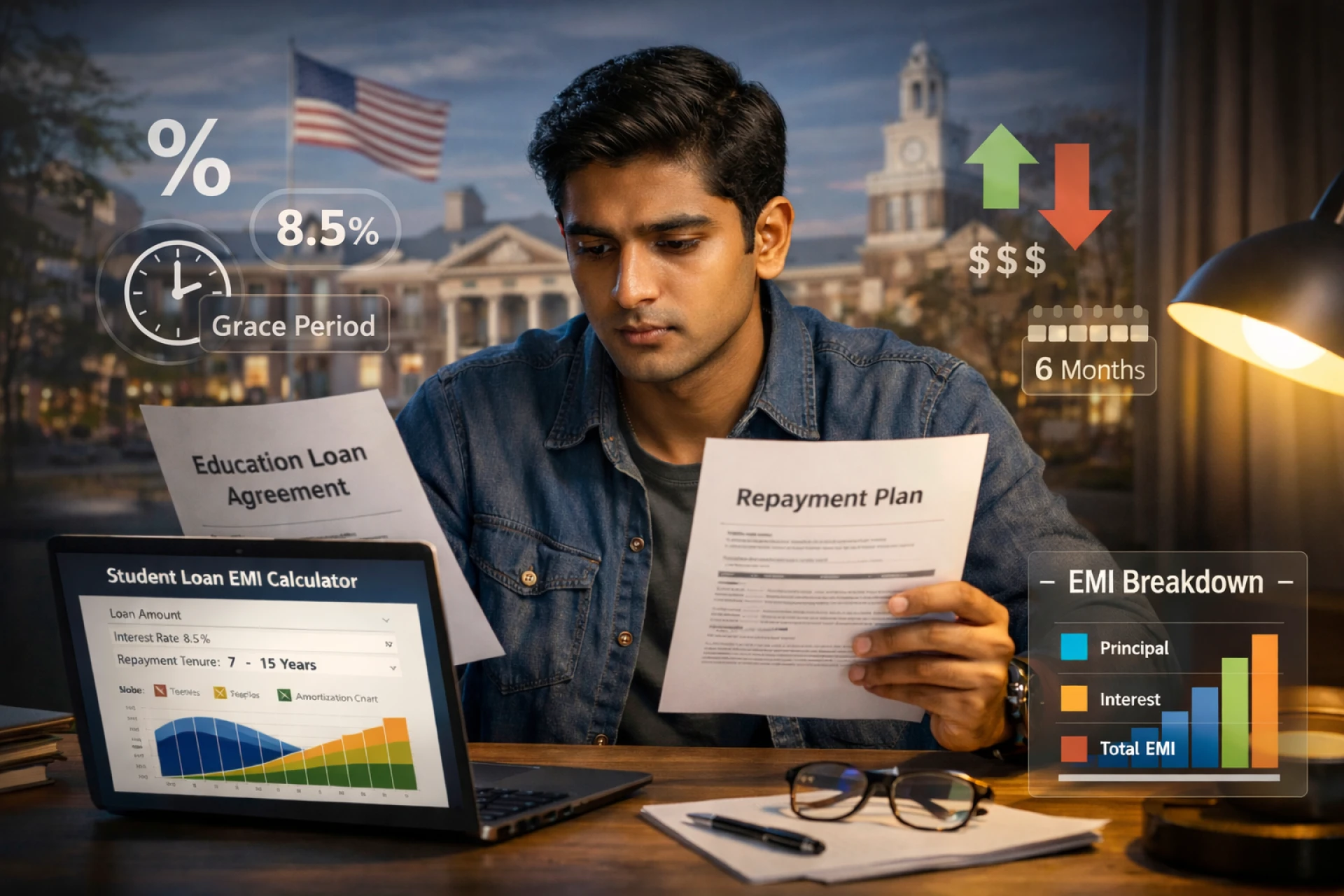

Funding a degree abroad is not cheap. Between tuition, housing, travel, and living expenses, most students are looking at anywhere from ₹30 lakhs to well over ₹1 crore depending on the country and university. That means the interest rate on your education loan is not just a number — it is a decision that follows you for years after graduation.

So let us get into what rates actually look like in 2026, who is charging what, and whether you can realistically get under 10%.

What Are Current Study Abroad Loan Interest Rates?

The honest answer: Foreign education loan interest rate depends heavily on the lender type, whether you offer collateral, your co-applicant's profile, and which country you are going to.

Here is a rough breakdown of where rates typically fall in 2026:

- Public sector banks (SBI, Bank of Baroda, Bank of India): 9% – 11.5%

- Private banks (HDFC, Axis, ICICI): 11% – 13.5%

- NBFCs (Avanse, Credila, InCred): 11% – 14%

- International lenders (MPOWER, Prodigy Finance): 9% – 15% (USD-denominated, no collateral)

The sub-10% bracket is real, but it is not guaranteed. You earn it with the right profile, the right lender, and sometimes with collateral on the table.

The Collateral Question: Does It Actually Lower Your Rate?

Yes — significantly. A collateral free education loan for abroad typically carries a higher interest rate because the lender is taking on more risk. Most banks price that risk at 1.5% to 3% above their secured loan rates.

That said, the collateral free education loan for abroad market has grown considerably. Lenders like Avanse and Prodigy Finance have made it their core product. MPOWER specifically targets students at top-ranked universities in the US and Canada and does not ask for collateral or a co-signer at all.

If you are okay with pledging property or fixed deposits, you will almost always get a better rate from a public bank — sometimes as low as 9.5% or even slightly under for premium institutions like IITs going abroad or admits to Ivy League schools.

If collateral is not an option, focus your energy on lenders who have built underwriting models around your admit and employability — not just your family's assets.

Education Loan for Abroad Eligibility: What Lenders Look At

Before embarking on the process of comparison, it’s important to ensure that you’re able to clear the baseline threshold. Qualifications for education loan for abroad depend from one lender to another, but the typical ones include the following:

- University ranking: The top 100 QS or THES rankings help unlock better rates

- Program of study and area of study: Students enrolled in engineering, management, healthcare, and other popular streams fare well.

- Income of co-borrower: Majority of Indian banks will require a co-applicant who earns stable income

- Educational qualifications: Consistent marks up until 10th, 12th, and university levels help

- Entrance exam scores: High scores in GRE, GMAT, IELTS, and TOEFL indicate employability

- Country of education: US, UK, Canada, Australia, and Germany are favorites amongst lenders

The education loan for abroad eligibility bar is not impossible to clear, but you need to present your application as a package — admit letter, co-applicant documents, and a clear repayment logic all bundled together.

Overseas Education Loan: Public Banks vs. NBFCs in 2026

The debate between banks and NBFCs for an overseas education loan is less about who is better and more about what your situation looks like.

Public Banks are better if:

- You have collateral to offer

- Your co-applicant has formal, salaried income

- You are applying to a university they already have on their approved list

- You can wait — public bank processing takes longer but rates are worth it

NBFCs are better if:

- You require faster processing time (some take just 7–10 business days)

- Your university is relatively new or specialized

- You prefer options in the loan repayment schedule

- You lack collateral but have an impressive profile

The sweet spot for most students is starting with SBI or Bank of Baroda, getting a sanction letter if possible, and then using that as leverage when comparing offers from NBFCs. You will know exactly what you are giving up or gaining on interest.

Which Lenders Are Under 10% in 2026?

Here are the ones where sub-10% is actually achievable:

- SBI Global Ed-Vantage: Beginning at 9.15% for collateralized loans to premier institutes

- Baroda Scholar (Bank of Baroda): Beginning at 9.20% for certain nations and institutions

- Union Bank of India: Very competitive rates below 10% for secured loans, particularly for US/UK admissions

- Axis Bank (select applicants): Sometimes falls below 10% for collateralized loans with high co-applicant incom

Note that these are base rates — your actual offered rate could be higher depending on risk assessment.

A Word on Overseas Education Consultants

Many students first learn about loan options through Overseas Education Consultants — and that makes sense. A good consultant handles your university shortlisting, visa, and sometimes loan referrals all at once.

Here’s what you should be careful about when using the services of Overseas Education Consultants: Some of them might have deals with particular lending companies and try to persuade you into borrowing their money, even if that’s not what is right for you.

Always compare independently. A referral from a consultant is a starting point, not the final word.

Use consultants for what they are genuinely good at — applications, SOPs, visa prep, and university research. For the loan itself, do your own comparison or use a neutral loan comparison platform.

Plan Your Loan Before You Plan Your Packing

The best time to start researching your loan is the moment you start shortlisting universities — not after you get your admit. Rates, processing times, and eligibility decisions all take time. The students who get the best deals are usually the ones who started early, compared seriously, and did not just go with whoever the consultant recommended.

Sign in to leave a comment.