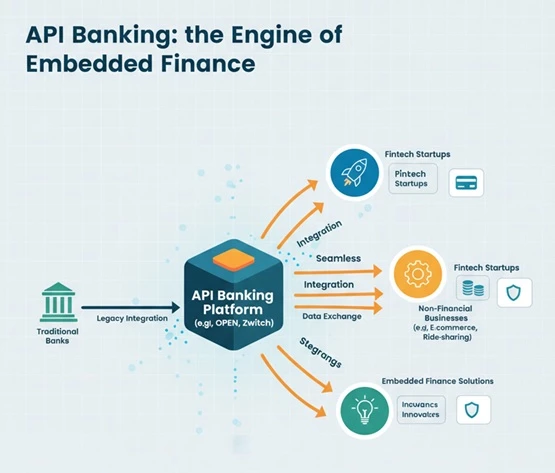

This visually represents API banking as a central hub connecting "Traditional Banks" and various "Fintech Startups" and "Non-Financial Businesses" (e.g., e-commerce, ride-sharing). Arrows emphasize "Seamless Integration" and "Data Exchange" from the API Banking Platform (e.g., OPEN, Zwitch) to "Embedded Finance Solutions" (e.g., Payments, Lending, Insurance) within these applications. The design is professional, with orange accents that illustrate fluid data flow.

How API Banking Is Powering the Embedded Finance Wave

Financial services are no longer confined to bank branches or standalone apps. They’re increasingly embedded directly into the digital experiences people already use—ride-hailing platforms, e-commerce marketplaces, SaaS tools, and super-apps.

At the core of this shift sits API banking.

API banking provides the infrastructure that allows financial services to be delivered contextually, at scale, and without rebuilding banking systems from scratch. For startups and platforms building embedded finance products, it’s not a nice-to-have—it’s foundational.

API Banking: The Infrastructure Layer Behind Embedded Finance

At its simplest, API banking enables secure, real-time exchange of financial data and services between banks and third-party platforms. But its real impact lies in what it unlocks.

For startups, APIs dramatically reduce the cost and time required to launch financial products. Instead of building payment rails, compliance systems, or ledger infrastructure internally, they can integrate pre-built banking capabilities directly into their platforms.

For banks, this represents a structural shift. Rather than relying primarily on interest-based income, banks increasingly operate as infrastructure providers—earning non-interest revenue by exposing their capabilities through APIs and Banking-as-a-Service (BaaS) models.

This collaborative model—banks providing regulated infrastructure, startups building customer-centric experiences—has become the dominant pattern in embedded finance.

Market Momentum: Why Embedded Finance Is Accelerating

The growth numbers around embedded finance are aggressive—and they matter because they reflect real platform adoption, not hype.

Globally, the embedded finance market was valued at USD 108.55 billion in 2024 and is projected to grow to USD 1.2 trillion by 2033, at a CAGR of roughly 28.5%. This is not a niche trend; it’s a structural re-architecture of financial distribution.

The momentum is even stronger in emerging, mobile-first regions:

- APAC is projected to grow at 36.7% annually, reaching USD 306.59 billion by 2029.

- MENA crossed USD 1 billion in fintech investments in 2024, with embedded finance revenues expected to reach USD 3.5–4.5 billion by 2025.

These regions share common characteristics: high smartphone penetration, fragmented banking access, and platforms that already own user trust. Embedded finance fits naturally into this environment.

How Startups Are Using APIs to Build Embedded Finance Products

Embedded finance works because it removes friction. Financial actions happen in context—when the user already has intent.

Common use cases include:

- Payments embedded into ride-sharing and delivery apps, eliminating the need for external checkout flows

- Micro-loans for online merchants, triggered by sales volume and transaction history

- Super-apps like Grab in Southeast Asia, combining transportation, food delivery, wallets, lending, and insurance in a single ecosystem

Through open banking and BaaS platforms, startups access regulated bank infrastructure via APIs to offer:

- Digital wallets and instant payments for seamless checkout

- Contextual lending, such as BNPL, supply-chain financing, or point-of-sale credit

- Embedded insurance, bundled directly into relevant purchases

The key advantage isn’t just speed—it’s relevance. Financial products appear exactly when they’re needed.

The Role of AI in Scaling Embedded Finance

As embedded finance matures, AI becomes a competitive necessity, not an add-on.

AI enables:

- Personalised financial experiences by analysing transaction behaviour, usage patterns, and risk signals. Generative AI allows this personalisation to scale without manual rule-building.

- Improved customer journeys through AI-driven chatbots and virtual assistants that handle onboarding, support, and routine queries in real time.

- Fraud detection and risk management, using predictive analytics to flag anomalies. With global fraud losses exceeding USD 1 trillion in 2023, this is mission-critical infrastructure.

- Operational efficiency, by automating reconciliation, increasing API throughput, and reducing manual intervention across financial workflows.

In short, APIs move money; AI decides how, when, and for whom.

Regulation, Trust, and Financial Inclusion

Regulation is often framed as a constraint—but in embedded finance, it’s a trust enabler.

Across Southeast Asia and the Middle East, regulators are actively defining open banking frameworks:

- Singapore, Malaysia, and Indonesia continue to formalise API and data-sharing standards

- Saudi Arabia’s Open Banking Framework entered phase two in 2024

While navigating multi-jurisdictional compliance is complex—especially around data privacy and licensing—clear regulatory boundaries increase consumer confidence and platform adoption.

Embedded finance also plays a tangible role in financial inclusion. By embedding payments, credit, and insurance into platforms people already use, startups can reach underbanked and unbanked populations more effectively than traditional banking ever could—particularly in Southeast Asia.

Closing Perspective

API banking is no longer a backend technical decision—it’s a strategic lever.

For next-generation startups, it provides the modularity and flexibility required to launch, iterate, and scale embedded finance products without owning banking complexity. Combined with AI, regulatory clarity, and platform-led distribution, it enables entirely new financial experiences that feel invisible, contextual, and intuitive.

Finance isn’t becoming a separate destination. It’s becoming part of everything—and API banking is what makes that possible.

Sign in to leave a comment.