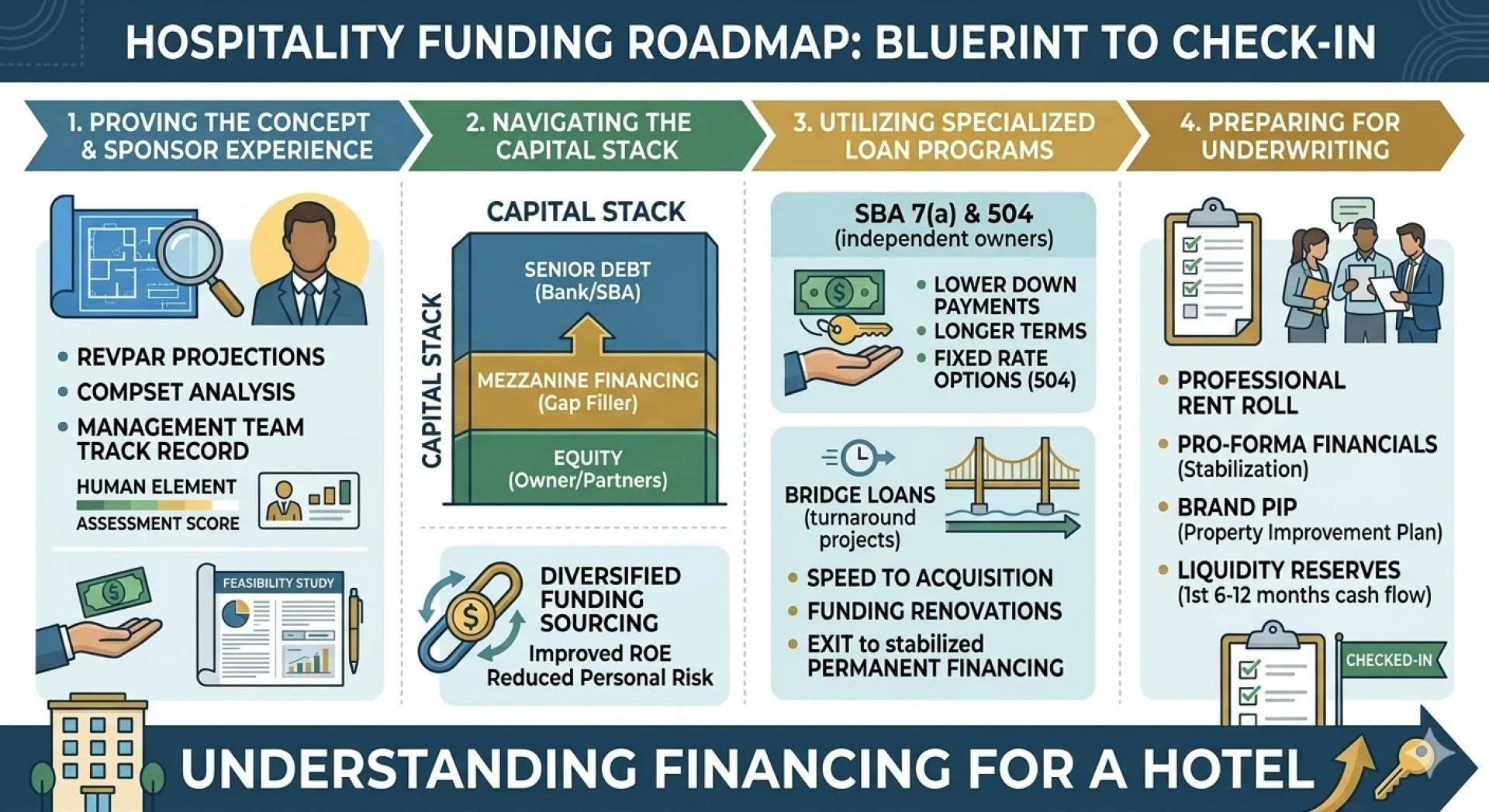

In the current real estate cycle, the transition from "vision" to "vertical construction" is more complex than ever. While the demand for high-quality housing remains at an all-time high, the capital markets in 2026 have become increasingly selective. For developers, success no longer depends solely on a prime location; it depends on a bulletproof financial structure that addresses the modern lender's primary fears: cost overruns and absorption delays.

The Shift from Speculation to Stability

Two years ago, "pro-forma" projections were often accepted with minimal scrutiny. Today, institutional and private lenders are performing deep-dive audits into supply chain resilience and local labor availability. Developers who win the best rates are those who present a "Guaranteed Maximum Price" (GMP) contract from a bonded general contractor before even entering the term sheet phase.

Lenders are also looking for a higher "Debt Yield"—a metric that measures the return the lender would receive if they had to take over the property today. In 2026, a target debt yield of 8% to 10% is becoming the new benchmark for secondary markets.

Solving the "Capital Gap"

One of the most significant hurdles in today’s market is the widening gap between the cost of land acquisition and the start of the build. Traditional banks have pulled back on leverage, often capping their participation at 60% LTC (Loan-to-Cost). This leaves developers searching for creative ways to fill the remaining 40% without over-diluting their equity.

To navigate these hurdles, sophisticated developers are moving away from local retail banks and toward specialized platforms that offer tailored ground up construction loans with non-recourse options. These specialized vehicles allow for a higher "leverage-to-value" ratio, often incorporating mezzanine debt or preferred equity into a single, seamless closing process. This integrated approach reduces the friction of dealing with multiple lienholders and speeds up the "first shovel" date.

The 2026 Underwriting Checklist

Before submitting a file to a specialized lender, ensure the following "stress tests" are addressed in your package:

- Sensitivity Analysis: How does the project perform if interest rates rise by another 50 basis points during the 24-month build cycle?

- The "ESG" Premium: Does the design include high-efficiency HVAC or LEED-certified materials? Lenders in 2026 are offering "Green Discounts" of up to 0.25% on interest rates for sustainable builds.

- Contingency Reserves: Standard 5% contingencies are often insufficient now. A robust 10% hard-cost contingency is the current gold standard for earning lender trust.

- The Exit Narrative: Is the local "Rent-vs-Own" gap wide enough to support your pro-forma rents? Lenders are prioritizing projects in submarkets where mortgage payments for a comparable condo are at least 30% higher than the projected apartment rent.

The Future of the "Build-to-Core" Strategy

The ultimate goal for most 2026 developers is the "Build-to-Core" strategy—constructing a high-quality asset with the intent to hold it as a long-term cash-flow vehicle. By securing a flexible construction-to-permanent loan structure, you can bypass the "refinance risk" that plagues many short-term flippers.

The key is to align with a lending partner who understands that a construction project is a living entity. It requires "Draw" schedules that match the reality of modern site work and an underwriting team that values the developer's experience as much as the appraisal.

Pro-Tip for Developers

If you are preparing your 2026 development pipeline, remember that the "Pre-Development" phase is your best time to negotiate. Secure your term sheet early to lock in your spread against the SOFR (Secured Overnight Financing Rate).

Sign in to leave a comment.