Some accounts can quietly distort financial reporting if they are not reviewed on time. A missed bank transaction, duplicate vendor invoice, unreconciled customer balance, or unsupported prepaid expense can affect cash visibility, liabilities, working capital, and audit readiness. The issue becomes bigger when finance teams treat all accounts with the same review schedule.

High-priority accounts need regular reconciliation because they carry higher transaction volume, higher risk, or higher reporting impact. This article covers 10 accounts every finance team should reconcile regularly, why each account matters, common differences, recommended review frequency, and how structured reconciliation helps finance teams close with greater confidence.

Why Some Accounts Require More Frequent Reconciliation Than Others

Some accounts change daily, while others move only at month-end. Reconciliation priority should reflect account activity and risk.

Relationship between account risk and reconciliation priority

Accounts exposed to cash movement, fraud risk, external settlements, or material balances should receive higher priority.

How transaction volume influences reconciliation frequency

High-volume accounts create more chances for missing entries, duplicate postings, and timing differences.

Impact of unreconciled high-risk accounts on financial reporting

Unreconciled accounts can affect financial statements, audit evidence, and management reporting.

How Finance Teams Decide Which Accounts Need Priority

Finance teams should classify accounts based on risk, value, and operational impact.

Materiality of account balances

Material accounts need regular review because errors can affect reported results.

Exposure to fraud, errors, and unauthorized transactions

Cash, card, and clearing accounts require closer monitoring because activity can move quickly.

Frequency of account activity

Accounts with daily activity need more frequent reconciliation than low-activity accounts.

Regulatory, audit, and compliance expectations

Tax, payroll, and statutory accounts require strong evidence and review discipline.

Effect on cash flow and working capital visibility

Cash, receivables, payables, and inventory affect liquidity and working capital reporting.

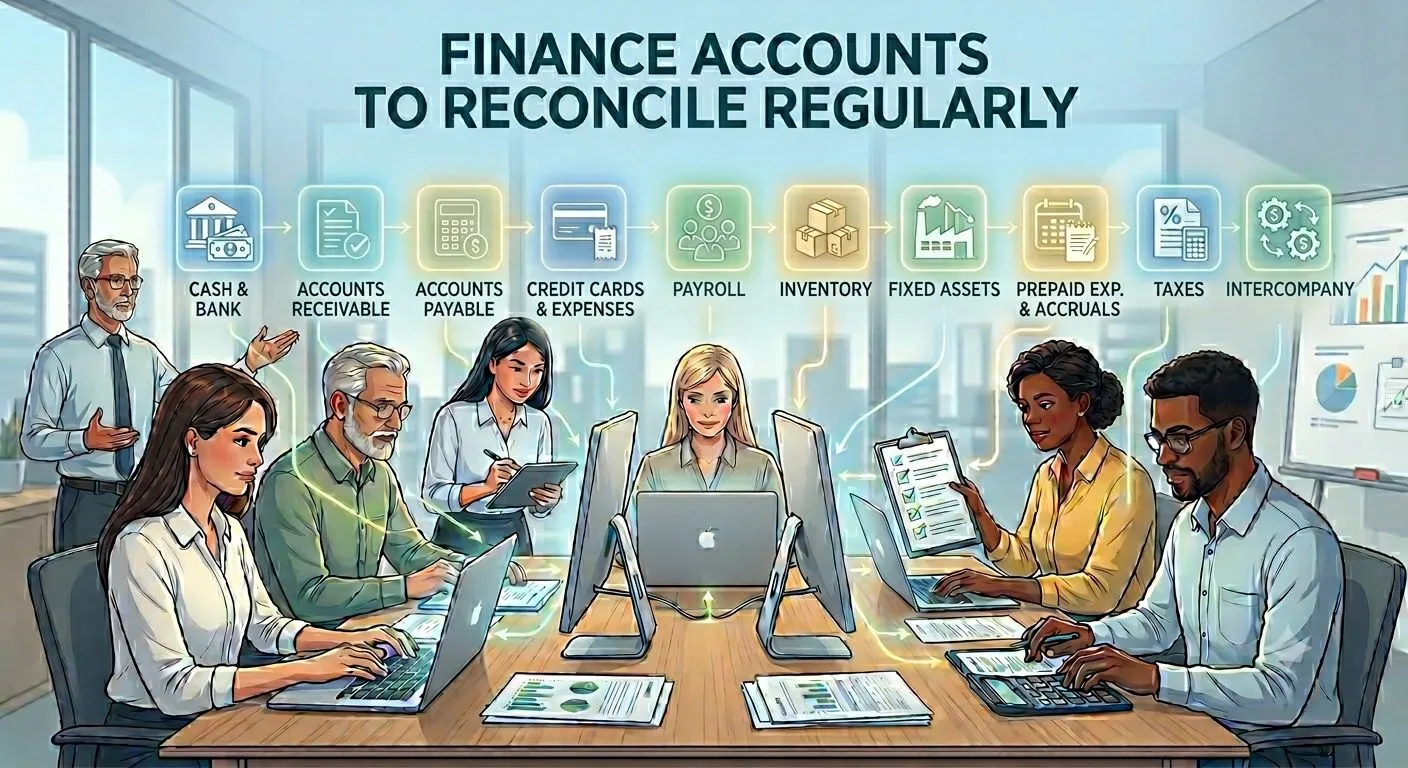

10 High-Priority Accounts Finance Teams Should Reconcile Regularly

The following accounts usually require closer review because they affect cash, liabilities, expenses, working capital, and reporting accuracy.

1. Cash and Bank Accounts

Cash and bank accounts are usually the highest-priority accounts for reconciliation.

Why cash balances require continuous validation

Cash balances affect liquidity, treasury planning, and fraud detection.

Common reconciliation differences

Common differences include deposits in transit, outstanding checks, bank fees, interest, direct debits, and unauthorized transactions.

Recommended reconciliation frequency

High-volume bank accounts should be reviewed daily. Lower-activity bank accounts may be reviewed weekly or monthly.

2. Accounts Receivable

Accounts receivable reconciliation confirms whether customer balances are accurate.

Matching customer balances with outstanding invoices

Finance teams compare customer invoices, receipts, credit notes, and open balances.

Common reconciliation differences

Common differences include unapplied cash, missing receipts, duplicate invoices, incorrect customer allocation, and disputed balances.

Recommended reconciliation frequency

High-volume receivable accounts should be reviewed daily or weekly. Full AR reconciliation should be completed before month-end close.

3. Accounts Payable

Accounts payable reconciliation validates supplier balances and outstanding obligations.

Comparing supplier balances with internal records

Finance teams compare supplier invoices, payments, credits, statements, and ledger balances.

Common reconciliation differences

Common differences include duplicate invoices, missing credits, delayed payments, incorrect invoice references, and unsupported adjustments.

Recommended reconciliation frequency

AP accounts should be reviewed weekly or monthly, depending on invoice volume and supplier-payment activity.

4. Corporate Credit Card and Expense Accounts

Corporate card and expense accounts need close review because they involve employee spending.

Matching card transactions with employee expense records

Finance teams compare card statements, receipts, expense reports, approvals, and ledger postings.

Common reconciliation differences

Common differences include missing receipts, duplicate expense claims, personal spending, delayed card feeds, and incorrect merchant categories.

Recommended reconciliation frequency

High-volume card programs should be reviewed daily or weekly. Expense balances should be reconciled before close.

5. Payroll and Employee Liability Accounts

Payroll accounts affect employee costs, deductions, taxes, and liabilities.

Reconciling payroll expenses, deductions, and liabilities

Finance teams compare payroll registers, employee records, benefit deductions, tax filings, and ledger balances.

Common reconciliation differences

Common differences include duplicate payroll entries, incorrect deductions, missing employee records, tax mismatches, and delayed corrections.

Recommended reconciliation frequency

Payroll accounts should be reconciled after each payroll run and again before month-end close.

6. Inventory Accounts

Inventory reconciliation supports asset valuation and profitability reporting.

Comparing inventory records with physical stock and valuation reports

Finance teams compare stock records, warehouse data, goods receipts, transfers, write-offs, and valuation reports.

Common reconciliation differences

Common differences include stock count variances, missing receipts, incorrect transfers, damaged goods, valuation errors, and unapproved write-offs.

Recommended reconciliation frequency

High-value or fast-moving inventory should be reviewed frequently. Full inventory reconciliation is usually completed monthly or during cycle counts.

7. Fixed Assets and Depreciation Accounts

Fixed asset reconciliation validates long-term asset balances and depreciation.

Validating acquisitions, disposals, and depreciation entries

Finance teams compare asset registers, invoices, disposal records, depreciation schedules, and ledger balances.

Common reconciliation differences

Common differences include missing asset additions, incorrect depreciation, unrecorded disposals, wrong asset classification, and outdated schedules.

Recommended reconciliation frequency

Fixed asset accounts are commonly reconciled monthly, quarterly, or during reporting close.

8. Prepaid Expenses and Accrual Accounts

Prepaids and accruals need review because they depend on schedules and estimates.

Verifying amortization schedules and accrued balances

Finance teams compare contracts, invoices, accrual schedules, amortization schedules, and journal entries.

Common reconciliation differences

Common differences include missed amortization, incorrect accrual amounts, duplicate accruals, stale balances, and unsupported adjustments.

Recommended reconciliation frequency

These accounts should be reconciled monthly before close.

9. Tax Accounts

Tax accounts require strong documentation because they affect compliance.

Reconciling tax liabilities with statutory filings

Finance teams compare tax balances with filings, payroll tax records, sales tax reports, withholding records, and payment confirmations.

Common reconciliation differences

Common differences include incorrect tax rates, timing differences, missing payments, filing mismatches, and unsupported tax adjustments.

Recommended reconciliation frequency

Tax accounts should be reconciled monthly and reviewed again during filing periods.

10. Intercompany and Clearing Accounts

Intercompany and clearing accounts can create major close delays if not reviewed regularly.

Validating balances across entities and business units

Finance teams compare balances between related entities, transfer records, invoices, settlement activity, and clearing account movements.

Common reconciliation differences

Common differences include mismatched intercompany entries, currency differences, missing settlement records, timing gaps, and unresolved clearing balances.

Recommended reconciliation frequency

High-activity clearing accounts may need daily or weekly review. Intercompany balances should be reconciled monthly before consolidation.

Accounts That May Need Daily, Weekly, or Monthly Review

Reconciliation frequency should vary by account type.

High-volume operational accounts

Cash, payment gateways, receivables, card, and clearing accounts may require daily or weekly review.

Period-end accounting accounts

Prepaids, accruals, fixed assets, and tax accounts often require monthly review.

Risk-based reconciliation scheduling

Finance teams should schedule reviews based on transaction volume, risk, materiality, and close impact.

Common Reconciliation Issues Across High-Priority Accounts

High-priority accounts often share similar reconciliation issues.

Missing transactions

Transactions may be recorded in one system but not another.

Duplicate entries

Duplicate postings can overstate balances or expenses.

Timing differences

Timing gaps occur when systems update in different periods.

Incorrect account classifications

Transactions may be posted to the wrong account, entity, or cost center.

Unsupported adjustments

Adjustments without approval or documentation create audit concerns.

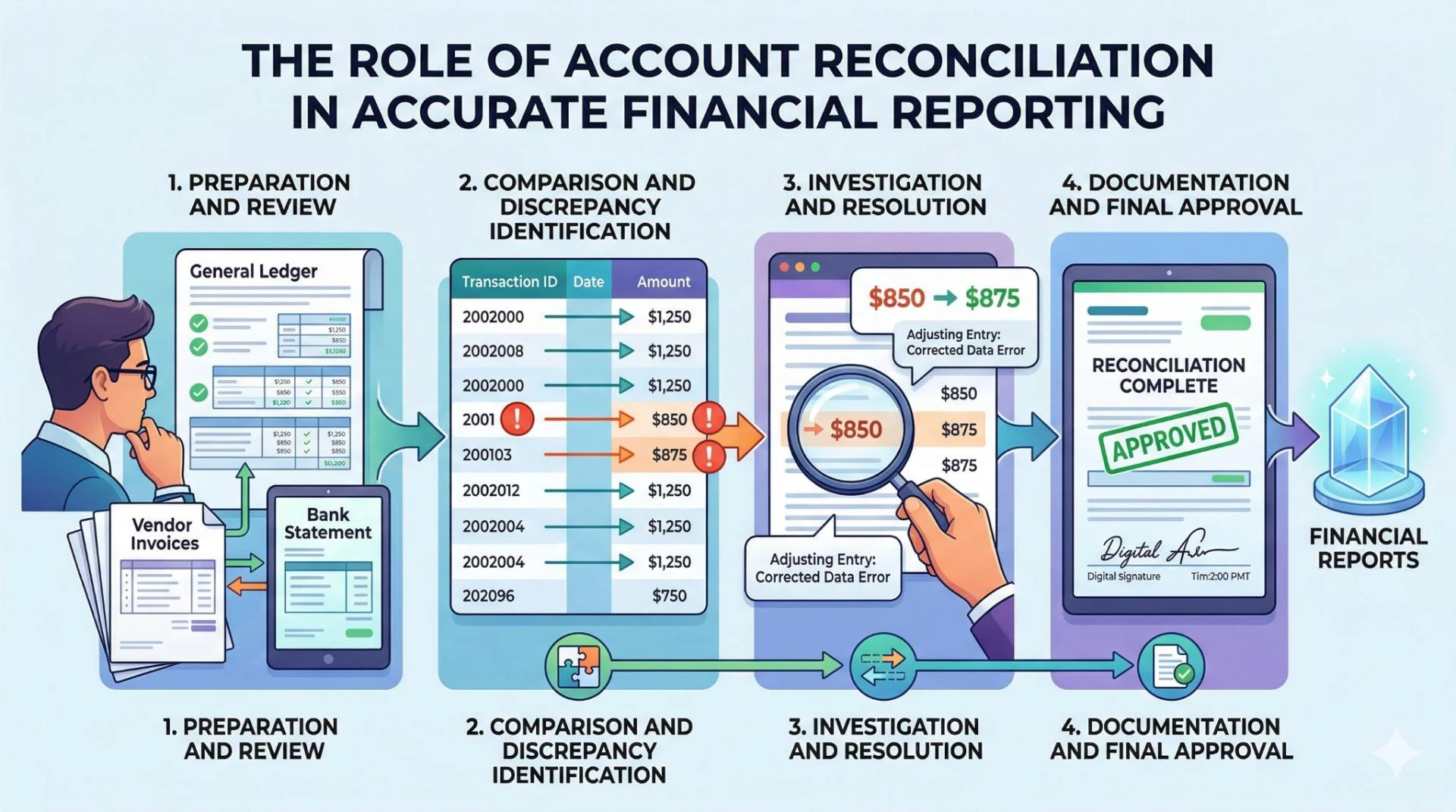

How High-Priority Accounts Affect Month-End Close

High-priority accounts directly influence close quality.

Relationship between reconciled balances and reporting accuracy

Accurate balances depend on completed reconciliations.

Impact on financial-close timelines

Open items delay review and reporting.

Reduction of post-close adjustments

Early reconciliation reduces late corrections.

Support for audit readiness

Well-documented reconciliations support audit evidence. Strong account reconciliation helps finance teams validate balances before reports are finalized.

Reconciliation Priorities in Multi-Entity Organizations

Multi-entity finance teams face additional reconciliation requirements.

Shared ERP environments across subsidiaries

Shared systems need consistent account ownership and coding rules.

Cross-border transactions and currency differences

Currency movement and local settlement timing can create differences.

Intercompany balance validation

Both sides of intercompany activity should match before consolidation.

Centralized reconciliation governance

Central governance helps maintain consistent schedules and evidence standards.

Risks of Managing High-Priority Accounts Through Spreadsheets

Spreadsheets create problems as reconciliation volume grows.

Version-control issues

Different file versions can create conflicting results.

Formula and manual-entry errors

Manual work increases the risk of incorrect balances.

Limited visibility into unresolved discrepancies

Open items may be difficult to track.

Difficulty maintaining supporting documentation

Evidence may sit across files, emails, and folders.

Controls That Keep High-Priority Accounts Accurate

Controls help finance teams reduce recurring issues.

Risk-based reconciliation calendars

Higher-risk accounts should be reviewed more frequently.

Segregation of preparer and reviewer responsibilities

The person preparing a reconciliation should not be the only reviewer.

Approval workflows for adjustments

Corrections should have proper approval and support.

Documentation standards supporting audits

Each reconciliation should include source records, explanations, and sign-off evidence.

Metrics That Reveal the Health of High-Priority Accounts

Metrics show whether account review is working.

Percentage of accounts reconciled on time

This shows close readiness.

Number of unresolved reconciliation items

Open items show review risk.

Aging of outstanding discrepancies

Older items need escalation.

Frequency of manual adjustments

Frequent adjustments may indicate process issues.

Financial-close delays linked to reconciliation issues

Close delays reveal accounts that need more attention.

How Automation Improves Reconciliation of High-Priority Accounts

Automation helps teams monitor high-priority accounts more consistently.

Automated matching across financial records

Systems can compare ledgers, subledgers, bank records, invoices, statements, and schedules.

Continuous monitoring of account activity

High-risk accounts can be reviewed throughout the period.

Real-time visibility into reconciliation exceptions

Dashboards show open items, aging, and owners.

Centralized management of supporting documentation

Centralized evidence improves review and audit readiness.

What High-Performing Finance Teams Do Differently

Strong finance teams prioritize accounts based on risk.

Prioritize accounts based on risk and materiality

They focus review effort where reporting impact is highest.

Resolve exceptions throughout the reporting period

They avoid leaving all exceptions for month-end.

Monitor recurring reconciliation trends

Recurring differences are reviewed for root cause.

Review reconciliation schedules regularly

Review schedules change as account activity changes.

Future Direction of High-Priority Account Reconciliation

High-priority reconciliation is moving toward continuous monitoring.

AI-assisted identification of high-risk account activity

AI can flag unusual activity, duplicates, and high-risk balances.

Predictive detection of reconciliation exceptions

Predictive checks can identify accounts likely to delay close.

Continuous reconciliation across finance systems

Continuous reconciliation reduces period-end pressure.

Real-time account monitoring supported by intelligent matching logic

These 10 accounts are among the most frequently reviewed accounts, but reconciliation requirements vary by business model and financial structure. Finance teams can explore the broader types of account reconciliation to identify other accounts that may require periodic review.

Sign in to leave a comment.