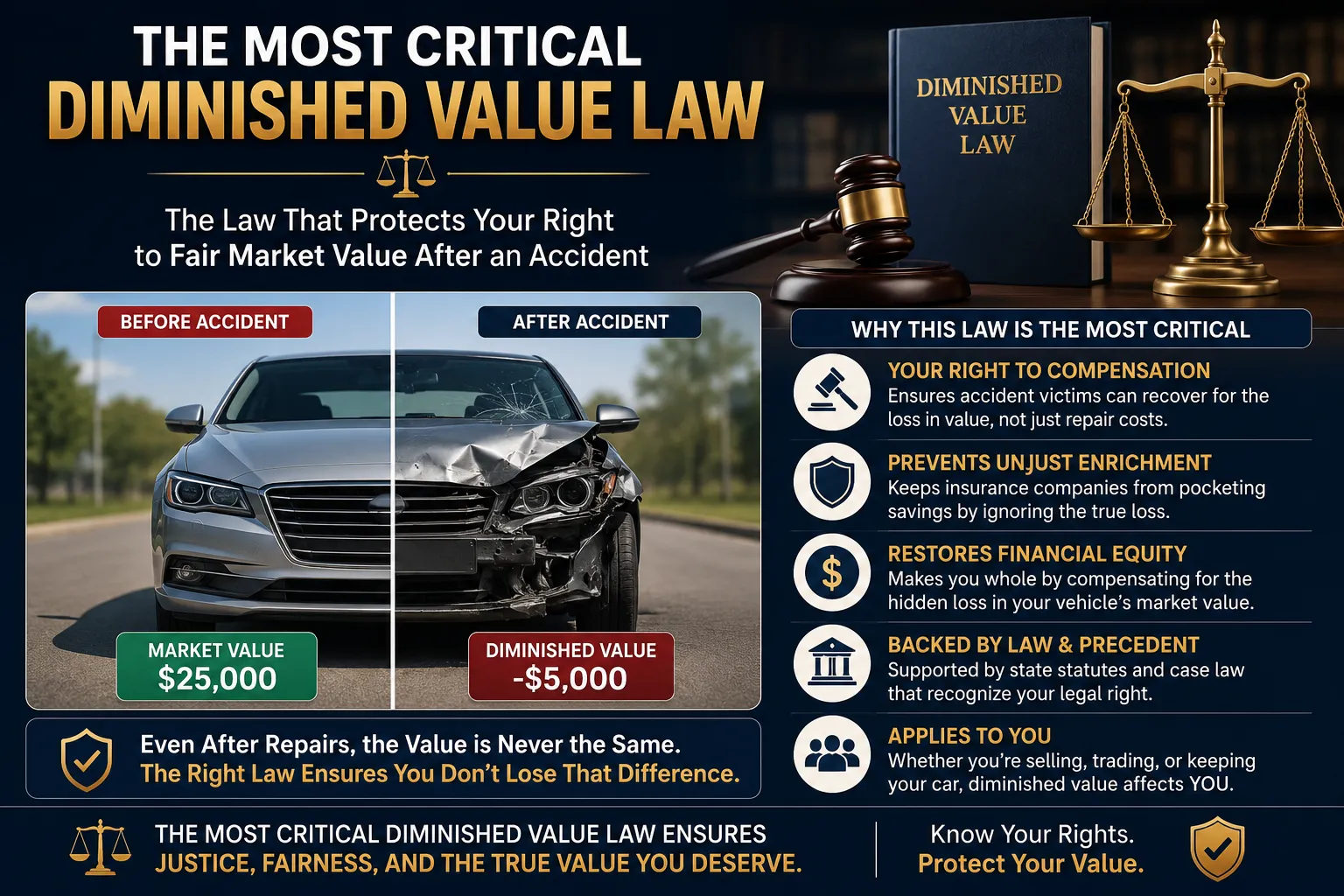

When your car has been in an accident, even after repairs, its value usually takes a hit. This loss in value—despite being fully fixed—is known as diminished value. Insurance companies may not openly tell you, but you could be entitled to compensation for this drop in resale value. Here's how to prove and maximize a diminished value claim like a pro.

1. Understand What Diminished Value Means

Diminished value refers to the reduction in a vehicle’s market value after it's been involved in an accident and repaired. Even if your car looks brand-new, a history report (like Carfax) will reveal the damage—and that scares off buyers. It’s not just a theory; it’s a real, quantifiable loss.

2. Know the Three Types of Diminished Value

There are three types: immediate, inherent, and repair-related. Immediate diminished value is the difference in value before and right after the accident. Inherent value is the permanent loss due to accident history, even after perfect repairs. Repair-related value reflects poor workmanship or use of non-OEM parts. Most claims involve inherent diminished value.

3. Confirm If You're Eligible to File

Not everyone qualifies. Generally, you can only file if you're not at fault and the at-fault party’s insurance accepts liability. If you're in a no-fault state or used your own insurance (and don’t have uninsured motorist property damage coverage), your options might be limited.

4. Act Quickly Before Deadlines Pass

Diminished value claim Florida often have a statute of limitations, which varies by state (typically 2–4 years). Waiting too long can cost you the right to file, so don’t drag your feet once the car is repaired and the at-fault party is identified.

5. Gather Documentation to Prove Value Loss

Start with the basics: pre-accident appraisals, repair invoices, photos, and the accident report. Use car valuation tools like Kelley Blue Book or Edmunds to show your car’s value before and after the accident. This builds the foundation of your claim.

6. Get a Professional Diminished Value Appraisal

A licensed auto appraiser can provide a formal diminished value report, showing the drop in value with market comparisons and expert analysis. These reports carry weight, especially when insurance companies try to downplay your loss.

7. Be Prepared to Counter the Insurance Company’s Offer

Insurers often use formulas like the 17c formula (named after a Georgia court case) to calculate diminished value. However, this method usually lowballs your actual loss. You have the right to challenge their number with your own appraisal.

8. Consider Getting Multiple Appraisals

For high-end or newer vehicles, it's smart to get more than one appraisal to strengthen your case. When you present consistent reports from different experts, it becomes harder for the insurer to dispute your claim.

9. Write a Clear, Firm Demand Letter

Submit a detailed demand letter to the insurance company, attaching your appraisal and stating the exact amount you’re claiming. Be polite but assertive. Mention that you’re willing to escalate the issue if needed. Sometimes, that alone moves things forward.

10. Don’t Be Afraid to Negotiate

Insurance adjusters are trained negotiators, so don’t accept the first offer. Back up your counter with facts and expert assessments. Stay calm, professional, and persistent—it could mean hundreds or even thousands more in your pocket.

11. Use State Laws to Your Advantage

Some states are more favorable to diminished value claims. For example, Georgia strongly supports them, while others are murkier. Knowing your state’s stance can help you shape your strategy or even give you an upper hand in discussions.

12. Hire an Attorney if Needed

If your claim is large or you’re hitting roadblocks, hiring a personal injury or diminished value attorney might be worth it. Many work on contingency, meaning they only get paid if you win. A lawyer’s involvement often prompts faster, fairer resolutions.

13. Learn from the Experience for the Future

Once your claim is settled, take note of what worked and what didn’t. Understanding how diminished value claims operate will help you respond faster and smarter if you ever find yourself in a similar situation down the road.

14. Don’t Leave Money on the Table

Too many people leave thousands of dollars unclaimed simply because they didn’t know about diminished value—or gave up too soon. Now that you know the steps, you have the power to protect your financial interests and make sure you’re fully compensated for your loss.

Sign in to leave a comment.