In the fast-changing world of finance, lenders are under constant pressure to innovate quickly, meet customer expectations, and comply with regulations—all while keeping costs down. That’s where no-code/low-code platforms come in. These platforms let lenders build, customize, and scale software without writing complex code. They’re changing the way banks, credit unions, and fintech companies approach lending software. Let’s explore how no-code and low-code platforms are reshaping loan technology.

What Are No-Code and Low-Code Platforms?

No-code platforms allow users to build applications using a drag-and-drop interface without writing any code. Low-code platforms, on the other hand, still offer visual development but allow for custom code where needed. Both help speed up development and reduce reliance on IT teams.

Why No-Code/Low-Code Is Gaining Popularity in Lending

- Speed to Market: Traditional lending systems can take months—or even years—to develop. No-code/low-code tools help lenders roll out new features or launch new lending products in weeks.

- Flexibility and Customization: Every lender has unique workflows, rules, and compliance needs. With a no-code or low-code platform, these can be tailored easily without waiting for a software developer.

- Lower Costs: Reducing the need for large development teams means cutting down costs. This makes it easier for smaller lenders and credit unions to stay competitive.

- Regulatory Compliance: Lending is a heavily regulated industry. No-code/low-code platforms allow compliance changes to be implemented quickly—reducing the risk of non-compliance.

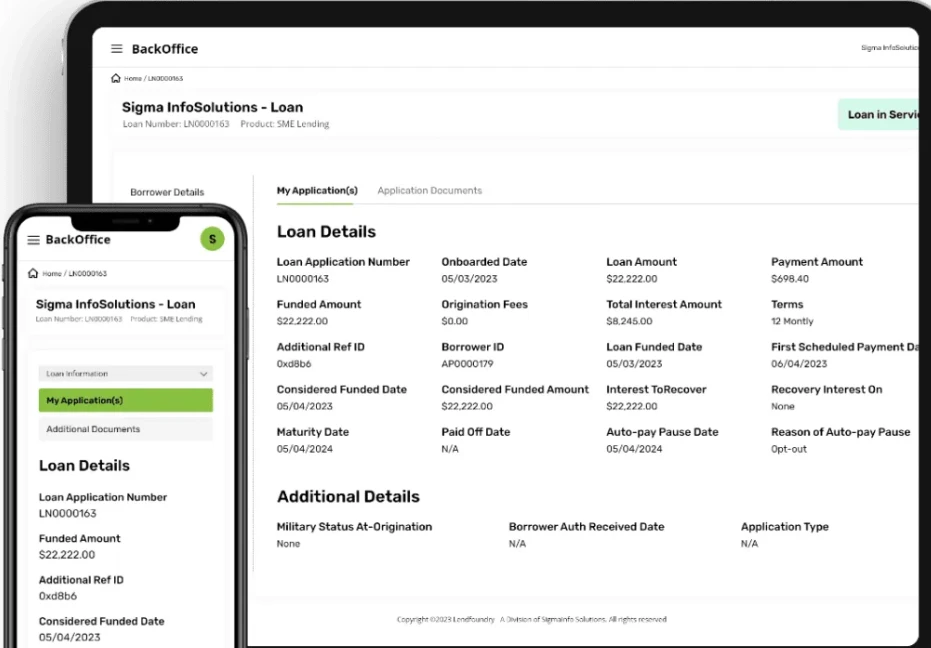

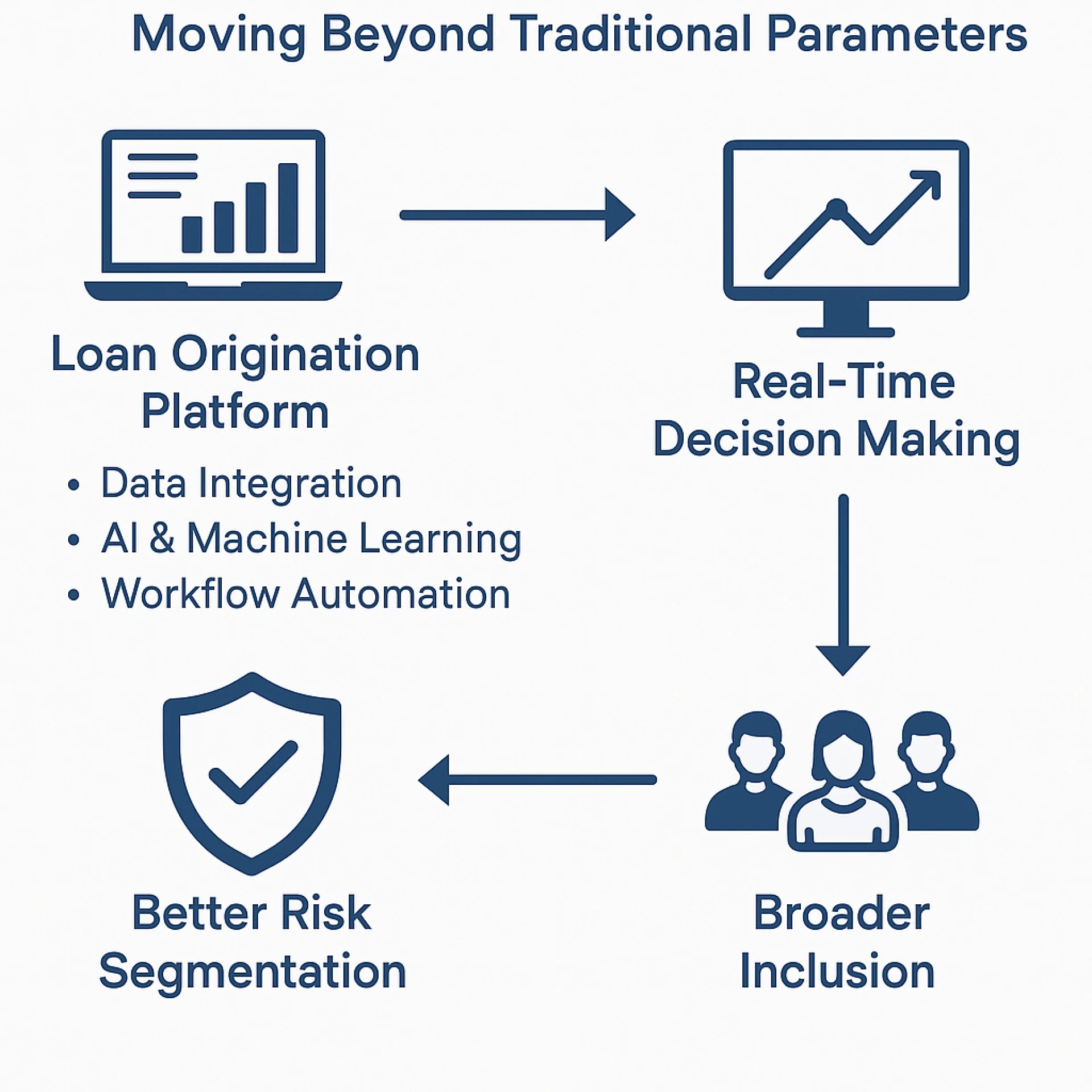

Role in Loan Origination Software

Loan origination software is used to manage the entire process of loan creation—from application to approval. With no-code/low-code tools, lenders can:

- Design custom digital loan applications

- Automate credit decisioning workflows

- Set up approval rules that match business policies

- Integrate with third-party services like credit bureaus, KYC/AML tools, and e-signature platforms

For example, a lender could use a no-code platform to create an online application form that adapts based on the loan type and applicant profile, without writing a single line of code. This creates a faster and more personalized experience for the borrower.

Role in Loan Servicing Software

Once a loan is issued, loan servicing software takes over. It handles billing, payment processing, customer communication, and collections. No-code/low-code platforms improve servicing in the following ways:

- Automating payment reminders and due-date alerts

- Creating dashboards for borrower account management

- Setting up rule-based workflows for late payments or refinancing

- Enabling self-service portals for borrowers to view balances, make payments, or request changes

Because servicing rules can vary across loan products, a no-code platform helps lenders adjust quickly as regulations or customer needs change—without complex system overhauls.

Integration with Existing Lending Ecosystems

Most lenders already use a variety of tools—CRM, analytics, compliance tools, etc. No-code/low-code platforms are often built with easy integrations in mind. They can connect with existing systems through APIs and webhooks, helping streamline the entire lending journey.

For example, a no-code platform might connect loan origination software with credit scoring tools and underwriting models, while also linking loan servicing software with payment gateways and customer support systems.

Empowering Non-Technical Teams

One of the biggest advantages of no-code/low-code tools is that they put power in the hands of non-technical users. Loan officers, compliance teams, or operations managers can make updates themselves—like changing form fields, updating approval logic, or generating reports—without waiting for IT.

This leads to faster decision-making, less IT bottlenecks, and more agile operations overall.

Challenges to Consider

While the benefits are many, there are also some challenges:

- Governance: Too much freedom can lead to inconsistent processes if not properly managed.

- Scalability: Some no-code platforms may struggle with large-scale or highly complex workflows.

- Security: Data security is crucial in lending. Not all no-code platforms are built with the same level of protection.

Choosing the right platform—and using it strategically—is key.

The Future of Lending Software Is Modular and Agile

As lending continues to move online and competition heats up, lenders need tools that are fast, flexible, and cost-effective. No-code and low-code platforms check all those boxes. When used to build and improve loan origination software and loan servicing software, these platforms can transform how lenders operate—making them more customer-friendly and responsive to change.

Whether you're a startup lender launching your first product, or a traditional bank modernizing legacy systems, no-code/low-code is no longer just a nice-to-have—it’s becoming a competitive advantage.

Conclusion

The rise of no-code and low-code development is one of the most important shifts in lending technology. By simplifying how software is built and updated, these platforms are unlocking new levels of efficiency and innovation across both loan origination and loan servicing. Lenders who embrace this approach can move faster, serve better, and stay ahead in an industry that never stands still.

Sign in to leave a comment.