In the high-stakes world of commercial real estate development, timing is often cited as the most critical factor for success. However, timing isn't just about when you break ground or when you open your doors to tenants; it is fundamentally about the cost of capital. For developers across the United States, staying ahead of the curve means having a granular understanding of commercial construction loan rates and how they dictate the feasibility of a project from inception to completion.

As we navigate an era of shifting fiscal policies and evolving market demands, the bridge between a blueprint and a finished structure is built on a foundation of strategic financing.

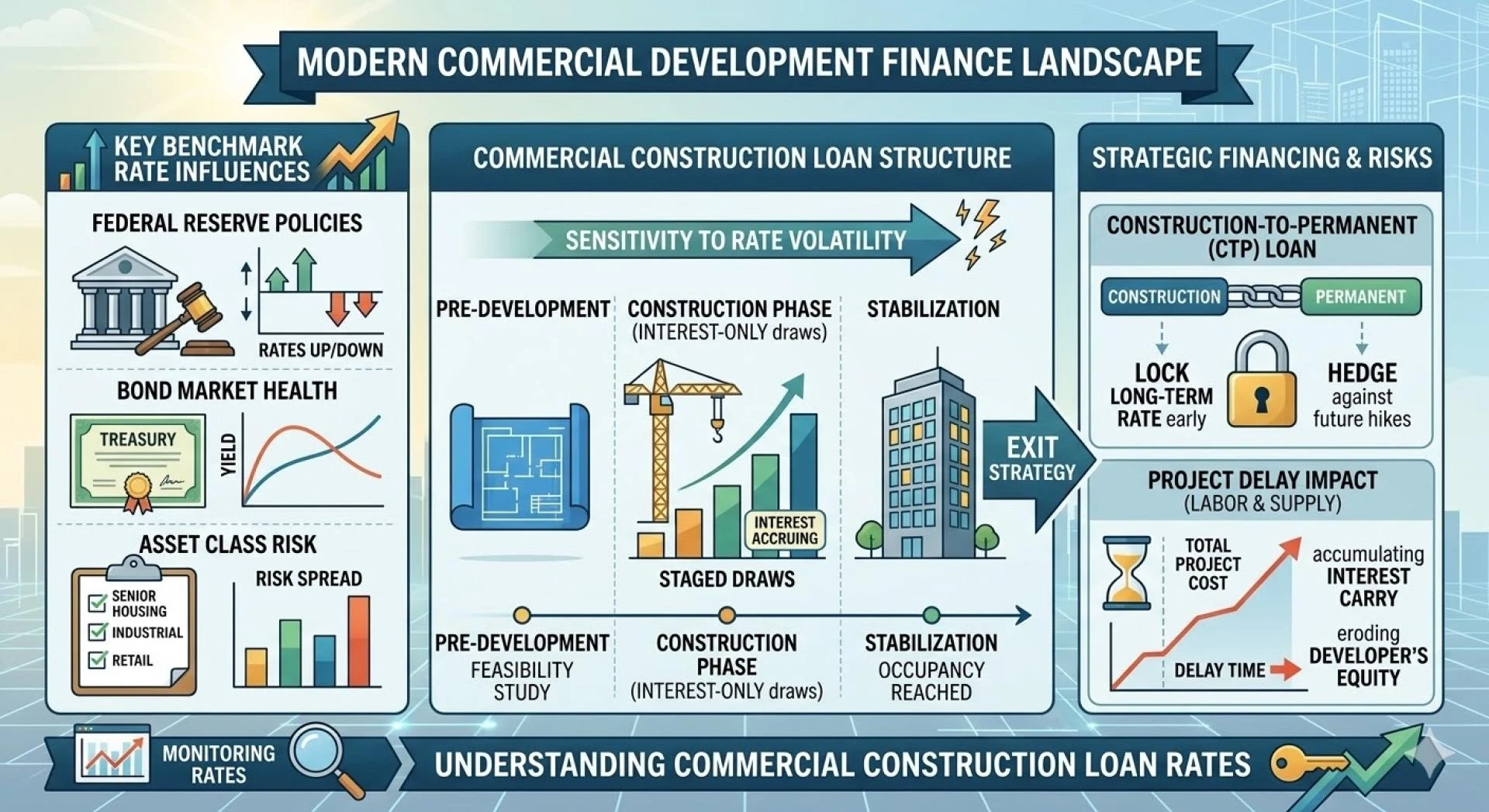

The Sensitivity of Construction Finance

Unlike permanent financing, which is often fixed and predictable, construction financing is inherently sensitive to market volatility. Because these loans are typically "interest-only" and drawn down in stages based on project milestones, even a minor fluctuation in the benchmark rates can have a compounding effect on the total project cost.

When developers monitor commercial construction loan rates, they aren't just looking for a number; they are looking for a window of opportunity. These rates are influenced by a complex cocktail of factors, including Federal Reserve policies, the health of the secondary bond market, and the specific risk profile of the asset class being developed—ranging from industrial warehouses to specialized senior living facilities.

Risk Premium and Asset Specialization

Lenders do not view all commercial projects through the same lens. A standard retail strip center carries a different risk weight than a specialized healthcare or senior housing facility. Consequently, the spread on commercial construction loan rates often reflects the complexity of the project.

Specialized assets, such as assisted living or memory care facilities, require a lender who understands the operational nuances of the "business" within the real estate. Because these projects have higher barriers to entry and more rigorous regulatory requirements, the financing must be structured with more flexibility. This often means looking beyond the "headline" rate to evaluate the total cost of the loan, including origination fees, exit fees, and the terms of the mini-perm transition.

The Transition from Construction to Permanent Debt

One of the most overlooked aspects of development finance is the "exit strategy." A construction loan is a means to an end, intended to be replaced by long-term permanent debt once the property achieves stabilization (a specific occupancy threshold).

Sophisticated developers use current commercial construction loan rates as a starting point, but they keep a close eye on the "cap rate" environment. If construction costs rise due to interest spikes, the project must either achieve higher rents or find operational efficiencies to remain viable. This is why many developers are now opting for "construction-to-permanent" (CTP) loans, which lock in the long-term financing at the start of the build, providing a hedge against future rate hikes.

Inflation, Labor, and the Cost of Delay

In 2026, the cost of construction isn't just about the loan rate; it’s about the time-value of money. Labor shortages and supply chain recalibrations have made project timelines less predictable. When a project is delayed by six months, the interest carry on the loan continues to accumulate.

In an environment where commercial construction loan rates are elevated, a delay isn't just a scheduling inconvenience—it’s a direct erosion of the developer’s equity. Efficient project management and a transparent relationship with the lender are essential to ensuring that "draws" are processed quickly and that the project remains on a path toward stabilization without unnecessary interest expenses.

Data-Driven Development

The developers who will define the skyline of the late 2020s are those who treat financing as a dynamic component of the build, rather than a static administrative hurdle. By maintaining a deep connection to the trends affecting commercial construction loan rates, investors can make informed decisions about when to pivot, when to hold, and when to go all-in on a new development.

As specialized sectors like senior housing continue to offer resilient returns, the role of specialized lenders—those who can provide nuanced rates and flexible terms—becomes the most valuable asset in a developer's portfolio. In the end, a successful project is one where the financial architecture is as sturdy and well-planned as the physical structure itself.

Sign in to leave a comment.