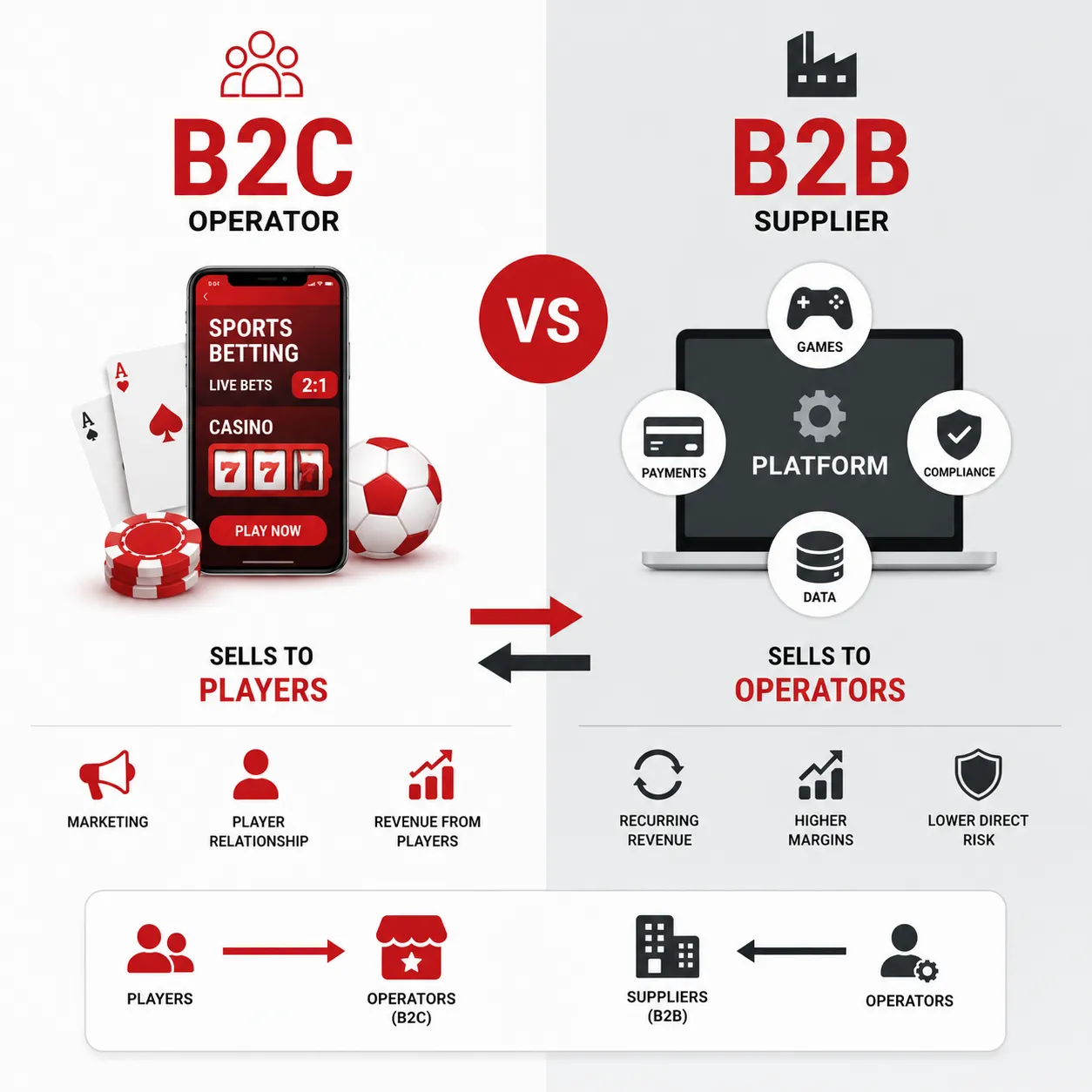

The difference between B2B and B2C iGaming comes down to who the customer is. B2C companies are the operators, the casino and sportsbook brands that take bets directly from players. B2B companies are the suppliers that sell games, platforms, and payment technology to those operators. One sells to players, the other sells to the companies that sell to players.

Ask most people to picture the iGaming industry and they'll describe a brand: the sportsbook on a stadium hoarding, the casino app dangling a welcome bonus, the betting site that seems to own a season. These are the businesses the public knows. They're also only half the story.

Sitting behind every brand a player ever touches is a second company the public almost never notices. It builds the platform, supplies the games, moves the money, and deals with the compliance headaches. It never meets a single gambler and never spends a cent on player marketing. And in 2026, this quieter half is often the more stable and more profitable of the two. That split, between the companies players see and the companies quietly powering them, decides how money moves, where the risk lands, and which businesses are actually built to win.

B2B vs B2C iGaming: operators and suppliers defined

B2C, business to consumer, is the operator. It's the brand that takes bets directly from players. Casinos, sportsbooks, poker rooms, and the apps where users deposit and play. Its customer is the gambler, full stop.

B2B, business to business, covers the companies that sell to operators instead of players:

- Game studios such as Evolution and Pragmatic Play, which produce the slots and live dealer titles that fill an operator's lobby

- Platform providers like Playtech, which supply the underlying technology an operator runs on

- Payment, data, and compliance firms, which handle deposits, odds feeds, KYC, and anti-money-laundering checks

Their customer is the operator, not the player. Most explanations stop right at this definition. But the definition isn't the interesting part. Follow the money and the real difference shows up.

B2B vs B2C iGaming compared at a glance

| Factor | B2C (Operator) | B2B (Supplier) |

| Customer | The player | The operator |

| Examples | Casinos, sportsbooks, poker rooms, betting apps | Game studios, platform providers, payment and compliance firms |

| Revenue model | Player deposits and losses | Revenue share or licensing fees |

| Revenue stability | Volatile, swings with player results | Recurring and predictable |

| Typical margin | Thinner, eroded by marketing and tax | Higher and steadier |

| Player acquisition cost | High and rising | None |

| Regulatory exposure | Direct and heavy | Indirect and limited |

| Core asset | The player relationship and brand | The product and its distribution |

The table lays out the split cleanly, but the reasoning behind it is where the real story sits.

Follow the money: who profits in B2B vs B2C iGaming

A B2C operator lives or dies on player acquisition. Growth means heavy spending to bring players in, then a constant grind to keep them. In competitive regulated markets, signing up a single real-money player can cost a serious sum before that player has placed one bet, and those costs have climbed sharply as ad platforms restrict gambling promotion and competition for high-intent search traffic intensifies. Then revenue swings with results, and a run of big player wins over one weekend can dent the whole month.

On top of that, the operator carries the marketing budget, the player liability, and the full weight of regulation in every market it touches. And that weight is heavy. In some jurisdictions, gambling taxes claim a punishing share of gross gaming revenue, and the toughest sports betting regimes take more than half. When a regulator tightens the rules or a tax rate climbs, the operator feels it first. And hardest.

A B2B supplier sits somewhere completely different. It gets paid by the operator, usually through revenue share or licensing, whether the operator wins or loses against players. Its income is recurring and far easier to predict. It carries no acquisition costs and sits outside the direct line of player-facing regulation. A studio pushing content to hundreds of operators barely notices any single weekend's results, while an individual operator can be badly stung by one.

The margin gap tells the story better than anything. Evolution, the largest live casino supplier, runs at EBITDA margins in the mid-sixties percent, serving hundreds of operators from studios across four continents. That is a level of profitability most consumer-facing operators cannot come close to, because suppliers aren't the ones absorbing the marketing spend or the player risk. It's a familiar pattern across the industry. An operator posts a strong month for deposits and still watches most of the margin vanish into acquisition costs and tax.

This has become impossible to ignore in 2026. Running a B2C brand keeps getting more expensive:

- Marketing costs climb as ad platforms restrict gambling promotion; Google alone made 18 policy changes to gambling advertising in 2025

- Tax rates rise across several regulated jurisdictions

- Licensing and compliance requirements tighten, with KYC and AML now a purchase-order priority rather than an afterthought

At the same time players expect faster withdrawals, better products, and safer experiences, all of which push operator costs up again. The visible brands work harder for thinner margins while the suppliers behind them earn more steadily. In plenty of cases, a company no player has ever heard of pulls in more reliable revenue than the brand they open every day.

Why B2C operators still exist despite the supplier advantage

Fair question. If the supplier model is that much more comfortable, why choose the operator life at all?

The answer is the one asset suppliers can only ever rent. The player.

The operator owns the customer relationship, the data, the brand, and the direct line to the gambler. That's the single most valuable thing in the industry. A supplier can be swapped out for a cheaper competitor next quarter. A brand that players trust and keep coming back to is far harder to dislodge. And when an operator hits real scale, the upside dwarfs what a content studio earns on revenue share.

Neither model is better. They're different bets. B2B is a bet on stability and margin. B2C is a bet on scale and ownership.

How iGaming operators choose B2B suppliers in 2026

The way operators find and choose their suppliers has shifted, and it mirrors what's happened everywhere else in B2B. Business buyers now start their research online, comparing providers through digital channels long before anyone picks up a phone. iGaming is no exception. An operator hunting for a platform, a payment partner, or a game supplier in 2026 increasingly begins with a search query, not a handshake at a trade show.

For suppliers, that changes the game. A great product is no longer enough on its own. If a supplier doesn't show up where operators research and build their shortlists, it may as well not exist to that buyer. Visibility has become a commercial necessity, not a marketing nicety.

The balance also shifts by market. A few examples make the point:

- Brazil opened its regulated market in January 2025 under Law 14.790/2023, bringing one of the world's largest populations into the regulated fold with a GGR-based tax and steep licensing fees. Compliance, local payment methods like PIX, and brand trust jumped to the top of operators' priority lists overnight, and demand for suppliers who could deliver them spiked with it.

- The United States still drives growth mainly through sports betting, with online casino gaming legal in only a handful of states. That creates a very different supplier opportunity from a full-casino market.

- Europe, the largest region by revenue, is seeing growth slow as mature markets tighten advertising codes and impose bonus caps, which pushes suppliers to prove compliance credentials rather than just product quality.

The B2C and B2B relationship isn't the same everywhere. It bends to each market's rules, payment habits, and maturity.

Why the line between B2B and B2C iGaming is blurring

Here's the clearest signal of where all this is heading. The line between operators and suppliers is starting to disappear.

Many of the biggest companies now play both sides at once. Operators are building their own platforms rather than renting them. Suppliers like Evolution have grown by buying up other studios, including NetEnt and Big Time Gaming, to assemble one-stop content portfolios. And in white-label arrangements, a single company can run a whole cluster of nominally separate casinos that look like rivals while sharing the same engine underneath.

So the 2026 reality is messier than a tidy two-sided model suggests. The best-positioned companies work in both worlds, banking the stable margins of the supplier business alongside the brand and player ownership of the operator business.

What B2B vs B2C iGaming means for investors, affiliates, and operators

Which model matters more depends entirely on your seat:

- For investors, it's a choice between two risk profiles. Operators offer higher potential upside but come with volatile revenue and heavy regulatory exposure. Suppliers offer recurring income and lower direct risk, even if they rarely make the headlines.

- For affiliates, it shapes who they partner with. The operator owns the player relationship and pays the commission, but the player experience that drives retention, and therefore affiliate revenue, often rests on the suppliers working out of sight. Anyone tracking how these partnership and commercial dynamics play out can follow the marketing and affiliates coverage, where the deals shaping this side of the business surface first.

- For newcomers to the industry, it clarifies the work itself. The B2C side is fast, marketing-led, and built around player acquisition. The B2B side is more technical, more stable, and far less visible.

- For operators, the message in 2026 is blunt. With margins under real pressure, supplier selection has stopped being an operational detail. It's now a decision that can shape commercial survival.

The future of B2B and B2C iGaming

The difference between B2B and B2C iGaming was never really about who sells to whom. That's the definition, not the substance. The substance is in how revenue behaves, where risk piles up, and which businesses quietly profit while public attention stays glued to the brands.

The bigger question for the next few years isn't B2B versus B2C. It's how much longer the separation between them lasts. Over the next six to twelve months, expect more operators to build platform capability in-house and more suppliers to broaden their portfolios. The convergence is already in motion, and regulatory and cost pressures are only speeding it up. Keeping an eye on the latest industry coverage is the simplest way to watch it unfold in real time.

The companies best placed in 2026 are the ones that have stopped choosing a side. As that convergence rolls on, the most powerful names in iGaming may increasingly be the ones you can't cleanly file as either operator or supplier.

Frequently Asked Questions

What does B2C mean in iGaming?

B2C, or business to consumer, refers to the operator. It's the brand that takes bets directly from players, including casinos, sportsbooks, poker rooms, and betting apps. Their customer is the gambler, and their business runs on acquiring and retaining players.

What does B2B mean in iGaming?

B2B, or business to business, refers to the companies that sell to operators rather than players. This includes game studios like Evolution and Pragmatic Play, platform providers such as Playtech, payment firms, data and odds feeds, and compliance tools. Their customer is the operator, not the player.

Which is more profitable, B2B or B2C iGaming?

B2B suppliers generally earn steadier, more predictable margins because they get paid whether an operator wins or loses against players, and they carry no player acquisition costs. The largest live casino suppliers run at margins operators rarely match once acquisition costs and tax are accounted for. B2C operators can reach far higher upside at scale, but they absorb the marketing spend, the player liability, and the regulatory burden. Neither is universally better. They're different bets on stability versus scale.

Why do operators still exist if suppliers carry lower risk?

Because operators own the one asset suppliers can only rent: the player. The customer relationship, the data, the brand, and the direct connection to the gambler are the most valuable assets in the industry, and a trusted brand is far harder to replace than a supplier. At scale, the operator's upside can dwarf what a supplier earns through revenue share.

Why is player acquisition so expensive for iGaming operators?

Acquiring a real-money player in a competitive regulated market has become costly and keeps rising, driven by tightening platform restrictions on gambling promotion, higher compliance requirements, and intense competition for high-intent search traffic. This is a core reason the operator model carries thinner margins than the supplier model.

Are B2B and B2C iGaming companies merging into one model?

Increasingly, yes. Many of the largest companies now operate on both sides. Operators are building their own platforms, suppliers are acquiring studios to expand their portfolios, and white-label setups run multiple casinos on shared technology. The clean two-sided split is breaking down, and the best-positioned firms in 2026 work across both.

Why does supplier selection matter more for operators in 2026?

With marketing costs climbing, tax rates rising, and licensing tightening, operator margins are under real pressure. The suppliers behind the scenes shape product quality, payment experience, compliance, and retention, so choosing the right ones has moved from an operational detail to a decision that can affect commercial survival.

How does the B2B and B2C balance differ by market?

It varies with each market's regulation, payment behavior, and maturity. In Brazil, the market opening in January 2025 pushed compliance, local payments, and brand trust to the top of operator priorities. In the United States, growth still comes mainly from sports betting, since online casino gaming is legal in only a limited number of states, which creates a different supplier opportunity than markets where online casino is widely available.

Sign in to leave a comment.