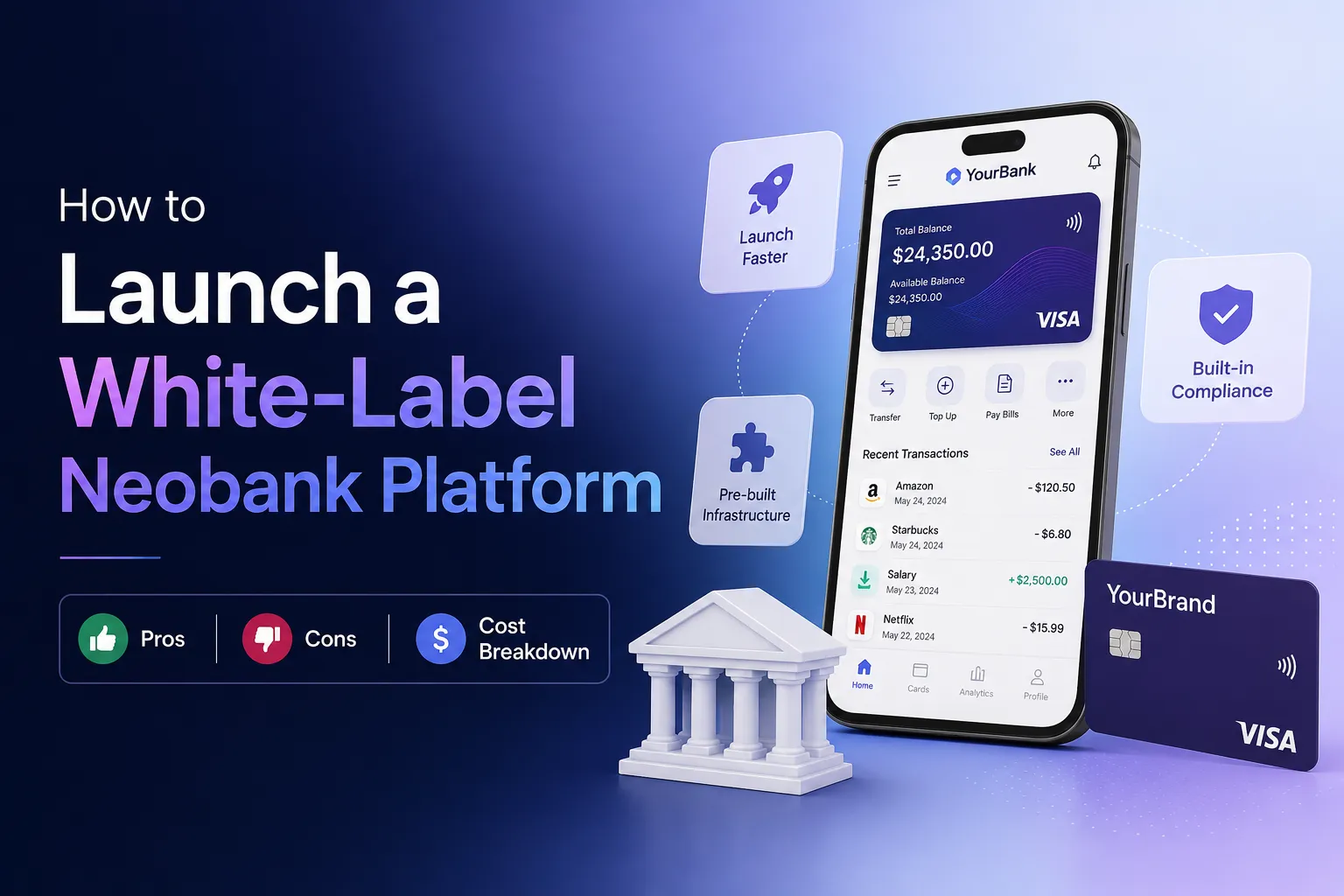

The digital banking revolution is no longer on the horizon — it is already here. Across the globe, consumers and businesses are ditching physical bank branches in favor of fast, mobile-first financial services. For entrepreneurs and enterprises looking to enter this space, the question is rarely whether to launch a digital banking product — it's how to do it quickly without burning through capital.

That's where white-label neobank platforms come in.

Rather than starting from zero, white-label solutions let businesses deploy a fully branded digital bank — complete with accounts, cards, payments, and compliance tools — in a fraction of the time and cost of custom neobank app development. Whether you're a fintech startup, a retail brand exploring embedded finance, or an enterprise looking to modernize financial services, a white-label platform could be your fastest path to market.

In this article, we break down exactly how to launch a white-label neobank, the real pros and cons, and what it will cost you in 2026.

What Is a White-Label Neobank Platform?

A white-label neobank is a pre-built digital banking infrastructure that businesses can rebrand and deploy as their own product. You don't build the core banking engine — you license it, customize it with your logo, colors, and user flows, and launch it under your brand name.

The underlying technology typically includes account management, KYC/AML verification, payment processing, debit card issuance, and a back-office dashboard. Your users experience it as your bank — the vendor is completely invisible.

This model is powered by Banking-as-a-Service (BaaS), which allows non-bank companies to offer regulated financial products by plugging into an existing licensed infrastructure. It's a key driver behind the explosive growth of fintech software development in recent years.

How to Launch: A Step-by-Step Overview

Step 1: Define your target audience and product scope. Are you building for consumers, SMEs, freelancers, or a specific niche like teens or migrants? Narrow your focus before choosing a platform. Your audience determines the features you need.

Step 2: Choose a white-label platform provider. Evaluate vendors on tech stack quality, supported payment rails (SEPA, SWIFT, ACH), compliance frameworks, API documentation, and post-launch support. Popular providers include Velmie, Crassula, and SDK.finance, among others. If you want a fully custom layer on top of a white-label base, a dedicated neobank app development partner like Nimble AppGenie can bridge the gap.

Step 3: Handle licensing and compliance. Depending on your target market, you will either operate under your own banking or e-money license, or under your provider's regulatory umbrella via BaaS. Compliance covers KYC (Know Your Customer), AML (Anti-Money Laundering), data protection laws, and regional mandates like PSD2 in Europe or RBI guidelines in India.

Step 4: Customize branding and UX. Apply your visual identity — logo, colors, typography — across mobile and web apps. Configure onboarding flows, notification templates, and admin dashboards to match your product experience.

Step 5: Integrate, test, and launch. Connect the platform to your existing systems via API, run thorough QA in a sandbox environment, submit apps to the App Store and Google Play, and do a soft launch with pilot users before going fully live.

Pros of Launching a White-Label Neobank

- Faster time to market. Building a neobank app from scratch can take 12 to 18 months. White-label platforms can get you live in as little as 6 to 12 weeks. That speed advantage allows you to acquire users, gather feedback, and iterate long before a custom-built competitor enters the market.

- Significantly lower upfront cost. Custom neobank app development typically runs between $100,000 and $500,000 or more. White-label platforms dramatically reduce that barrier, with total launch costs often falling in the $50,000 to $200,000 range including customization, compliance, and integration.

- Built-in compliance. Navigating financial regulations is one of the most complex aspects of neobank vs digital bank comparisons. White-label providers with existing licenses or BaaS frameworks handle the heavy regulatory lifting, reducing your legal risk from day one.

- Reduced technical risk. The core infrastructure has already been built, tested, and deployed at scale by the vendor. You inherit battle-tested systems rather than debugging a brand-new codebase.

- Focus on customer experience. Instead of worrying about ledger systems and payment rails, your team can focus entirely on product design, user acquisition, and what genuinely differentiates your offering.

Cons of Launching a White-Label Neobank

- Limited customization depth. White-label platforms come with a pre-defined feature set. While branding is fully flexible, deep customization of core logic — like proprietary credit models or unique transaction architectures — may require costly extensions or may simply not be possible.

- Vendor dependency. Your product's reliability is tied to your vendor's uptime, roadmap decisions, and pricing changes. If the vendor raises fees or discontinues a feature, you have limited control.

- Recurring platform costs. Unlike a custom build where you own the code outright, white-label platforms typically charge monthly licensing fees plus per-transaction costs, which can erode margins at scale.

- Differentiation challenges. If multiple neobanks use the same underlying platform with only cosmetic differences, standing out in a crowded market becomes harder. Long-term, a truly differentiated product may require migrating to a custom-built solution.

Cost Breakdown: What to Budget For

Here's a realistic picture of what launching a white-label neobank costs in 2026:

| Cost Category | Estimated Range |

|---|---|

| Platform License (upfront) | $15,000 – $50,000 |

| Branding & UI Customization | $10,000 – $30,000 |

| Compliance & Licensing | $15,000 – $50,000 |

| API Integration & Development | $5,000 – $40,000 |

| QA Testing & Launch | $5,000 – $30,000 |

| Total Estimated Range | $50,000 – $200,000 |

Beyond launch, expect ongoing monthly platform fees of $2,000 to $10,000 depending on your user base, plus per-transaction costs. Marketing, customer support, and operations are additional considerations.

Compared to a fully custom build — which can cost $500,000 to $2,000,000 and take well over a year — the white-label route offers a compelling ROI for early-stage products and market validation.

When to Choose White-Label vs. Custom Development

White-label is ideal when you are launching an MVP, entering a new market quickly, or validating product-market fit before committing to large engineering investment.

Custom neobank app development makes more sense when you need proprietary technology, have complex product requirements that no off-the-shelf platform supports, or are scaling to millions of users where vendor licensing costs exceed the cost of ownership of your own system.

Many successful neobanks begin with a white-label foundation and gradually migrate to custom fintech software development as they scale, generating revenue, and gain deeper clarity on their product direction.

Conclusion

Launching a white-label neobank platform is one of the smartest ways to enter the digital banking market in 2026 — fast, cost-effective, and backed by proven infrastructure. The tradeoffs around customization and vendor dependency are real, but manageable for most early-stage and mid-market products.

The key is choosing the right platform partner, planning your compliance strategy upfront, and investing in a customer experience that genuinely sets you apart from the competition.

If you're considering neobank app development — whether white-label or custom — Nimble AppGenie brings the fintech expertise, regulatory awareness, and development experience to help you build, launch, and scale your digital banking product the right way.

Frequently Asked Questions (FAQs)

Q1. How long does it take to launch a white-label neobank?

With the right platform and development partner, a white-label neobank can go live in 6 to 12 weeks. This timeline covers branding configuration, API integration, compliance setup, and app store submissions. Custom neobank app development, by comparison, typically takes 9 to 18 months.

Q2. Do I need a banking license to launch a white-label neobank?

Not always. Many white-label platforms operate under a Banking-as-a-Service model, which means you can launch under your provider's existing banking or e-money license. However, requirements vary significantly by country, so it's important to consult a fintech regulatory expert for your specific target market before launch.

Q3. What is the difference between a neobank and a digital bank, and does it affect the white-label approach?

The neobank vs digital banking distinction comes down to infrastructure. Neobanks operate exclusively online with no physical branches, typically relying on third-party licensed partners for core banking. Digital banks are often extensions of traditional banks that have built their own digital front-ends on existing regulated infrastructure. For white-label launches, the neobank model is more common, since it doesn't require owning a full banking charter and leverages BaaS providers to handle the regulatory backend.

Sign in to leave a comment.