What is ACH Payment? A Complete Guide for 2026

In a digital economy where speed, security, and cost-efficiency matter more than ever, businesses and consumers alike are turning to modern payment systems that go beyond traditional cards and cash. One such essential system powering countless transactions every day is ACH payment processing — a backbone of electronic finance, particularly in the United States. In this guide, we’ll explore what ACH is, how it works, and why platforms that combine ACH with card issuing and other services are invaluable in 2026.

What Does ACH Stand For?

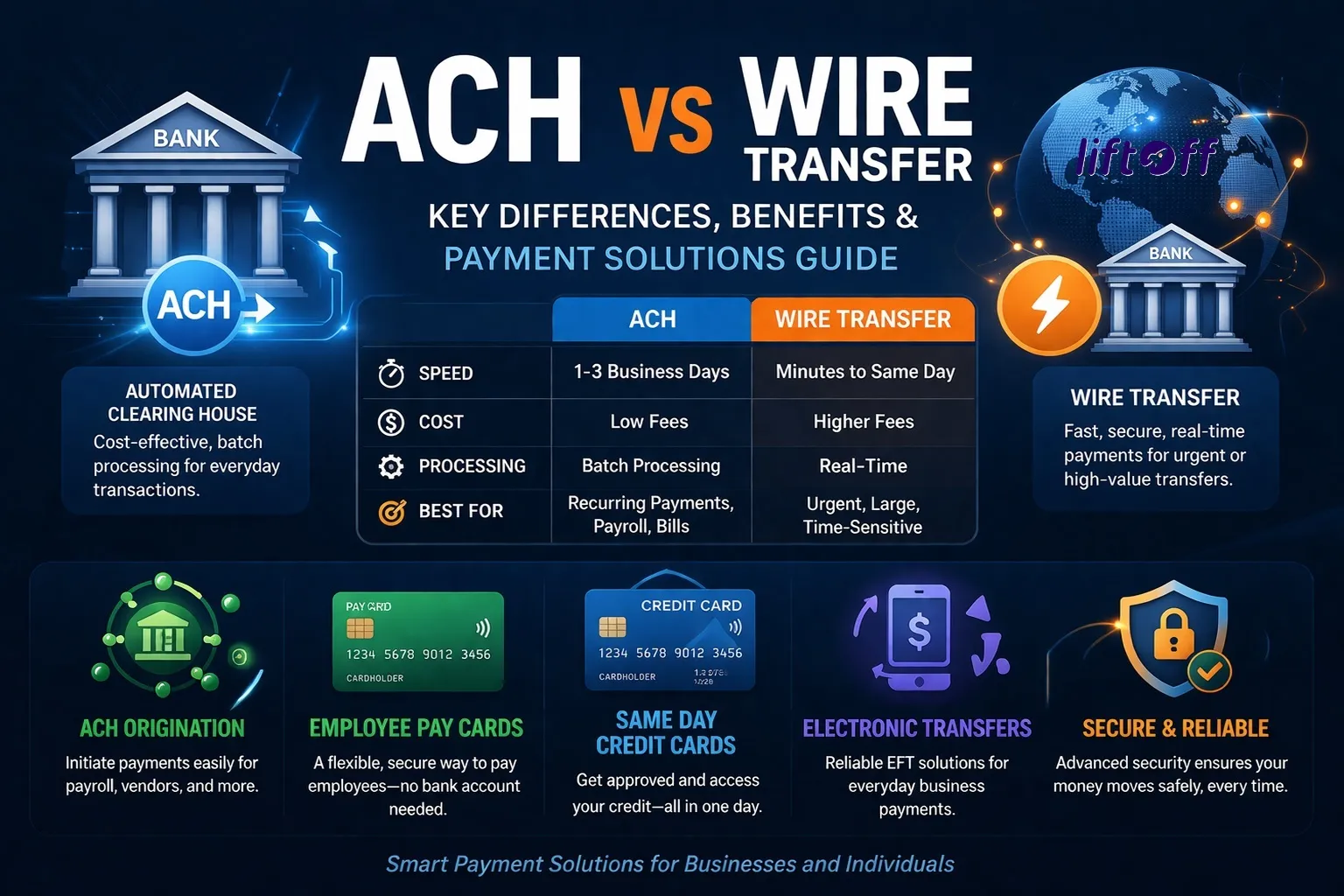

ACH stands for Automated Clearing House, a nationwide electronic network used to transfer funds between bank accounts. Unlike debit or credit card payments, ACH transactions are typically batch-processed, which means they are grouped together and settled at designated times throughout the day. This system is overseen by the National Automated Clearing House Association (NACHA), ensuring secure, reliable, and standardized transfers that businesses and consumers’ trust.

ACH isn’t new — it’s been around for decades — but it’s evolved significantly, powering direct deposits, automated bill pay, subscription payments, vendor payouts, and much more.

How ACH Payment Processing Works

ACH processing moves money between bank accounts without physical checks or card swipes. Here’s a simplified breakdown:

- Authorization: The payer first authorizes the payment — for example, setting up a recurring bill or direct deposit.

- Submission: The transaction request is sent to the Originating Depository Financial Institution (ODFI), usually the sender’s bank.

- Clearing: The ODFI forwards the information to the ACH network, which links it to the Receiving Depository Financial Institution (RDFI) — the recipient’s bank.

- Settlement: The money is debited from the payer’s account and credited to the recipient’s account. Standard ACH settlement usually takes 1–3 business days, but same-day ACH options are becoming more common.

This process makes ACH highly reliable and secure, allowing both businesses and consumers to send and receive funds without the friction of physical checks or the expense of wire transfers.

Benefits of ACH in 2026

1. Lower Costs

ACH transactions are typically much cheaper than credit card processing or wire transfers. This makes ACH ideal for businesses handling large volumes of payments or high-ticket transactions.

2. Recurring Payments

Because ACH supports automatic debits, it’s perfect for subscription-based businesses, memberships, or any service requiring regular billing.

3. Enhanced Cash Flow

With functions like direct deposit for payroll or automated vendor payouts, companies can streamline cash flow and reduce administrative burden.

4. Security

ACH transfers follow strict NACHA guidelines and banking standards, including encryption and fraud monitoring, making them a secure choice for both small and large enterprises.

What Is ACH Processing on Modern Platforms?

In 2026, simply accepting payments isn’t enough — businesses need integrated systems that handle multiple payment types efficiently. That’s where platforms like Liftoff Platform come in. They combine ACH with other payment rails, including card issuing platforms, RTP (Real-Time Payments), and same-day settlement options, into a single API and dashboard.

Card Issuing Platform + ACH

A card issuing platform allows businesses to create and manage debit or virtual cards for users, employees, or customers. Combining this with ACH processing means you can offer both bank transfers and card payments, covering a wide range of payment needs from one backend system.

For example, a business might:

- Pay vendors via ACH (lower cost, bank-to-bank transfer)

- Issue virtual cards to remote workers for expense management

- Accept customer payments through ACH or card checkout

Platforms like Liftoff simplify this entire ecosystem, giving you one interface to manage bank transfers, cards, recurring billing, and fraud protection.

Use Cases: Who Uses ACH Payments?

In 2026, ACH payment processing is essential across industries:

- Payroll and Direct Deposit: Employers use ACH to distribute wages directly to employees’ bank accounts, avoiding paper checks.

- Recurring Billing: Subscription businesses, membership services, and SaaS companies often rely on ACH to automate monthly payments.

- Vendor Payments: Businesses can pay suppliers or service partners efficiently, reducing manual invoicing and payment delays.

- Consumer Payments: Utilities, insurance premiums, loan repayments, and rent collection can all be handled through ACH debits or credits.

ACH in the Modern Payment Stack

By 2026, payments are expected to be smooth, integrated, and adaptable:

- Customers demand multiple payment options — bank transfers, card payments, wallets, and APIs that tie everything together.

- Businesses want control and transparency — consolidated dashboards, fraud prevention, and reconciliation data.

- Developers need simplicity — a single API to manage transfers, verify accounts, and handle settlement with minimal backend complexity.

Platforms like Liftoff serve this ecosystem by offering ACH processing, card issuing, tokenization, bank account verification, and fraud prevention under one roof, enabling both B2B and B2C transactions with a unified approach.

Final Thoughts: What Is ACH Payment in 2026?

In simple terms, an ACH payment is an electronic bank transfer that moves money between accounts through a structured network. It stands out because of its low cost, security, and flexibility for recurring and high-volume use cases.

As payment technology evolves, ACH remains a foundational component — but modern platforms are elevating it with features like same-day settlement, API-driven workflows, and integrated card issuing. This makes ACH not just a way to move money, but a strategic advantage for businesses that want to optimize collection, reduce friction, and deliver better user experiences.

Whether you’re a small business owner looking to streamline payments or an enterprise seeking a unified payment solution, understanding and leveraging ACH payment processing in 2026 is essential to staying competitive.

Sign in to leave a comment.