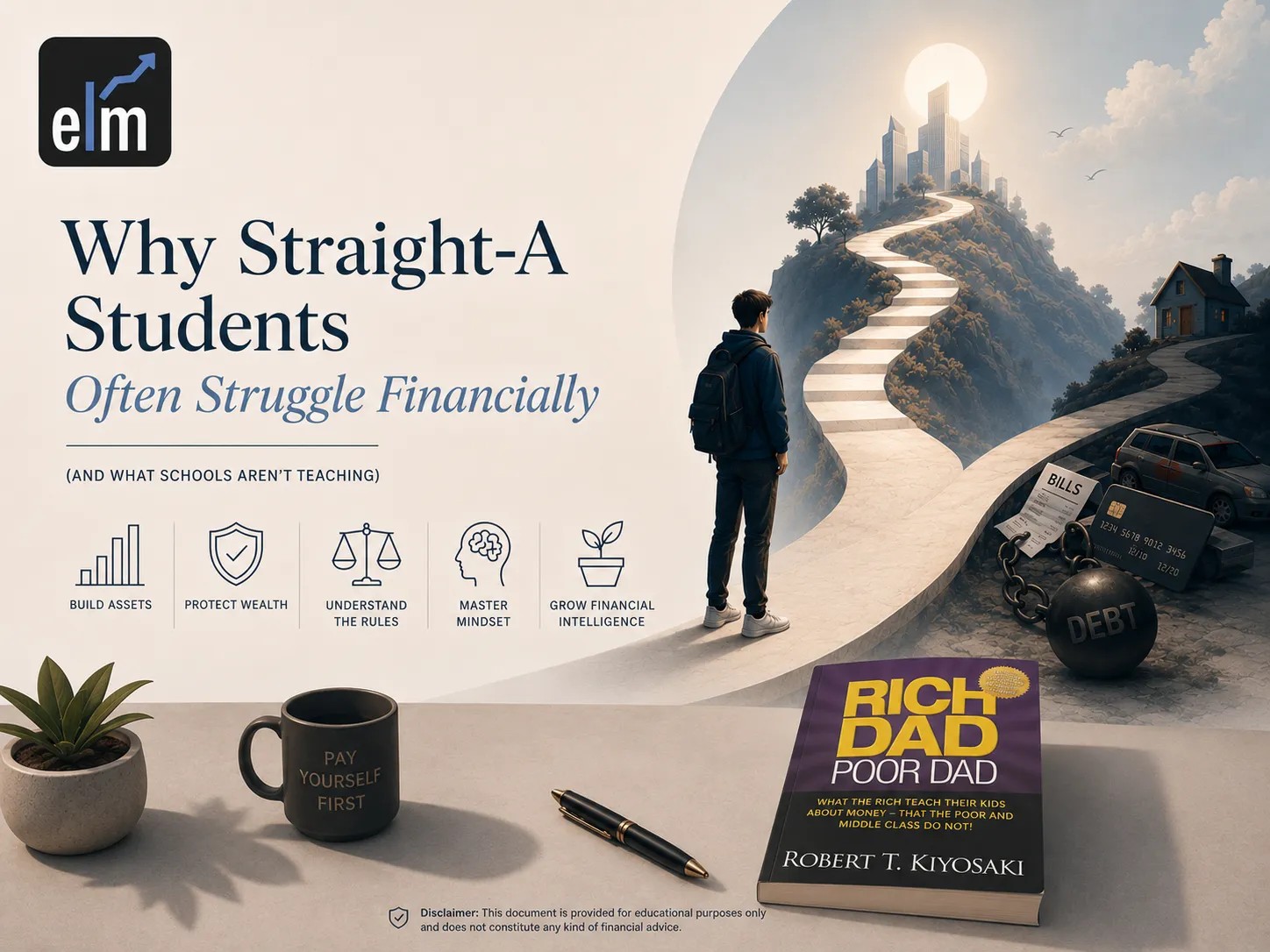

We’ve all seen the archetype: the student who never missed a deadline, aced every calculus exam, and graduated with honors, only to find themselves ten years later drowning in credit card debt and living paycheck to paycheck. Meanwhile, the kid who spent half of high school in detention is somehow managing a portfolio of rental properties.

It feels like a glitch in the system. If schools are designed to prepare us for the "real world," why do they leave out the one thing we use every single day?

According to the core philosophy in Rich Dad Poor Dad by Robert Kiyosaki, the answer is simple: our education system was built to produce employees, not employers. It teaches us how to work for money, but it completely ignores how to make money work for us.

The Gap: Professional Skills vs. Financial IQ

Most modern curricula are excellent at teaching professional skills. We learn how to be doctors, engineers, or middle managers. These skills are vital for the "Poor Dad" philosophy: studying hard to find a stable company and a steady paycheck.

However, there is a massive chasm between being a high-income professional and being financially literate. As the book summary points out, smart students often struggle because they haven't been taught Financial IQ. This isn't just about "saving money"; it's a combination of four specific pillars:

- Accounting: The ability to read and understand financial statements.

- Investing: The science of money making money.

- Understanding Markets: Knowing the patterns of supply and demand.

- The Law: Understanding how to use corporations and tax structures to protect wealth.

Without these, a Straight-A student is essentially a high-performance engine with no steering wheel. They earn a lot, but they have no idea how to keep it.

The Trap of the "Asset"

One of the most profound flaws in our education is the failure to define an asset correctly. In school, we are taught that a house is an asset. In the world of high-level finance, as Robert Kiyosaki argues, a house is often a liability because it takes money out of your pocket every month via mortgages, taxes, and maintenance.

"The rich acquire assets. The poor and middle class acquire liabilities that they think are assets."

Because schools don't teach the difference between an asset and a liability, graduates enter the workforce and immediately fall into the "Rat Race." They get a raise, so they buy a bigger car. They get a promotion, so they buy a bigger house. Their expenses rise to meet their income, leaving them perpetually stuck working for someone else just to stay afloat.

The Power of "The Asset Column"

Wealth isn't defined by the size of your paycheck but by the strength of your asset column. True financial freedom is achieved when the cash flow generated by your assets (stocks, bonds, rental properties, or intellectual property) exceeds your monthly expenses.

Why Financial Literacy Must Be a Core Subject

If we taught financial literacy with the same rigor we apply to history or biology, the economic landscape would look drastically different. Currently, we leave "money talk" at the dinner table which is a problem if your parents also grew up in a system that prioritized security over financial freedom.

The ELM School summary highlights that the rich "invent money" by seeing opportunities that others miss. This isn't magic; it's a trained mindset.

1. Overcoming the Fear of Risk

Schools punish mistakes. If you fail a test, your GPA drops. In the real world of wealth, winners are inspired by loss. Financial education would teach students how to manage risk rather than simply avoiding it.

2. Understanding Taxes and Corporations

Most employees work from January to May just to pay the government. The rich, through the power of corporations, earn, spend, and then pay taxes on what’s left. This is a legal, fundamental piece of "minding your own business" that is almost never whispered in a high school classroom.

3. The Importance of Financial History and Law

To master money, you must understand the rules of the game. This includes the history of how taxes were originally intended for the wealthy but shifted to the middle class, and the legal protections offered by corporations (such as limited liability and asset protection). Knowledge of the law is the shield that protects your wealth from being eroded by "the taxman" and legal predators.

4. Paying Yourself First

The concept of paying yourself first is a psychological shift. It teaches self-discipline. Instead of paying the bills and saving "what's left," you invest in your asset column first, which forces you to get creative and work harder to cover your remaining expenses.

5. Work to Learn, Not to Earn

In the early stages of a career, prioritize roles that offer high-value skill acquisition over immediate high pay. Seek out learning positions in sales, marketing, and leadership. These skills are portable and provide the infrastructure needed to eventually run your own business, whereas a specialized technical skill may only make you a better employee.

The Final Lesson: Mindset Over Mechanics

At the end of the day, the biggest flaw in modern education isn't just a missing textbook; it's a missing mindset. As the author states, "Broke is temporary, poor is eternal."

A student can be broke while they build their business, but as long as they have a high financial IQ, they aren't poor. True wealth comes from the mind. Until our schools stop treating money as a taboo subject and start treating it as a vital life skill, we will continue to see brilliant, hard-working people trapped in a cycle of financial stress.

If you want to move beyond the resume-building cycle, the first step is to mind your own business, meaning focus on your asset column as much as your career. Your diploma might get you the job, but only your financial education will get you the freedom.

Cultivating a "Wealthy Mindset"

The greatest asset we all have is our mind. If trained well, it can create enormous wealth in what seems like an instant. Conversely, an untrained mind can lose a fortune just as quickly. Financial intelligence is simply the ability to see opportunities where others see risks and to have the discipline to act on them while others remain paralyzed by fear.

Disclaimer: This document is provided for educational purposes only and does not constitute any kind of financial advice.

Sign in to leave a comment.