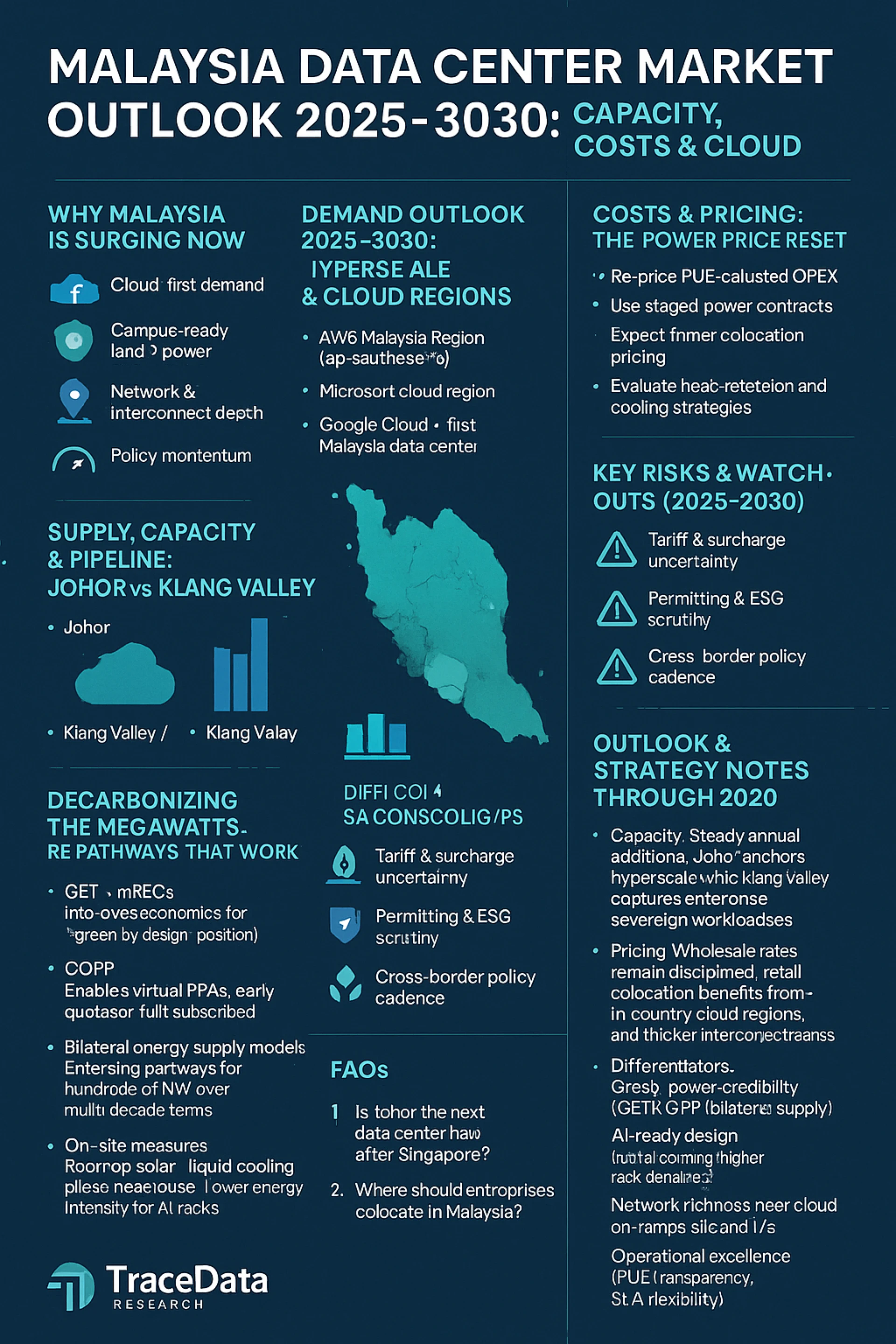

Malaysia’s data center market is evolving from a Singapore spillover to a primary build destination. Strong hyperscaler commitments (AWS, Microsoft, Google), Johor’s hyperscale campuses, and cross-border collaboration with Singapore are driving multi-gigawatt pipelines. The flip side: higher electricity tariffs, tightening permits, and the need for credible renewable energy (RE) strategies. From 2025–2030, expect steady capacity additions anchored in Johor and Klang Valley, with pricing shaped by power costs and RE procurement.

Why Malaysia Is Surging Now

- Cloud-first demand: In-country cloud regions reduce latency and meet data-residency needs.

- Campus-ready land + power: Johor offers large, contiguous parcels suited to AI-era densities.

- Network & interconnect depth: Klang Valley/Cyberjaya remains the enterprise and peering core.

- Policy momentum: Cross-border SEZ collaboration, digital infrastructure incentives, and grid upgrades.

Demand Outlook 2025–2030: Hyperscale & Cloud Regions

- AWS Malaysia Region (ap-southeast-5) expands low-latency options for regulated industries.

- Microsoft cloud region unlocks enterprise migration, analytics, and GenAI adoption.

- Google Cloud + first Malaysia data center signals long-term platform investment.

What this means: Cloud adoption converts into colocation uptake, interconnect growth, edge caching, AI training/finetuning clusters, and DR footprints, supporting multi-year utilization of wholesale halls.

Supply, Capacity & Pipeline: Johor vs. Klang Valley

Johor (Sedenak/Kulai/Iskandar) has scaled from low double-digit MW earlier in the decade to GW-class campuses today. Phased deliveries (e.g., ~25MW blocks within 100MW-class builds) are common.

Klang Valley/Cyberjaya remains the interconnect-rich core for enterprise colocation and hybrid workloads.

Notable developers/operators to watch: YTL (with GDS), Vantage, Yondr, K2, BrightRay and others—designing liquid-cool-ready halls for AI densities.

Policy Tailwinds: JS-SEZ, Incentives & Grid Upgrades

- Johor–Singapore Special Economic Zone (JS-SEZ): Streamlines flows of people and goods, strengthening a unified cross-border investment narrative.

- Incentive frameworks: Digital infrastructure and green-tech aligned programs improve project viability.

- Grid expansion: Transmission reinforcements, new substations, and backbone upgrades will gate new MW timelines—plan for phased energization.

Costs & Pricing: The Power Price Reset

From mid-2025, revised tariff structures and surcharges recalibrate electricity costs—a critical input for large data centers.

Implications for buyers & operators

- Re-price PUE-adjusted OPEX and refresh TCO models.

- Use staged power contracts to manage volatility.

- Expect firmer wholesale colocation pricing on new builds.

- Evaluate heat-rejection and cooling strategies (air → liquid/immersion readiness) to control power intensity.

Decarbonizing the Megawatts: RE Pathways That Work

- GET (Green Electricity Tariff) + mRECs: Improves economics for “green by design” positioning.

- CGPP (Corporate Green Power Programme): Enables virtual PPAs; early quotas are fully subscribed—helpful for long-dated RE.

- Bilateral energy supply models: Emerging pathways for hundreds of MW over multi-decade terms.

- On-site measures: Rooftop solar, liquid cooling pilots, heat reuse—lower energy intensity for AI racks.

Takeaway: Buyers increasingly ask for auditable green power. Bankable RE strategy = faster leasing cycles and better enterprise win rates.

Location Strategy: Where to Place Workloads

Johor (Sedenak / Kulai / Iskandar)

- Best for: Large, multi-building hyperscale campuses, AI-dense halls, Singapore adjacency.

- Watch: Grid connection timelines, water allocation, and environmental approvals.

Klang Valley / Cyberjaya

- Best for: Enterprise and regulated workloads, dense peering, cloud on-ramps, metro DR.

- Watch: Land availability by zone, fiber routes, and upgrade windows for power.

Key Risks & Watch-Outs (2025–2030)

- Tariff & surcharge uncertainty

- Re-underwrite power lines annually; build pass-through flexibility into SLAs.

- Permitting & ESG scrutiny

- Expect tighter water-use, cooling, and environmental oversight—engage early.

- Cross-border policy cadence

- JS-SEZ execution (immigration, customs, logistics) drives latency-sensitive placement.

- Supply competition

- New Singapore capacity releases can rebalance demand across the SIJORI triangle.

Outlook & Strategy Notes Through 2030

- Capacity: Steady annual additions; Johor anchors hyperscale while Klang Valley captures enterprise/sovereign workloads.

- Pricing: Wholesale rates remain disciplined; retail colocation benefits from in-country cloud regions and thicker interconnect fabrics.

- Differentiators:

- Green-power credibility (GET/CGPP/bilateral supply)

- AI-ready design (liquid cooling, higher rack densities)

- Network richness near cloud on-ramps and IXs

- Operational excellence (PUE transparency, SLA flexibility)

FAQs: Malaysia Data Center Market

1) Is Johor the next data center hub after Singapore?

Yes—Johor’s land, power, and proximity to Singapore make it ideal for GW-scale campuses and AI workloads.

2) Where should enterprises colocate in Malaysia?

Klang Valley/Cyberjaya for interconnect and compliance, paired with Johor for scale and DR.

3) How will power tariffs affect data center pricing?

Higher tariffs drive firmer wholesale rates and tighter OPEX control; RE procurement helps offset volatility.

4) What renewable energy options exist for data centers in Malaysia?

GET, CGPP/virtual PPAs, and bilateral supply models—plus on-site solar and liquid cooling to reduce energy intensity.

5) What matters most when selecting a Malaysia DC site?

Power timelines, RE strategy, cooling design, network proximity, permitting path, and total landed cost.

How TraceData Research Can Help

TraceData partners with operators, investors, and enterprises to size demand, benchmark pricing, evaluate sites, and design RE strategies that win. From market scans and capacity maps to colocation pricing analysis and AI-ready facility assessments, we deliver decision-grade insights.

Contact Us-

TraceData Research

+91 9266849840

Sign in to leave a comment.