Getting declined for a car loan hits harder than most people expect. You finally find a car you like, submit your application, and then reject it. No clear explanation, just a vague “credit criteria not met.”

If that sounds familiar, you’re not alone. Across Australia, thousands of people are turned down by banks and dealerships every month. But here’s the part most people don’t realise:

There are car options that don’t rely on your credit score at all.

And that’s where rent-to-own car programs come in.

Why do banks reject so many car loan applications?

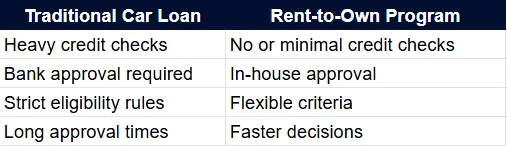

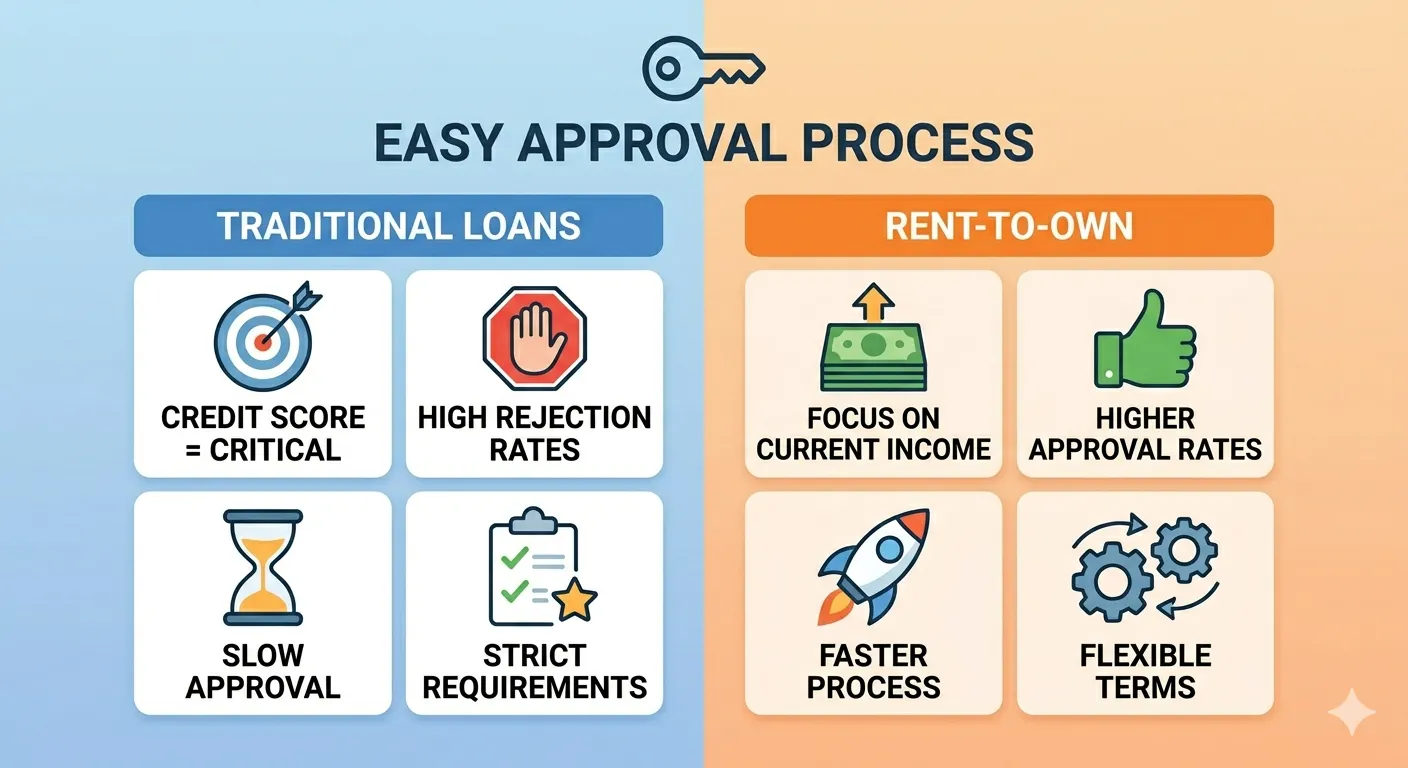

Banks don’t just look at whether you can afford repayments. They focus heavily on your financial history.

Here’s what typically works against you:

- No credit history

- Missed payments in the past

- Short employment history

- Existing debts

Even if you’re earning now, banks often see you as “high risk.”

What makes rent-to-own approval easier?

Rent-to-own flips the traditional system. Instead of judging your past, it focuses on your current ability to pay and your consistency moving forward.

Here’s the key difference:

This is the main reason approval rates are significantly higher.

How does rent-to-own actually work?

If you’ve never looked into it before, it’s simpler than it sounds.

Step-by-step:

1. You choose a car based on your income

2. You agree on a weekly payment plan

3. You start driving the car immediately

4. Over time, ownership transfers to you

No complex loan structures. No dealing with banks. Just a more direct path to getting on the road.

Is it really possible to get approved without a credit check?

In many cases, yes. That’s because providers are more interested in:

- Your current income

- Your ability to make regular payments

- Your stability right now

Not what happened years ago. For someone who’s been declined before, this can be a game changer.

Who benefits the most from rent-to-own?

This option isn’t for everyone, but it’s incredibly useful for specific situations.

It’s a strong fit if you:

- Were recently declined by a bank

- Have bad or no credit history

- Need a car urgently for work

- Are rebuilding financially

What are the biggest advantages?

Let’s break it down in practical terms.

✔ Faster approvals

You’re not stuck waiting for bank processing times.

✔ Lower barriers to entry

No need for a perfect financial history.

✔ Flexible payment structures

Payments are often tailored to your situation.

✔ Immediate access to a car

You can start driving sooner, not later.

Are there things you should watch out for?

Yes, and this is where many articles fall short. Before jumping in, make sure you:

- Understand the full payment structure

- Check what happens if you miss a payment

- Confirm when ownership officially transfers

- Read the agreement carefully

A good provider will always be transparent about these details.

How do you find the right provider in Australia?

Not all rent-to-own programs are the same.

Look for:

- Clear terms and conditions

- Flexible payment options

- Good customer support

- A straightforward application process

If you’re currently searching for rent to own cars near me, it’s worth exploring trusted providers like CarCoop that focus on accessibility and fast approvals without the usual bank hurdles.

Why is this becoming more popular in Australia?

There’s a growing shift happening. More Australians are:

- Working gig jobs

- Moving countries without credit history

- Rebuilding after financial setbacks

Traditional lending hasn’t adapted fast enough.

Rent-to-own fills that gap by offering a more realistic path to car ownership.

So, is rent-to-own actually worth it?

If you’ve been knocked back by a bank, it can feel like you’ve hit a wall.

And honestly, that’s where a lot of people just stop trying.

But rent-to-own isn’t really a “backup plan.” For many people, it ends up being the option that actually works with their situation, not against it.

You don’t need a perfect credit history.

You don’t need to tick every box banks expect.

You just need something that lets you get back on the road and keep moving forward.

Final thoughts

Getting declined sucks. There’s no way around it.

But it doesn’t mean you’re out of options, even if it feels like it at the time.

Some paths just aren’t built for everyone, especially if your credit history isn’t ideal. That’s exactly why options like rent-to-own exist in the first place.

For a lot of people, it’s less about “what’s the best financial product” and more about “what actually lets me get a car now so I can work, earn, and sort things out.”

That’s also why spending a bit of time understanding rent to own car programs in Australia can make a big difference. Once you see how it actually works, it starts to feel a lot more realistic and less like a last resort.

Have you ever felt stuck by traditional banking rules? Let us know your thoughts below.

Sign in to leave a comment.