In today's fast-changing financial world, lenders can no longer rely solely on traditional credit scoring models. The old systems, built around static parameters like credit history, income statements, and outstanding debts, often fail to capture a borrower's complete financial picture, especially in an era where alternative data and digital footprints are shaping financial behavior.

Enter dynamic credit scoring models—a more advanced, real-time, and data-rich approach to evaluating borrower risk. These models are not just upgrades—they're redefining how lending decisions are made, especially when powered by robust technology.

What Are Dynamic Credit Scoring Models?

Dynamic credit scoring refers to scoring systems that use real-time and non-traditional data points to evaluate a borrower's creditworthiness. Unlike traditional models that rely heavily on credit bureau data, dynamic models pull from a wide range of sources, such as:

- Banking and cash flow data

- Mobile phone usage

- Utility and rent payment records

- Social media behavior

- E-commerce activity

- Employment and education records

These data points are constantly updated, offering lenders a living profile of the borrower’s financial behavior rather than a snapshot frozen in time.

Why Traditional Credit Scoring Falls Short

Traditional scoring models, such as FICO or VantageScore, were not designed for the gig economy or unbanked populations. They can penalize borrowers with limited credit history (thin files) or those who prefer cash-based transactions. This leads to:

- High rejection rates for creditworthy applicants

- Limited access to loans for small businesses and freelancers

- Inaccurate risk assessment for emerging market borrowers

How Dynamic Credit Scoring Changes the Game

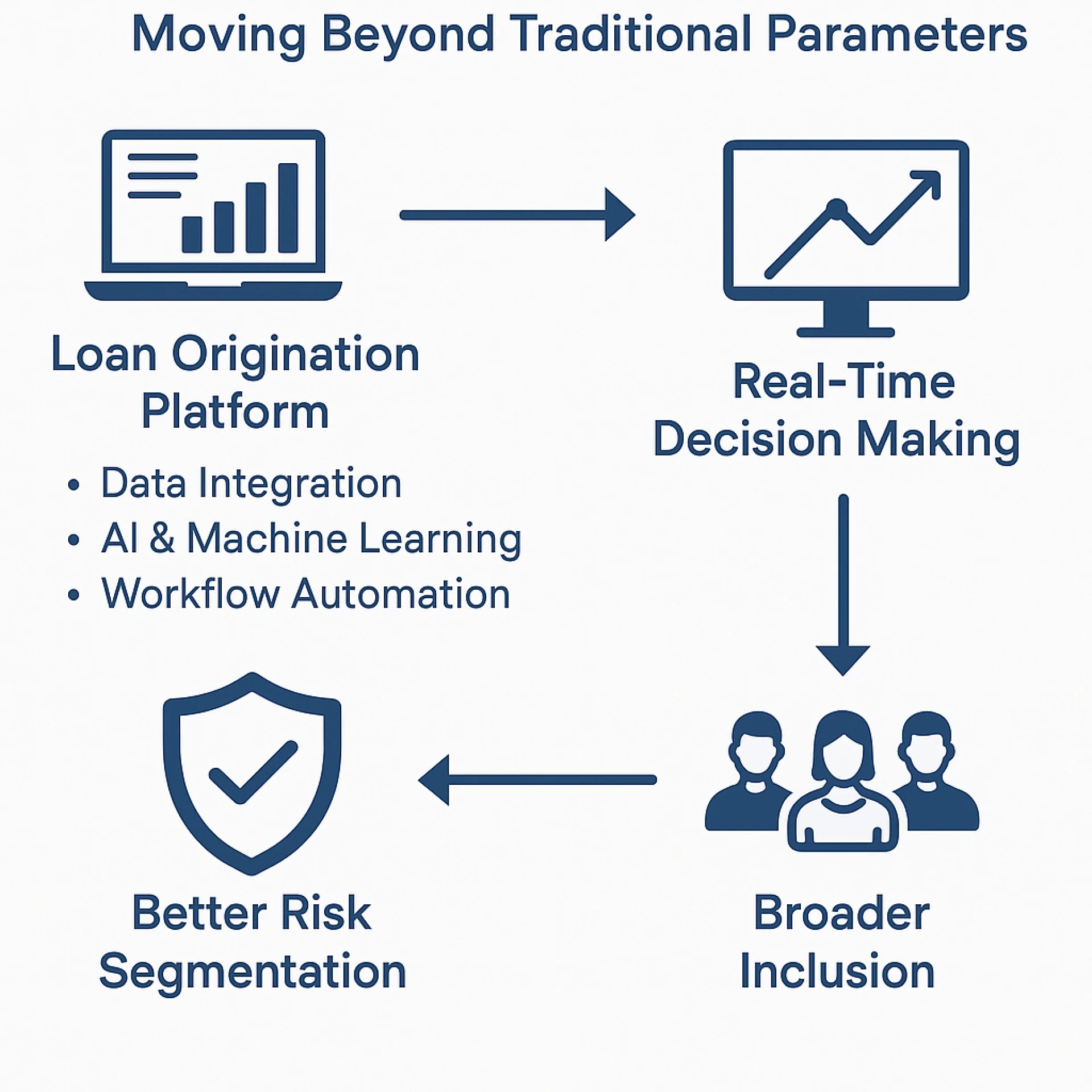

1. Real-Time Decision Making

Dynamic models provide continuous updates, helping lenders make informed decisions quickly. When integrated with a loan origination system, they can trigger instant approvals or rejections based on live data.

2. Broader Inclusion

People with no formal credit history—like students, self-employed workers, or rural borrowers—can still be evaluated using alternative data points.

3. Better Risk Segmentation

By analyzing behavioral and transactional data, lenders can group borrowers more accurately and design custom products based on their risk levels.

The Role of Technology: Loan Origination Software in Dynamic Credit Scoring

Advanced loan origination software plays a critical role in enabling dynamic credit scoring. Here’s how:

- Data Integration: Modern loan origination platforms are designed to pull data from APIs, mobile apps, banking systems, and credit bureaus—all in one interface.

- AI & Machine Learning: These platforms use predictive algorithms that evolve with data, helping lenders forecast borrower behavior.

- Workflow Automation: From application to disbursal, the loan origination system automates scoring, verification, risk analysis, and compliance.

Without an agile, data-driven loan origination platform, implementing dynamic credit scoring would be inefficient, costly, and slow.

Challenges and Considerations

While dynamic scoring offers many advantages, it also raises challenges:

- Data privacy: Collecting non-traditional data must comply with GDPR, CCPA, and other regulations.

- Bias and fairness: AI models must be audited to avoid reinforcing social or economic bias.

- Model explainability: Lenders must ensure that decisions based on dynamic models can be explained to regulators and borrowers.

This is where integrating an ethical AI layer and compliance engine into the loan origination platform becomes essential.

Future Outlook

As financial services become more digital and personalized, dynamic credit scoring will become the standard. The real innovation lies not just in data collection, but in how loan origination systems interpret and act on this data in real time.

We’re heading into a future where creditworthiness is not defined by your past mistakes, but by your current financial behavior—thanks to the power of AI, alternative data, and modern loan origination software.

Conclusion

Dynamic credit scoring models are revolutionizing the way lenders evaluate risk, expanding credit access to millions of underserved individuals and businesses. But to fully unlock their potential, lenders need agile, AI-ready loan origination platforms that can process vast datasets, learn continuously, and adapt to market needs. Moving beyond traditional parameters isn’t just a technical upgrade—it’s a strategic imperative in the modern lending ecosystem.

Sign in to leave a comment.