If the insurer refuses to cooperate, your only recourse might be small claims court or hiring an attorney. That adds time, expense, and stress to an already frustrating situation. For a lot of people, it’s just not worth the hassle unless the lost value is significant — typically several thousand dollars.

Most People Just Want to Move On

After an accident, most folks are focused on getting their car back, healing from injuries, or just returning to normal life. A diminished value claim often feels like one more headache, and people figure, “I’ll just live with it.” The potential reward doesn’t always feel worth the emotional investment.

It’s Easier With New or High-End Cars

Diminished value claims tend to make more sense with newer or luxury vehicles, where the loss in resale value can be substantial. If you’re driving a 12-year-old sedan, the diminished value might be a few hundred bucks — not really worth the battle. That skews the statistics and makes these claims seem even rarer than they are.

Final Thoughts

Diminished value claims are one of the best-kept secrets in the auto insurance world — and that’s by design. Between lack of awareness, legal complexity, and insurer resistance, it’s no wonder most people don’t pursue them. But if you’ve been in an accident and your car wasn’t your fault, it’s worth at least exploring the option. You could be leaving real money on the table.

Source: https://sites.google.com/view/diminished-value-claim---/home

Sign in to leave a comment.