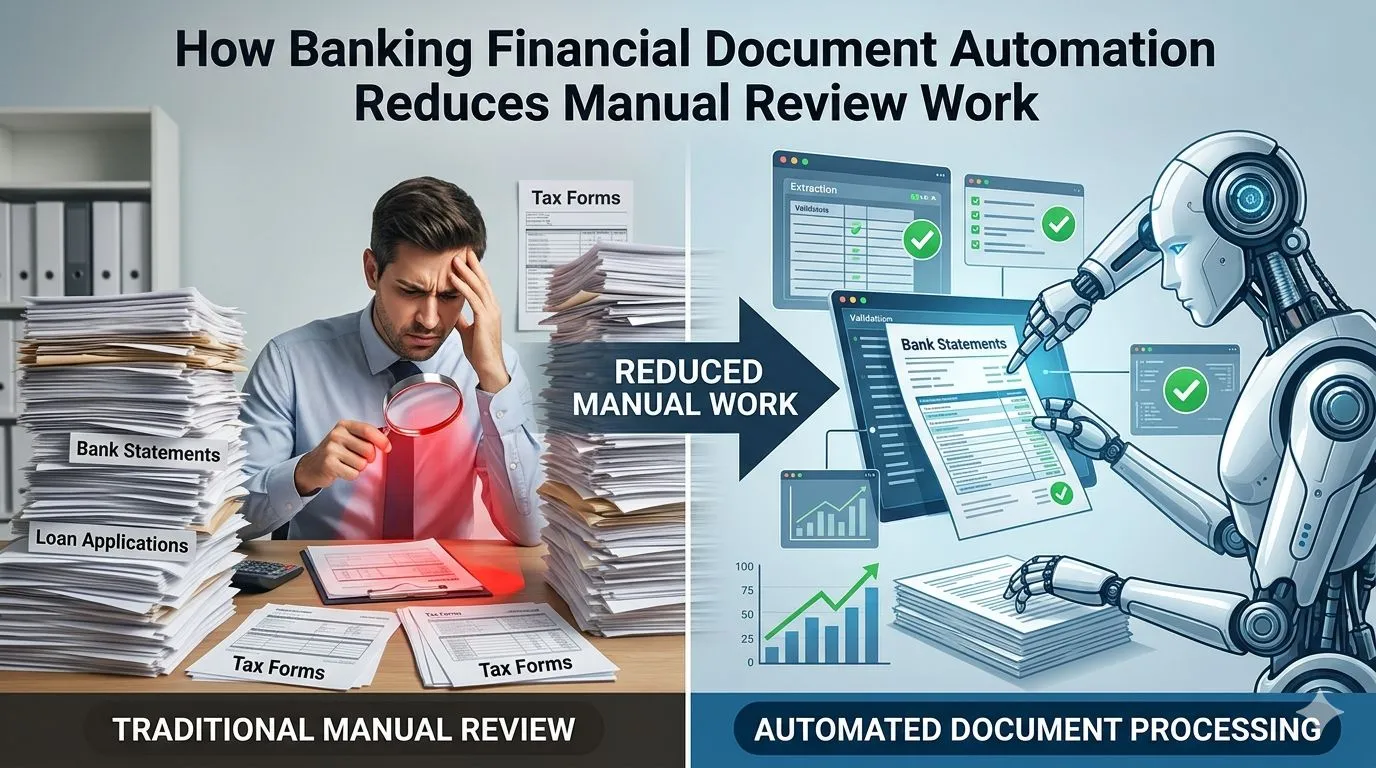

Banks process thousands of customer records, loan files, identity documents, statements, tax proofs, and compliance files every day. The problem starts when teams review these documents manually, enter the same data into multiple systems, and chase missing fields across emails and folders. This slows onboarding, loan processing, credit review, and audit preparation.

Banking financial document automation helps reduce manual review work by capturing data, validating fields, routing exceptions, and keeping source links intact. This blog explains how automation supports onboarding, loan processing, credit review, compliance, and banking operations while keeping human review in place for risk and approval decisions.

What Is Banking Financial Document Automation?

Banking financial document automation is the use of digital workflows and AI-based document reading to process banking documents with less manual effort.

Banking Financial Document Automation Definition

Banking financial document automation means capturing, classifying, extracting, validating, and routing banking documents for review and downstream processing.

How Document Automation Converts Banking Files Into Usable Data

It turns PDFs, scans, spreadsheets, forms, and statements into structured fields such as name, account number, income, balance, tax value, facility amount, and document date.

Why Manual Document Review Slows Banking Operations

Manual review slows operations because teams must read files, enter values, verify fields, check missing documents, and send exceptions for approval.

This is why many banks still rely on human review even when some parts of the process are digital.

Why Banks Still Depend on Manual Document Review

Banks still depend on manual document review because banking files vary widely and many decisions need human judgement.

High Document Volume Across Banking Teams

Onboarding, lending, credit, compliance, audit, and operations teams all handle large document volumes.

Varied File Formats Across Customers and Products

Customer files arrive as scans, images, PDFs, emails, spreadsheets, and product-specific forms.

Legacy Systems With Limited Data Connectivity

Older banking systems may not connect easily with document platforms, loan systems, or core banking records.

Compliance Checks That Need Human Oversight

Compliance review often needs human judgement for exceptions, high-risk customers, policy differences, and escalations.

Manual review appears across several banking workflows, not just one department.

Where Manual Review Work Happens in Banking

Manual review work appears wherever banking teams handle documents, validate data, and make decisions.

Customer Onboarding and KYC Review

Teams review identity proofs, address documents, ownership records, and customer declarations.

Loan Application Document Review

Loan teams check application forms, borrower details, income records, and supporting documents.

Bank Statement and Transaction Review

Analysts review account activity, balances, inflows, outflows, and transaction patterns.

Financial Statement Review

Credit teams review balance sheets, income statements, cash flow statements, schedules, and notes.

Trade Finance Document Checking

Trade teams compare letters of credit, invoices, bills of lading, packing lists, and shipment records.

Compliance and Audit Evidence Collection

Compliance and audit teams collect source documents, approvals, review history, and control evidence.

These review steps often create repeated work and operational delays.

Key Problems With Manual Banking Document Review

Manual banking document review creates delays, errors, duplicated effort, and weak traceability.

Slow Turnaround Time

Manual review can delay onboarding, loan approval, trade processing, and compliance checks.

Repeated Data Entry Across Systems

The same customer or borrower data may be entered into multiple banking systems.

Missing or Incorrect Document Fields

Incomplete files, unclear scans, and wrong values can create review delays.

Duplicate Checks Across Teams

Different teams may review the same document fields more than once.

Weak Traceability From File to Decision

Manual workflows can make it hard to prove which document supported a decision.

Document automation reduces this work by structuring the process from the first file intake.

How Banking Document Automation Reduces Manual Review Work

Banking document automation reduces manual review by handling intake, classification, extraction, validation, and exception routing.

Automated Document Intake

Documents are collected from portals, emails, branches, and relationship managers in a controlled workflow.

Document Classification by Type and Purpose

Files are classified as KYC documents, statements, tax proofs, loan forms, audit reports, or collateral records.

Field Extraction From PDFs, Scans, and Spreadsheets

Financial data extraction captures values from banking documents and converts them into usable data fields.

Data Validation Against Banking Records

Extracted data is checked against customer records, account data, policy rules, and expected formats.

Exception Routing for Human Review

Missing, low-confidence, or mismatched fields are routed to the right reviewer.

Many banking document types can benefit from this approach.

Banking Documents That Can Be Automated

Banking document automation can support files used across onboarding, lending, credit, compliance, and trade finance.

KYC and Customer Identity Documents

Identity proofs, address documents, ownership records, and business registrations can be processed faster.

Bank Statements and Transaction Records

Bank statements can be read for account details, balances, credits, debits, and transaction patterns.

Loan Applications and Facility Forms

Loan forms can be checked for borrower details, facility type, amount, tenure, and purpose.

Financial Statements and Audit Reports

Statements and audit reports can be processed for revenue, debt, assets, liabilities, and cash flow.

Tax Returns and Income Proofs

Tax files and income proofs help validate borrower income and business activity.

Collateral and Security Documents

Collateral documents support ownership, valuation, lien, and security checks.

Trade Finance Documents

Trade files such as invoices, letters of credit, and shipment documents can be checked for consistency.

Customer onboarding is one of the first areas where banks can reduce manual review effort.

How Automation Reduces Manual Work in Customer Onboarding

Automation reduces onboarding work by capturing customer data and flagging incomplete records early.

Faster Identity Document Capture

Identity data can be captured from uploaded documents without repeated manual entry.

Customer Data Extraction and Validation

Customer names, IDs, addresses, and entity details can be checked against banking records.

Missing Field Detection

Missing names, dates, document numbers, signatures, or declarations can be flagged.

KYC Checklist Completion Support

KYC checklists can be updated based on submitted and verified documents.

Review Routing for Exceptions

High-risk or incomplete cases can move to compliance teams for review.

The same logic applies to loan processing, where file preparation often consumes analyst time.

How Automation Reduces Manual Work in Loan Processing

Automation reduces loan processing work by preparing borrower files before underwriting begins.

Borrower File Preparation

Borrower documents are collected, sorted, classified, and made ready for review.

Application Data Capture

Application fields such as borrower name, loan amount, tenure, purpose, and entity type are extracted.

Income and Cash Flow Validation

Income proofs, bank statements, and financial documents can be compared for consistency.

Document Completeness Checks

The workflow can identify whether required loan, income, KYC, and collateral documents are present.

Underwriting Input Preparation

Validated borrower data can be prepared for underwriting and credit review.

Credit review needs a deeper layer of document and financial data processing.

How Automation Reduces Manual Work in Credit Review

Automation reduces credit review effort by extracting financial data and preparing structured inputs.

Financial Statement Data Extraction

Revenue, expenses, assets, liabilities, debt, equity, and cash flow values can be captured from statements.

Line Item Mapping for Credit Analysis

Borrower-specific line items can be mapped into standard credit categories.

Ratio-Ready Data Preparation

Structured financial data can support liquidity, leverage, profitability, and cash flow ratios.

Source Links for Extracted Values

Each extracted value can link back to the source statement, page, and line item.

Analyst Review for Exceptions

Analysts can focus on unclear fields, unusual values, and credit judgement instead of manual entry.

Compliance review also benefits when source evidence and review history are easier to manage.

How Automation Reduces Manual Work in Compliance Review

Automation reduces compliance work by checking completeness, rules, approvals, and evidence.

Document Completeness Checks

Required compliance documents can be checked against customer type, product, and policy rules.

Policy Rule Validation

Data fields can be checked against internal policies, thresholds, and required formats.

Sanctions and AML Data Review Support

Extracted customer and transaction data can support sanctions and AML review steps.

Approval Logs and Review History

Reviewer actions, approvals, rejections, and changes can be recorded.

Audit Evidence Preparation

Source files, extracted fields, and approval logs can be organized for audit review.

AI strengthens document automation by handling variation across file types and layouts.

How AI Supports Banking Financial Document Automation

AI supports banking document automation by reading varied documents, recognizing fields, and flagging issues.

AI for Document Classification

AI identifies document types before extraction begins.

AI for Table, Field, and Layout Recognition

AI reads tables, labels, rows, columns, and layout patterns across banking files.

AI for Data Validation

AI helps compare extracted values with expected formats, system records, and supporting documents.

AI for Anomaly and Discrepancy Detection

AI can flag mismatched values, missing fields, duplicate records, or unusual entries.

AI for Review Queue Prioritization

AI can help prioritize files that need faster review or carry higher risk.

Automation reduces manual effort, but some review tasks should remain with banking teams.

Manual Review Tasks That Should Still Stay With Banking Teams

Manual review should remain where judgement, policy interpretation, or risk assessment is required.

Low-Confidence Field Review

Fields with low confidence should be checked before use.

High-Risk Customer Cases

High-risk customers need human review for context and decision control.

Policy Exceptions

Policy exceptions should be reviewed by authorized banking teams.

Credit Judgement and Approval Decisions

Final credit decisions should remain with analysts and approvers.

Compliance Escalations

Compliance escalations need human ownership and documented resolution.

The goal is not to remove people from the process, but to improve review quality.

How Banking Document Automation Improves Review Quality

Banking document automation improves review quality by making data capture and validation more consistent.

Consistent Field Capture

Standard field capture reduces variation across teams and files.

Fewer Data Entry Errors

Reduced manual entry lowers the risk of typing mistakes and missed values.

Cleaner Borrower and Customer Records

Validated data supports more accurate borrower and customer records.

Faster Exception Identification

Exceptions can be identified earlier in the workflow.

Better Source-Level Traceability

Reviewers can trace values back to the original document.

Different banking teams benefit from this traceability in different ways.

How Document Automation Supports Banking Teams Across Workflows

Document automation supports banking teams by giving each function cleaner data and clearer review paths.

Operations Teams

Operations teams can process files faster and reduce repeated manual checks.

Credit Analysts

Credit analysts get structured borrower data for financial review and risk assessment.

Relationship Managers

Relationship managers can track missing documents and borrower file status more easily.

Compliance Officers

Compliance officers can review exceptions, policy checks, and high-risk files with better evidence.

Audit Teams

Audit teams can access source documents, review logs, and approval history.

Risk Review Teams

Risk teams can review borrower patterns, exceptions, and document-linked risk indicators.

Banks should also avoid common gaps that reduce the value of automation.

Common Gaps Banks Should Avoid in Document Automation

Banks should avoid automation setups that capture documents but fail to validate, route, or trace data properly.

Automating Intake Without Validation Rules

Document intake alone does not reduce review effort unless data is validated.

Using OCR Without Contextual Review

OCR can read text, but banking workflows need field meaning, document context, and source checks.

Ignoring Low-Confidence Fields

Low-confidence values should be routed for review instead of being used directly.

Separating Extracted Data From Banking Workflows

Extracted data should flow into onboarding, lending, credit, compliance, and audit processes.

Missing Source Links for Review and Audit

Every important value should connect back to the original file.

Before reducing manual review, banks should assess workflow readiness.

What Banks Should Check Before Reducing Manual Review Work

Banks should check document volume, required fields, systems, review rules, and security needs.

Document Volume and Format Variation

Banks should identify which documents create the most manual review effort.

Required Fields for Each Banking Workflow

Each workflow needs defined fields such as name, amount, account, income, tax, facility, collateral, and date.

Core Banking and LOS Integration Needs

Extracted data should connect with core banking, loan origination, document, and risk systems.

Review and Approval Rules

Banks should define who reviews exceptions, who approves records, and when escalation is needed.

Security, Access, and Retention Requirements

Access controls, retention rules, privacy requirements, and audit logs should be planned early.

Metrics can show whether manual review work is truly reducing.

Metrics That Show Manual Review Work Is Reducing

Banks can measure manual review reduction through speed, accuracy, touchpoints, and audit outcomes.

Document Processing Time

This measures how long files take to classify, extract, validate, and route.

Data Extraction Accuracy

This measures how often extracted fields match the source document.

Manual Touchpoints per File

This tracks how many human actions are required before a file moves forward.

Exception Rate

This shows how often documents need manual review because of missing or mismatched data.

Review Queue Ageing

Queue ageing shows how long files remain pending with reviewers.

Loan File Preparation Time

This measures the time needed to prepare borrower files for underwriting or credit review.

Audit Finding Reduction

Fewer audit findings can indicate better evidence, source links, and review control.

The final step is building a connected banking document automation workflow.

How to Build a Banking Document Automation Workflow

A banking document automation workflow should connect document intake, extraction, validation, review, and downstream systems.

Start With High-Volume Document Types

Start with documents that create the most manual review work, such as KYC files, bank statements, loan forms, and financial statements.

Standardize Banking Data Fields

Use standard fields for customer identity, account details, income, debt, collateral, document dates, and approval status.

Define Validation and Exception Rules

Set rules for missing fields, mismatches, low-confidence data, and policy exceptions.

Connect Extracted Data With Downstream Systems

Extracted and validated data should move into onboarding, LOS, core banking, credit, and compliance workflows.

Keep Human Review for Risk and Approval Steps

Human review should remain in place for exceptions, high-risk cases, and final approvals.

End Note: Banking Document Automation Reduces Manual Review Without Removing Human Control

Banking financial document automation reduces manual review work by turning files into structured data, validating fields, routing exceptions, and preserving source traceability. It helps onboarding, lending, credit, compliance, operations, and audit teams work with cleaner data and fewer repeated checks.

The strongest approach keeps human control where it matters most: risk review, policy exceptions, compliance escalations, and final banking decisions.

Sign in to leave a comment.