Finance teams process large volumes of financial statements each week, yet most credit decisions still depend on slow manual preparation. Raw files arrive in mixed formats, line items vary across issuers, and analysts spend hours aligning labels before any ratio can be trusted. The pain shows up as review delays, repeated corrections, and inconsistent credit memos across teams. The problem grows with portfolio size and reporting cycles. This article explains what financial spreading means in credit analysis, how raw statements become structured records, where accuracy breaks down, and how automated and AI-led workflows change credit operations. It also covers data quality controls, governance needs, integration points, adoption barriers, and future directions.

What Financial Spreading Means in Credit Analysis

Financial spreading refers to the structured conversion of raw financial statements into standardized records that credit teams can compare, validate, and use for risk assessment. The focus remains on preparing reliable data rather than forming credit opinions.

Definition and scope of financial spreading

Financial spreading converts income statements, balance sheets, and cash flow statements into uniform formats with consistent labels and fields. The scope includes capture, normalization, mapping, and validation so analysts receive records ready for ratio calculation and trend review. This process builds on disciplined financial statement spreading practices used across commercial lending and risk teams.

How spreading differs from financial analysis and underwriting

Spreading prepares the data. Financial analysis interprets performance and position. Underwriting applies policy rules to approve or decline credit exposure. Each step depends on the accuracy of the previous one.

Where spreading fits in the credit workflow

Spreading begins after document intake and ends before ratio calculation and credit memo preparation. Errors at this stage pass forward into later decisions and increase review cycles.

Clear definition of the process sets the stage for understanding the source material used for spreading.

Source Documents Used for Financial Spreading

Credit teams rely on multiple document types that differ in structure, period coverage, and reliability. Each source carries distinct preparation needs.

Income statements and cash flow statements

These statements provide performance and liquidity signals. Revenue, operating costs, and cash movements must be aligned across periods to support consistent trend review.

Balance sheets and supporting schedules

Balance sheets show capital structure and asset quality. Supporting schedules add detail on receivables, payables, inventory, and debt terms that affect credit ratios.

Bank statements and tax records

Bank data offers transaction-level evidence of cash movement. Tax records provide verified totals that often differ from management reports. Both require careful alignment during financial data extraction to prevent mismatches later in credit analysis.

Once sources are defined, teams move to structuring the data for analysis and review.

From Raw Statements to Structured Records

Raw files arrive in many formats and must be converted into standard financial records before any credit work can begin.

Data capture from scanned and digital files

Statements arrive as PDFs, images, or spreadsheets. Capture processes convert them into machine-readable fields so analysts do not need to rekey values manually.

Normalization of line items across formats

The same financial concept appears under different labels across issuers. Normalization aligns these variations into standard categories used by lending teams.

Mapping to standard financial templates

Mapped values populate standard templates used in financial statement spreading so ratios, peer comparisons, and trends remain consistent across borrowers and periods.

After structuring, accuracy risks become visible and must be addressed early.

Accuracy Challenges in Financial Spreading

Errors at this stage affect every downstream credit decision and review outcome.

Inconsistent labels and accounting formats

Different issuers use varied naming conventions and accounting treatments. Without alignment, line items may be placed in the wrong category.

Missing fields and partial disclosures

Statements may omit details or present aggregated values. Gaps require flags and follow ups before credit review.

Multi-period alignment errors

Periods across statements may not match. Misalignment distorts trends and coverage ratios.

These risks explain why manual methods persist, even though they limit scale.

Manual Spreading Methods and Their Limits

Manual approaches remain common due to familiarity and perceived control.

Spreadsheet-based workflows in lending teams

Analysts rekey data into spreadsheets and adjust formulas for each borrower. This creates inconsistency across teams.

Time and error exposure in manual entry

Repeated entry increases fatigue and typo rates. Verification consumes senior analyst time.

Review cycles and rework loops

Supervisors review entries, send corrections back, and repeat cycles. Turnaround slows during peak periods.

Automation addresses some of these limits but older systems still fall short.

Automated Spreading Approaches in Lending Operations

Automation handles capture and mapping through rules and pattern detection.

Rule-based extraction and mapping

Rules map known labels to standard fields. This works for stable formats but breaks when layouts change.

OCR with layout detection

OCR reads text and table structure from documents. It reduces manual entry yet misreads merged cells and footnotes in varied layouts.

Limits of template-driven systems

Template systems fail when issuers change formats or combine statements in one file, leading to frequent exceptions.

AI-led workflows address these limits through context and learning.

AI-Led Spreading Workflows

AI-led workflows focus on meaning rather than position.

NLP for context-aware line item identification

NLP reads surrounding text and table context to classify items even when labels vary across issuers.

Probabilistic models for field validation

Probabilistic models assign confidence scores to extracted values and flag anomalies for review.

Learning loops from reviewer feedback

Reviewer corrections feed learning loops so capture accuracy improves over time and review effort drops.

These workflows produce outputs that analysts can use directly for credit work.

Credit-Ready Outputs from Spreading

Prepared outputs shape underwriting speed and consistency.

Standardized financial statements for underwriting

Uniform statements allow consistent comparisons across borrowers and periods.

Ratio sets used in credit memos

Prepared ratios flow into credit memos without repeated recalculation.

Trend views across periods

Aligned periods allow trend views that reveal growth, margin shifts, and liquidity changes.

Quality controls keep these outputs dependable across cases.

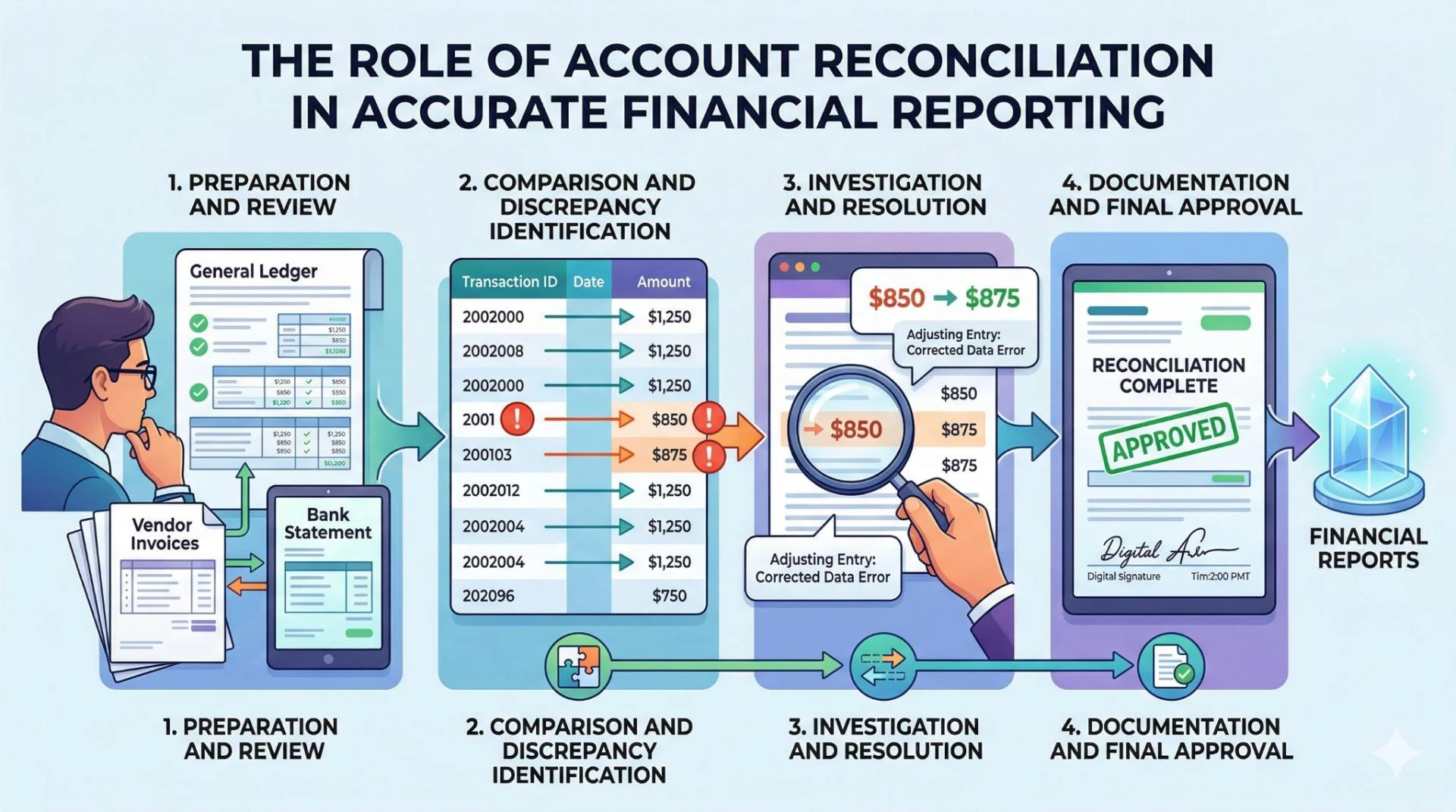

Data Quality Controls for Credit Decisions

Controls reduce risk in credit outcomes and audit exposure.

Field-level checks and variance flags

Checks flag outliers such as negative revenue or sudden jumps in expense ratios.

Cross-statement reconciliation

Totals reconcile across income statements, balance sheets, and cash flow records to confirm consistency.

Exception handling and audit trails

Exceptions carry notes and change history for audit review and internal control checks.

With quality controls in place, risk signals become easier to spot early.

Risk Signals Uncovered Through Spreading

Structured data reveals patterns before underwriting begins.

Early warning signs in cash flow patterns

Irregular inflows and rising outflows point to liquidity stress.

Leverage and coverage shifts across periods

Debt ratios and coverage changes show growing exposure risk.

Volatility indicators in operating metrics

Volatile margins signal unstable operations that warrant closer review.

As portfolios grow, scale places new demands on spreading workflows.

Spreading at Scale for Commercial Lending

Scale changes both process design and system needs.

Multi-entity and multi-currency handling

Large borrowers submit consolidated and local statements. Currency alignment is needed for valid ratio comparison.

Portfolio-level consistency checks

Consistency checks keep definitions uniform across thousands of records.

Throughput needs during peak cycles

Peak cycles require predictable turnaround to avoid backlog and approval delays.

Governance frameworks support trust in scaled operations.

Governance and Compliance in Spreading Programs

Governance aligns processes with audit and policy needs.

Evidence retention for audits

Source files and field history remain available for audit review.

Access control and data privacy

Controls restrict who can view and edit sensitive financial data.

Review accountability and sign-off

Named reviewers approve final records to maintain accountability.

To justify process change, teams track measurable impact.

Measuring Business Impact of Financial Spreading

Impact links process change to operating outcomes.

Cycle time from intake to credit memo

Shorter cycles reduce approval delays and improve borrower response times.

Rework rates and correction volume

Lower rework shows better capture quality and fewer review loops.

Analyst capacity and case throughput

Higher throughput shows analysts spend time on judgment rather than entry.

These outcomes depend on system integration across credit workflows.

Integration with Credit Systems

Spreading outputs must move into core credit systems without friction.

Feeds into loan origination systems

Standard records feed directly into origination workflows.

Links with risk rating workflows

Ratios move into rating logic without manual copying.

Data exchange with reporting stacks

Prepared data flows into reporting stacks for portfolio views and trend review.

Even with integration, adoption barriers can slow progress.

Adoption Barriers in Enterprise Finance Teams

Operational change requires people and data alignment.

Change management for analysts

Analysts need training and trust in new workflows to reduce fallback to spreadsheets.

Data ownership across departments

Finance, risk, and IT often hold different views of financial data ownership.

Standard definitions across regions

Regional teams use varied definitions that require alignment for portfolio reporting.

Several gaps remain across many programs and deserve attention.

Gaps in Current Coverage

These gaps create hidden rework and audit risk.

Handling restated financials without rework sprawl

Restated statements often trigger full re-entry rather than selective updates.

Traceability from credit decision back to source fields

Credit memos rarely link directly to source fields, limiting audit traceability.

Consistent treatment of non-standard disclosures

Non-standard notes often remain outside structured records and affect ratio accuracy.

Future directions point to closer links between data preparation and risk work.

Future Directions in Financial Spreading

Trends point to deeper context and learning across portfolios.

Context-aware mapping across industries

Industry patterns guide field mapping and reduce manual review for sector-specific statements.

Continuous learning from portfolio outcomes

Portfolio outcomes inform capture confidence and review focus over time.

Convergence of spreading with risk scoring

Prepared data feeds risk scoring directly, linking preparation with decision logic.

Teams evaluating structured capture and validation at scale can review Financial Spreading Software options that support consistent record preparation and integration across enterprise credit workflows.

Sign in to leave a comment.