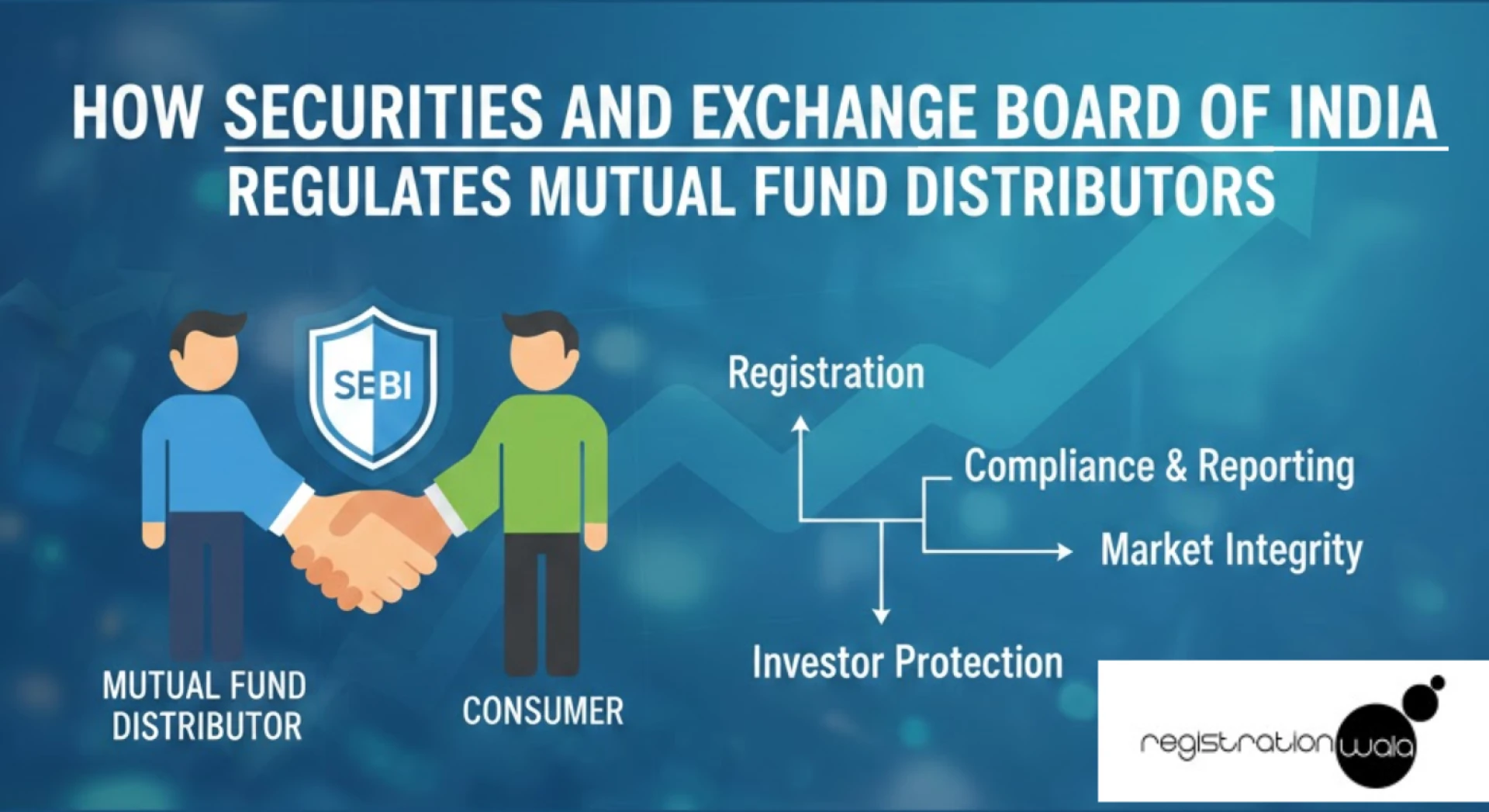

In the Indian financial landscape, Mutual Funds have become the go-to investment vehicle for millions. Behind this massive growth is a dedicated force of Mutual Fund Distributors (MFDs) who bridge the gap between complex financial products and the common investor.

However, handling someone’s hard-earned money is a huge responsibility. To ensure that this "bridge" is built on trust and transparency, the Securities and Exchange Board of India (SEBI) maintains a strict regulatory eye on how anyone can obtain a Mutual Fund Distributor License and operate in the market.

If you are a financial consultant, an insurance agent, or an aspiring entrepreneur looking to start your journey, understanding the "SEBI way" is essential. Here is a humanized, deep-dive guide into the regulatory world of MFDs.

Who is a Mutual Fund Distributor (MFD)?

At its core, a Mutual Fund Distributor is an intermediary who helps investors buy and sell units of mutual fund schemes. Unlike Investment Advisers (who charge a fee for advice), MFDs earn a commission from the Asset Management Companies (AMCs) for the business they bring in.

SEBI views MFDs as the "first point of contact" for investors. Therefore, the regulations are designed to ensure that an MFD is qualified, ethical, and transparent.

The Legal Gateway: How to Get an MFD License

You cannot simply wake up one day and start selling mutual funds. There is a specific legal process involved to acquire a Mutual Fund Distributor License.

Step 1: The NISM Certification

SEBI has mandated that any person wishing to sell or distribute mutual funds must pass the NISM-Series-V-A: Mutual Fund Distributors Certification Examination. This exam tests your knowledge of fund structures, risk factors, legalities, and investment math. It ensures that you aren't just a salesperson, but someone who understands the product.

Step 2: AMFI Registration (ARN)

Once you pass the NISM exam, you don't go back to SEBI directly. Instead, you register with AMFI (Association of Mutual Funds in India). AMFI acts as the primary trade body under SEBI's oversight. Upon successful registration, you are issued an AMFI Registration Number (ARN).

- The ARN is your "License." Without a valid, active ARN, no AMC in India is allowed to pay you a commission or allow you to log in applications.

SEBI’s Code of Conduct for Distributors

SEBI doesn't just give you a license and walk away. Every Mutual Fund Distributor must follow a strict Code of Conduct. Think of these as the "Commandments" of the profession:

- Best Interest of the Investor: An MFD must always recommend products that suit the investor’s risk profile, not the ones that pay the highest commission.

- No "Rebating": You cannot legally share your commission with the client to entice them to invest. This is a serious violation.

- Standardized Disclosures: When you talk to a client, you must disclose that you are a distributor and not an "Investment Adviser" (unless you hold that specific SEBI license too).

- Professionalism: You must ensure that the investor fills out their own forms and understands the "Riskometer" of the fund.

The "Commission" Transparency Rule

Years ago, investors had no idea how much their distributor was earning. SEBI changed that to bring in total transparency.

- Direct vs. Regular Plans: SEBI mandated that every mutual fund must have a "Direct Plan" (for those who don't want a distributor) and a "Regular Plan" (which includes the MFD's commission).

- Disclosure in Statements: The Consolidated Account Statement (CAS) sent to investors now clearly shows the commission paid to the distributor.

- No Upfront Commission: To prevent "churning" (moving a client’s money from one fund to another just to earn more), SEBI banned upfront commissions. Now, MFDs only earn an "All-Trail" commission, meaning you get paid only as long as the investor stays invested. This aligns your success with the investor's success.

Due Diligence Requirements for MFDs

If you are a "Small Advisory Firm" or a "Large Distributor," SEBI requires AMCs to perform Due Diligence on you. If an MFD crosses certain thresholds (like operating in more than 20 locations or managing assets over a certain limit), they undergo a more rigorous audit.

What do they check?

- Your sales practices.

- Whether you are providing "advice" under the guise of "distribution."

- If you have a proper system to handle investor complaints.

Advertisements and Social Media Compliance

In the age of "Finfluencers," SEBI has become very strict about how a Mutual Fund Distributor License holder promotes their services.

- You cannot guarantee returns.

- You cannot use "Catchy" slogans that mislead people into thinking mutual funds are as safe as fixed deposits.

- Every advertisement must carry the standard disclaimer: "Mutual Fund investments are subject to market risks, read all scheme related documents carefully."

If you are active on YouTube or Instagram, remember that SEBI considers these platforms as "Public Forums." Any misleading info can lead to your ARN being suspended.

EUIN: Tracking the Individual Behind the Sale

To ensure accountability, SEBI introduced the Employee Unique Identification Number (EUIN). If you work for a large bank or a firm, your specific ID is attached to every application you process. This way, if a client is "mis-sold" a product, SEBI and AMFI can track exactly which person in the organization was responsible, rather than just blaming the company.

Why This Regulation is Good for You (The Distributor)

At first glance, these rules might seem like a lot of "red tape." But for a serious professional, they are a blessing:

- Eliminates Unethical Competition: Rules keep the "fly-by-night" operators out of the market.

- Increases Public Trust: When investors know the industry is regulated by SEBI, they feel safer investing larger amounts.

- Sustainable Income: The trail commission model ensures that if you take care of your clients, you build a steady, long-term recurring income.

Conclusion

Becoming a Mutual Fund Distributor is one of the most rewarding career paths in the Indian financial sector. However, the MFD License is not a "set it and forget it" document. It represents a commitment to stay updated with SEBI’s evolving circulars and to put the investor’s financial health above everything else.

The regulatory framework is not there to stop you from selling; it is there to ensure that when you sell, you do it with integrity. In a country where financial literacy is still growing, your role as a regulated MFD is crucial in helping India achieve its "Viksit Bharat" (Developed India) goals through smart investing.

Sign in to leave a comment.