Finance teams process thousands of transactions across bank accounts, customer invoices, supplier payments, payroll records, and journal entries every month. As transaction volumes grow, even small errors can create reporting issues, unsupported balances, and audit concerns. A missing entry, duplicate posting, or timing difference can leave account balances out of sync with supporting records.

The challenge becomes more visible during month-end close, when finance teams need confidence that reported balances are accurate. This is where account reconciliation becomes a critical finance process. In this guide, we explain what account reconciliation means, the types of accounts commonly reconciled, the information required before starting, and a practical step-by-step account reconciliation example that shows how the process works in practice.

Why Account Reconciliation Matters in Finance Operations

Account reconciliation helps finance teams verify that reported balances are accurate and supported by evidence.

Growth in transactions across banking, payable, receivable, payroll, and accounting systems

Modern finance operations rely on multiple systems that process payments, invoices, payroll transactions, tax entries, and journal postings. More systems create more opportunities for discrepancies.

Why unreconciled balances create reporting and compliance risks

When balances remain unreconciled, financial statements may contain inaccurate figures. This can affect reporting, compliance reviews, and management decisions.

Impact of reconciliation accuracy on financial statements and audits

Accurate reconciliation reduces reporting errors, improves confidence in financial statements, and creates stronger audit support.

What Account Reconciliation Means

Before reviewing the process, it helps to understand the purpose of reconciliation.

Definition of account reconciliation in accounting and finance

Account Reconciliation is the process of comparing account balances against supporting records to confirm accuracy and completeness.

Purpose of comparing balances against supporting records

The objective is to identify differences, investigate their cause, and ensure balances are supported by valid transactions and documentation.

Why reconciliation confirms the accuracy of financial data

A reconciled account provides evidence that reported balances reflect actual financial activity.

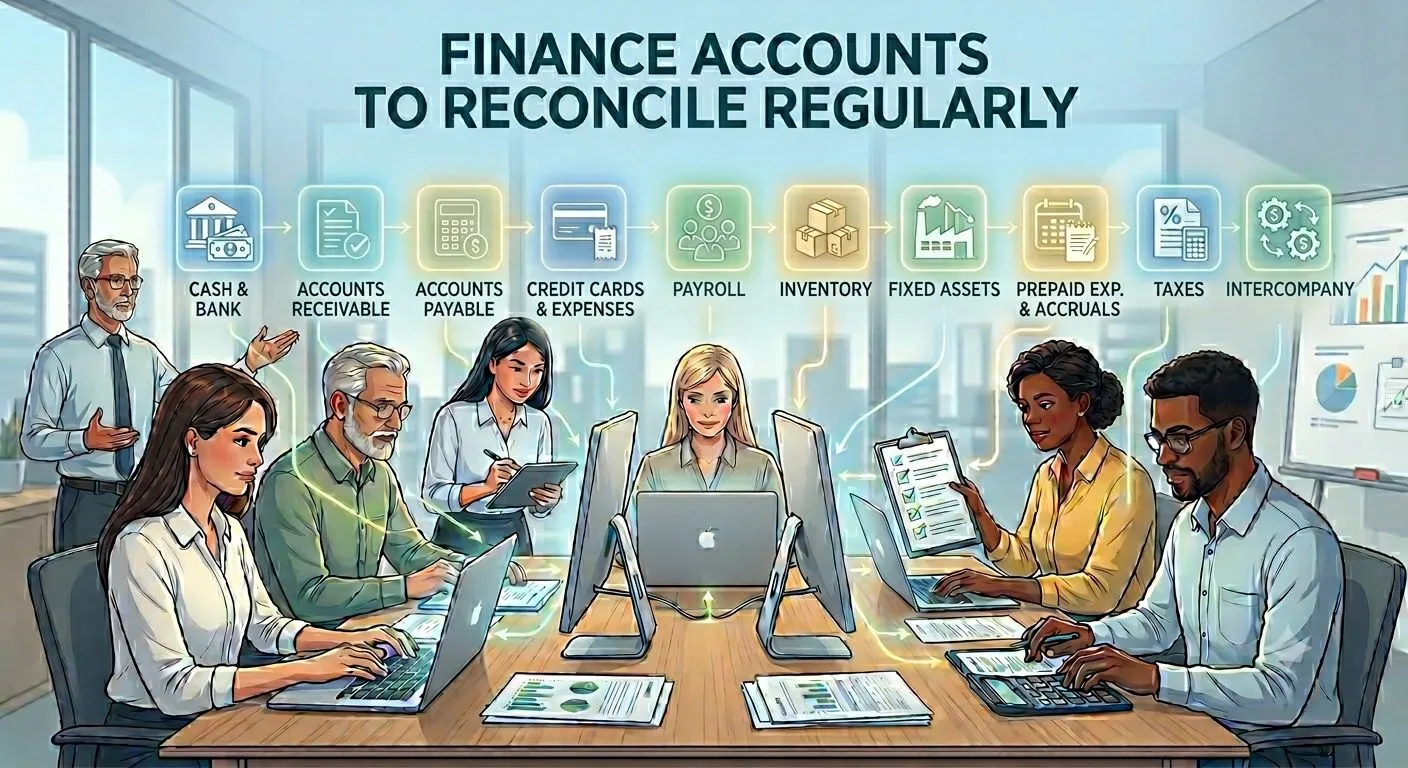

Types of Accounts Commonly Reconciled

Different accounts require reconciliation throughout the reporting cycle.

Cash and bank accounts

Cash balances are compared against bank statements and treasury records.

Accounts receivable balances

Customer balances are validated against invoices, payments, and credit notes.

Accounts payable balances

Supplier balances are reviewed against invoices, payments, and outstanding obligations.

Payroll and employee-related accounts

Payroll liabilities, taxes, and employee-related balances require regular validation.

Inventory, accrual, and prepaid expense accounts

These accounts often contain adjustments that require supporting schedules and documentation.

Intercompany accounts and clearing accounts

Organizations with multiple entities reconcile balances between related companies and temporary clearing accounts.

When Finance Teams Should Reconcile Accounts

The timing of reconciliation depends on transaction volume and account risk.

Daily reconciliation for high-volume transactions

Cash-intensive accounts may require daily monitoring.

Weekly reconciliation for operational accounts

Operational accounts often benefit from weekly review cycles.

Month-end reconciliation before financial close

Most account reconciliations are completed before month-end reporting.

Quarter-end and year-end reconciliation requirements

Additional review is typically performed during major reporting periods.

Information Needed Before Starting Account Reconciliation

Preparation is one of the most important parts of the process.

General ledger balances

The general ledger provides the official account balance being reviewed.

Supporting schedules and account reports

Schedules provide detailed activity supporting the balance.

Source documents and transaction records

Invoices, receipts, statements, contracts, and reports help validate transactions.

Prior-period reconciliation records

Previous reconciliations provide context for recurring items.

Approval and adjustment documentation

Any prior corrections should be properly approved and documented.

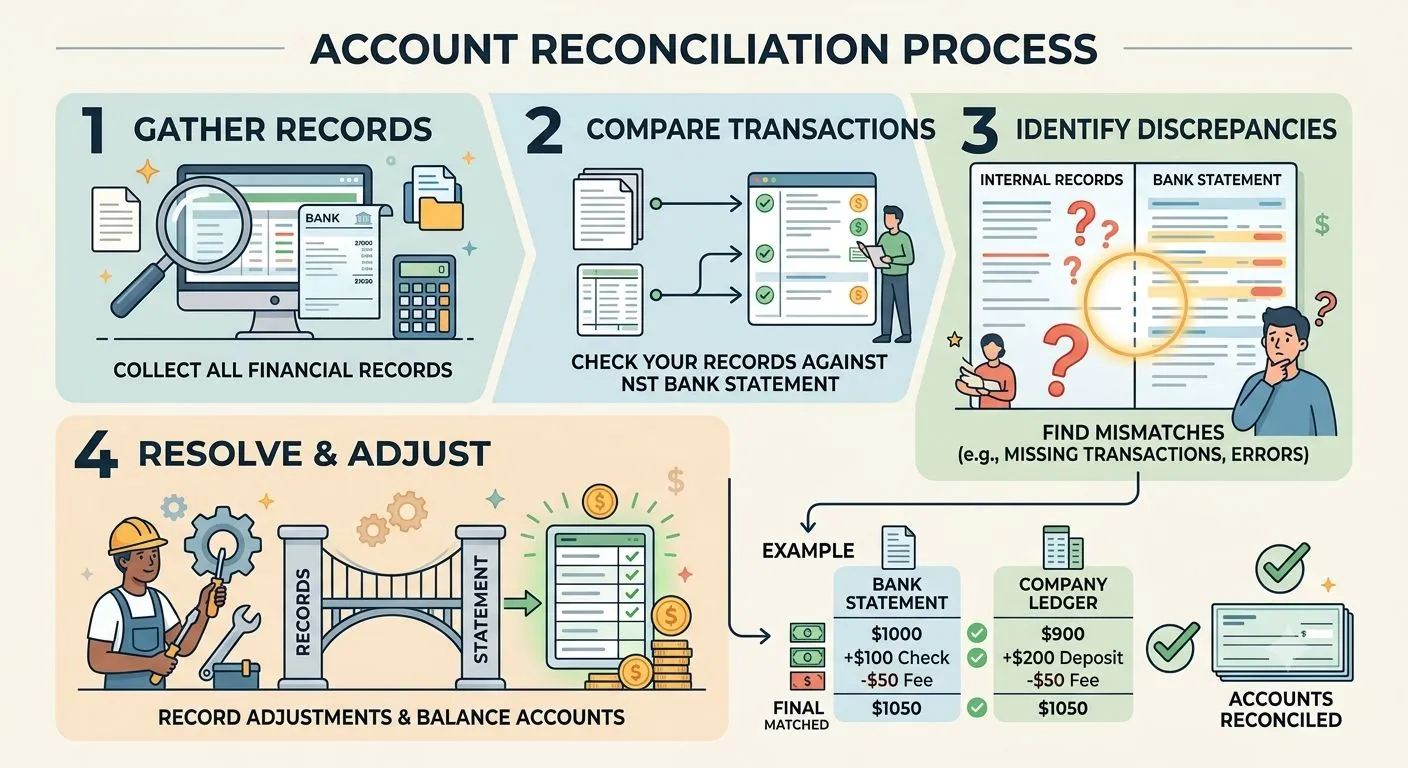

Step 1: Identify the Account and Reporting Period

Every reconciliation begins with defining the scope.

Confirm account ownership and responsibility

Assign responsibility for reviewing and approving the account.

Define the reconciliation period

Determine whether the reconciliation covers a month, quarter, or year.

Verify opening and closing balances

Confirm that balances agree with the reporting period being reviewed.

Once the account is defined, supporting records can be collected.

Step 2: Gather Supporting Records

Collect all documents needed to support the account balance.

Collect statements, schedules, and transaction reports

Gather relevant reports from finance systems and external sources.

Review source documents supporting account activity

Validate invoices, receipts, contracts, and statements.

Confirm data completeness before analysis

Missing records can lead to incorrect conclusions during reconciliation.

With supporting data available, balances can now be compared.

Step 3: Compare Account Balances Against Supporting Records

This stage identifies whether differences exist.

Match balances to schedules and reports

Compare ledger balances with supporting schedules and source records.

Identify differences between records

Any mismatch should be documented for review.

Separate explained and unexplained variances

Known timing differences should be separated from unexplained discrepancies.

After differences are identified, investigation begins.

Step 4: Investigate Reconciliation Differences

Understanding why a discrepancy exists is the core of reconciliation.

Review missing transactions

Determine whether transactions were omitted from records.

Check duplicate entries and duplicate postings

Duplicate activity can overstate balances.

Validate account classifications and coding

Incorrect coding can place transactions in the wrong account.

Review timing-related differences

Settlement delays and reporting cut-offs often create temporary differences.

After investigation, findings must be documented.

Step 5: Document and Resolve Exceptions

Every discrepancy should have a documented explanation.

Record findings for each discrepancy

Maintain records explaining each identified difference.

Obtain supporting evidence for corrections

Supporting documents should validate any proposed correction.

Escalate unresolved items when necessary

Material differences may require management review.

Once exceptions are approved, adjustments can be posted.

Step 6: Post Approved Adjustments

Corrections should follow established approval procedures.

Create correcting journal entries

Adjust balances where errors have been confirmed.

Validate approval requirements

Ensure corrections meet internal approval policies.

Update supporting schedules after adjustments

Schedules should reflect the revised balance.

The final step confirms that reconciliation objectives have been achieved.

Step 7: Verify Final Reconciled Balance

The account should now agree with supporting records.

Confirm account balance matches supporting records

The reconciled balance should align with validated documentation.

Review outstanding items remaining open

Any unresolved items should be documented and tracked.

Validate reconciliation completeness

Confirm that all reconciliation procedures have been completed.

Step-by-Step Account Reconciliation Example

The following example demonstrates the process in practice.

Example scenario and account balance

Assume a cash account shows a general ledger balance of $100,000 at month-end. Supporting bank records show a balance of $97,500.

Identification of reconciliation differences

The review identifies:

- Deposit in transit: $3,000

- Outstanding payment: $500

Investigation and adjustment process

The deposit was recorded internally but had not yet appeared in the bank statement. The payment had been issued but not yet cleared.

Both items were supported by documentation, so no correcting entry was required.

Final reconciled balance calculation

Bank balance: $97,500

Plus deposit in transit: $3,000

Less outstanding payment: $500

Adjusted balance: $100,000

The adjusted balance matches the ledger balance, meaning the account is reconciled.

A useful way to validate that all reconciliation steps have been completed is to follow an Account Reconciliation Review Checklist before final approval.

Common Reconciliation Differences Explained

Reconciliation differences usually fall into a few common categories.

Missing transactions

A transaction may appear in one record but not another because it was not posted, imported, or recorded on time.

Duplicate transactions

Duplicate entries can overstate balances and create false account activity.

Timing differences

Timing differences occur when a transaction is recorded in one period or system before it appears in another.

Incorrect account postings

Transactions may be posted to the wrong account, cost center, or entity.

Unsupported adjustments

Adjustments without approval or evidence should be reviewed before the account is signed off.

How to Handle Outstanding Reconciliation Items

Outstanding items should be tracked until they are resolved.

Items awaiting supporting documentation

Assign ownership and due dates for missing invoices, statements, approvals, or receipts.

Transactions pending settlement

Keep settlement-related items open until bank, vendor, customer, or payroll records confirm completion.

Open exceptions carried into the next period

Carry-forward items should include explanations, owners, and expected resolution dates.

Escalation procedures for aging discrepancies

Older or high-value items should be escalated for management review.

Reconciliation Controls That Improve Accuracy

Controls help finance teams make reconciliation consistent.

Segregation of duties

The person preparing the reconciliation should not be the only reviewer or approver.

Review and approval checkpoints

Reconciliations should pass through documented review before close.

Standardized reconciliation templates

Standard templates help teams apply consistent checks across accounts.

Documentation requirements for audit readiness

Each reconciliation should include source records, explanations, approvals, and open-item notes.

Common Mistakes to Avoid During Account Reconciliation

Avoiding common errors improves reconciliation quality.

Relying on balances without supporting evidence

A matching balance is not enough if there is no support behind it.

Ignoring small recurring differences

Small recurring differences can indicate larger process issues.

Posting adjustments without approval

Every adjustment should have a clear reason and approval.

Leaving open items unresolved across periods

Unresolved items should not remain open without owner tracking.

How Account Reconciliation Supports Month-End Close

Account reconciliation improves close quality by confirming account accuracy before reports are finalized.

Validation of account balances before reporting

Finance teams can confirm balances before financial statements are prepared.

Reduction of close-related corrections

Fewer unresolved differences mean fewer late corrections.

Faster review and approval processes

Clear documentation helps reviewers approve reconciliations faster.

Improved confidence in reported numbers

Reconciled accounts give finance leaders more confidence in period-end results.

How Account Reconciliation Supports Audit Readiness

Audit readiness depends on clear records and traceable balances.

Creation of a clear audit trail

Reconciliation creates a link between reported balances and source records.

Evidence supporting reported balances

Invoices, schedules, statements, and approvals support account accuracy.

Documentation of adjustments and corrections

Corrections should show what changed, why it changed, and who approved it.

Reduced audit queries and follow-up requests

Well-supported reconciliations reduce audit back-and-forth.

Why Spreadsheet-Based Reconciliation Creates Challenges

Spreadsheets become harder to manage as account volume grows.

Version-control issues

Different team members may work from different file versions.

Formula and manual-entry errors

Manual formulas and copied data can create errors.

Limited visibility into reconciliation status

It becomes difficult to see which accounts are complete, open, or overdue.

Difficulty maintaining supporting evidence

Evidence may be spread across folders, emails, and attachments.

Metrics That Measure Reconciliation Effectiveness

Metrics help finance leaders understand reconciliation quality.

Number of unresolved discrepancies

A high number of open items shows process risk.

Aging of open reconciliation items

Older items need faster review and escalation.

Percentage of accounts reconciled on time

This shows whether teams are meeting close deadlines.

Frequency of manual adjustments

Frequent adjustments may indicate weak upstream records.

Close delays linked to reconciliation issues

Close delays show where reconciliation problems affect reporting timelines.

How Automation Improves Account Reconciliation

Automation helps finance teams reduce manual work and improve exception visibility.

Automated matching of balances and transactions

Automation compares balances, transactions, schedules, and source records faster than manual review.

Continuous validation of account activity

Accounts can be checked throughout the period instead of only at month-end.

Real-time visibility into exceptions

Finance teams can see unresolved items, owners, and aging in one place.

Centralized management of supporting documentation

An account reconciliation software helps centralize matching, documentation, approvals, audit trails, and exception tracking.

What High-Performing Finance Teams Do Differently

High-performing teams treat reconciliation as an ongoing finance process.

Reconcile accounts throughout the reporting period

They review high-risk accounts before close pressure begins.

Assign clear ownership for each account

Each account has a preparer, reviewer, and escalation owner.

Monitor exceptions before close deadlines

Open items are reviewed before reporting deadlines.

Review recurring discrepancies for root-cause resolution

Recurring issues are corrected at the process level.

Future Direction of Account Reconciliation

Account reconciliation is moving toward continuous validation and better exception visibility.

AI-assisted identification of unusual transactions

AI can help identify unusual postings, duplicates, and high-risk balances.

Predictive detection of reconciliation risks

Predictive checks can flag accounts likely to delay close.

Continuous reconciliation across finance systems

Continuous reconciliation reduces period-end pressure.

Real-time account validation supported by intelligent matching logic

The future of reconciliation depends on connected records, faster matching, and real-time visibility into account accuracy.

Sign in to leave a comment.