The sector is valued at approximately USD 14 billion in 2024, driven by rapid growth in e‑commerce, significant infrastructure investments, and rising demand for efficient supply chain solutions across industries. Key regional hubs such as South Africa, Nigeria, and Kenya are leading this evolution due to enhanced logistics infrastructure and strategic positioning within African trade corridors. The Africa contract logistics market analysis demonstrates how contract logistics is becoming a strategic enabler for businesses seeking to optimize distribution networks, reduce delivery times, and improve service quality amidst rising consumer expectations.

Contract Logistics Market Segmentation and Service Breakdown

The Africa contract logistics market is segmented by service and end‑user industry:

Service Segments: Transportation, Warehousing, Distribution, Aftermarket Logistics, and Other Value‑Added Services. Transportation remains the largest segment due to continued reliance on multimodal freight movement, while warehousing and distribution are gaining prominence with inventory management and last‑mile delivery demand.

End‑User Industries: Retail & E‑commerce, Automotive, Consumer Goods, Pharmaceuticals & Healthcare, and Manufacturing. Retail & e‑commerce is the leading end‑user category, driven by exponential growth in online shopping and the corresponding need for robust delivery networks.

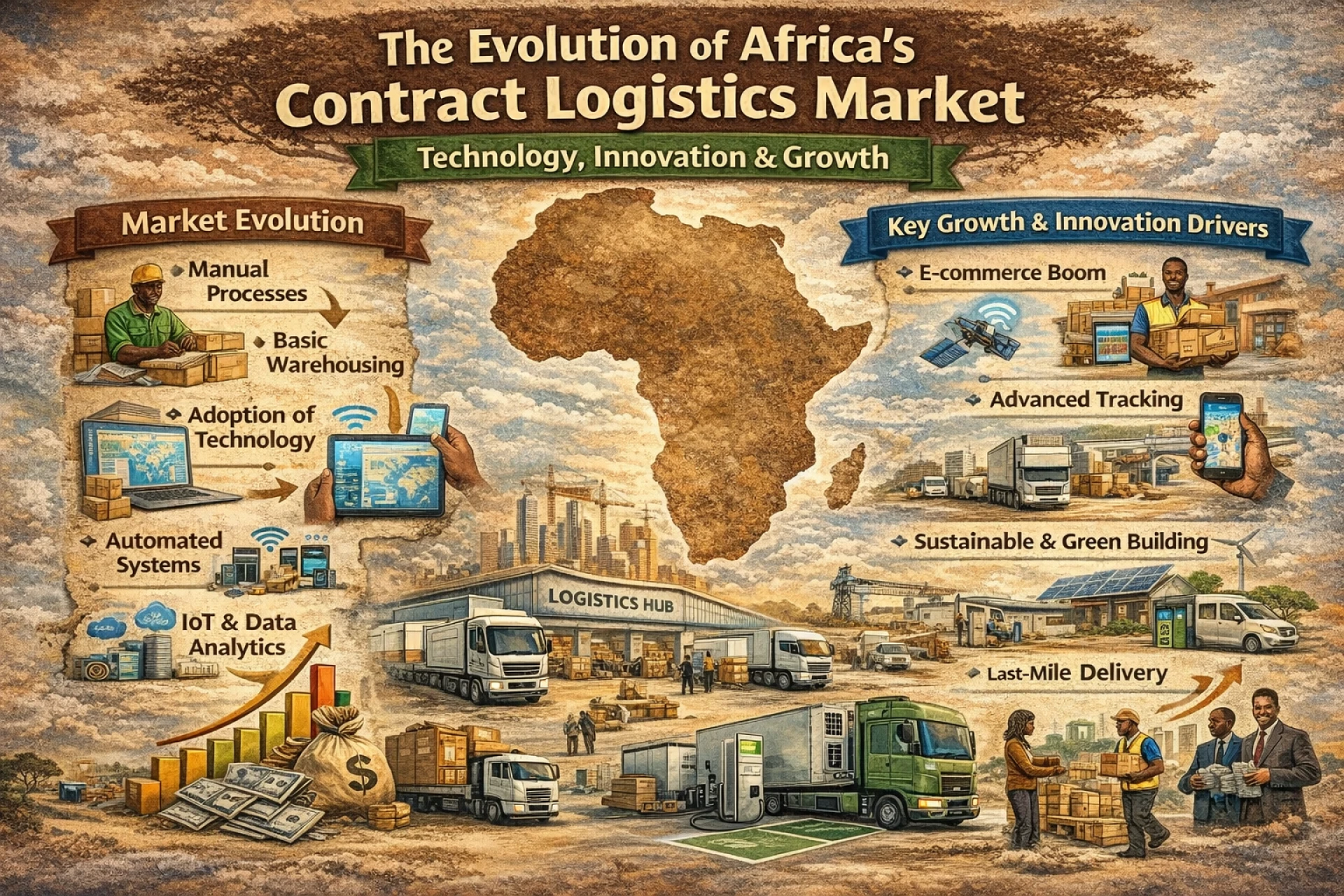

Key Growth Drivers and Market Trends in Africa’s Contract Logistics

The Africa contract logistics market growth is supported by several key factors:

E‑Commerce Expansion: Rapid rise in online retail transactions is pushing logistics providers to scale operations, enhance order fulfillment systems, and deploy advanced tracking technologies.

Infrastructure Investment: Government initiatives and public‑private partnerships strengthen road, rail, and port networks, improving logistics flow across borders and boosting regional trade efficiency.

Manufacturing & Retail Sector Expansion: As industrial and retail activities rise, there is greater demand for integrated logistics solutions to support inbound and outbound supply chains.

These factors contribute to evolving Africa contract logistics market trends, including the adoption of automation, real‑time visibility tools, and flexible warehouse solutions aimed at improving operational agility.

Competitive Landscape in Africa’s Contract Logistics Market

The Africa contract logistics market is highly competitive, with five key players leading the way:

DHL Supply Chain: A global logistics giant offering integrated supply chain services, with strong operations across Africa, focusing on warehousing, distribution, and e‑commerce fulfillment.

Kuehne + Nagel: Known for its advanced digital solutions and strong presence in key African markets, Kuehne + Nagel provides tailored logistics services with a focus on e‑commerce fulfillment and inventory management.

DB Schenker: Offers multimodal logistics solutions with a focus on enhancing supply chain efficiency through technology and seamless integration of freight and contract logistics services.

CEVA Logistics: Specializes in providing tailored contract logistics solutions, focusing on inventory management, distribution, and supply chain optimization for various sectors, including retail and e‑commerce.

Bolloré Logistics: With its robust regional infrastructure, Bolloré Logistics provides end‑to‑end logistics services across Africa, including warehousing, distribution, and customs clearance, especially in transport and industrial sectors.

These top players dominate the market by leveraging their global reach, technology, and strong regional networks to offer efficient, scalable logistics solutions across Africa.

Strategic Challenges in the Africa Contract Logistics Ecosystem

The Africa contract logistics market challenges include:

Infrastructure Gaps: Uneven development of multimodal logistics networks, particularly in landlocked regions, impedes seamless freight movement.

Regulatory Fragmentation: Variations in customs, trade policies, and cross‑border procedures increase complexity and costs for logistics operators.

Skill and Technology Shortfalls: Limited availability of a skilled workforce and delayed digital adoption slow the uptake of advanced logistics practices.

Despite these hurdles, ongoing policy reforms and regional integration initiatives are gradually improving the business environment for contract logistics service providers.

Market Forecast and Growth Projections in Africa

Industry projections indicate that the Africa contract logistics sector will continue to expand steadily over the next decade, bolstered by sustained e‑commerce growth, enhanced regional trade agreements, and the adoption of advanced logistics technologies. According to the Africa contract logistics market forecast, the contract logistics segment generated approximately USD 14.28 billion in revenue in 2024 and is expected to grow at a compound annual growth rate (CAGR) of around 5.3% from 2025 to 2030, reflecting ongoing investments in supply chain optimization and warehousing infrastructure development.

Additionally, broader logistics data show that the overall Africa logistics market, a larger ecosystem that includes contract logistics is projected to grow from around USD 471.5 billion in 2024 to an estimated USD 680.3 billion by 2030, at a CAGR of about 6.3%, underscoring the rising demand for efficient logistics and automated solutions across the region.

Conclusion: Africa Contract Logistics Market Outlook

In conclusion, the Africa contract logistics market outlook is optimistic, with strong momentum driven by e‑commerce penetration, infrastructure upgrades, and rising demand for integrated supply chain services. As digital innovation and regional trade agreements continue to shape market dynamics, contract logistics will play a central role in enhancing efficiency and competitiveness across Africa’s burgeoning logistics landscape.

Read In‑Depth

For detailed insights, segment‑level data, competitive analysis, and future projections in the Africa contract logistics market.

Sign in to leave a comment.