In today’s dynamic lending landscape, the stakes for financial institutions have never been higher. With rising customer expectations, increased competition, and the growing complexity of risk profiles, minimizing loan defaults has become mission-critical.

That’s where predictive analytics steps in—not just as a buzzword, but as a transformative technology. Across the banking and fintech sector, institutions are now embracing data-driven forecasting to identify high-risk borrowers, optimize credit decisions, and mitigate non-performing loans.

So how exactly does predictive analytics reduce loan defaults? Let’s explore.

Understanding the Problem: Why Loan Defaults Still Hurt Lenders

Despite advancements in digital lending, loan defaults remain a significant challenge. According to industry data, even a small percentage of non-performing loans (NPLs) can eat away at profitability and operational stability.

Common causes of loan defaults include:

- Inadequate credit assessments

- Outdated risk models

- Economic downturns or job loss

- Fraudulent applications

- Lack of personalized loan structuring

Traditional credit scoring systems often rely heavily on static indicators like income, employment history, or past repayment. But they fall short in accounting for nuanced, real-time borrower behavior—especially in an era where consumer behavior is constantly evolving.

Enter Predictive Analytics: A Smarter Way to Assess Risk

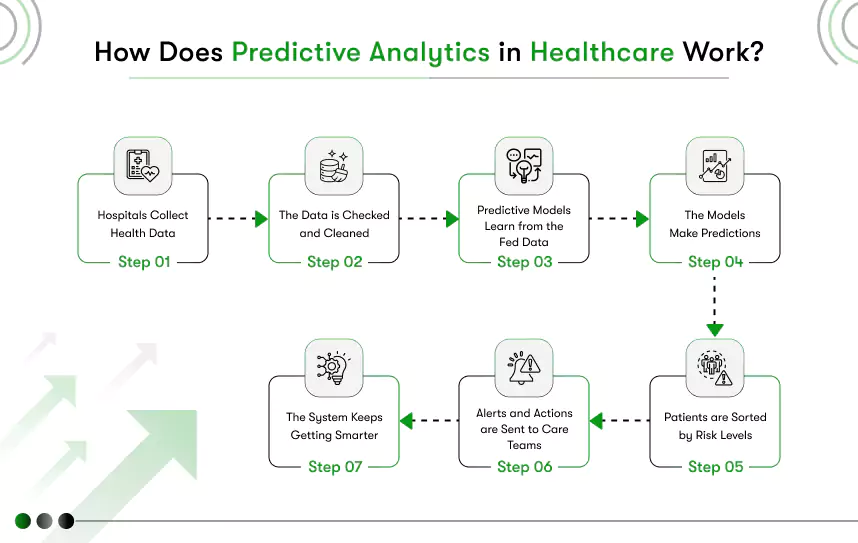

Predictive analytics uses statistical techniques, machine learning, and historical data to identify patterns and forecast future borrower behavior. By analyzing variables like transaction history, social behavior, digital footprints, and economic signals, predictive models can accurately assess the likelihood of a loan default—long before it happens.

Key technologies involved include:

- Machine Learning (ML) algorithms

- Natural Language Processing (NLP)

- Big Data integration

- Real-time behavioral tracking

- AI-powered credit scoring

How Predictive Analytics Reduces Loan Defaults—A Deep Dive

1. Improved Credit Scoring and Risk Profiling

Traditional scoring often gives equal weight to borrowers with vastly different financial behaviors. Predictive analytics enables lenders to go beyond surface-level data and include a broader set of indicators:

- Payment behavior trends

- Employment volatility

- Spending patterns

- Social and digital activity (e.g., mobile data, browsing habits)

This results in a more dynamic and accurate risk profile, helping lenders avoid approving loans to borrowers with concealed financial instability.

2. Early Warning Systems

One of the most powerful outcomes of predictive analytics is the development of early warning systems. These models flag borrowers who show signs of potential default — such as irregular spending, late payments, or sudden drops in income.

This allows banks and NBFCs to take proactive measures:

- Restructure loans

- Offer grace periods

- Engage borrowers early to find repayment solutions

The ability to intervene before a default not only saves costs but also improves customer relationships.

3. Fraud Detection and Prevention

Predictive analytics is instrumental in identifying fraud-prone applications during onboarding. Machine learning models analyze anomalies in application data, device usage, and behavior patterns to flag suspicious activities.

For instance, if an applicant’s behavior deviates from past borrower norms or shows inconsistencies across devices and locations, the system can alert risk teams instantly.

4. Loan Personalization and Dynamic Structuring

Borrowers are more likely to default when loan structures don’t align with their income cycle or repayment capacity. Predictive analytics enables personalized loan offerings, helping fintech companies structure:

- Flexible EMI plans

- Custom interest rates

- Seasonal repayment schedules

By aligning repayment with the borrower’s behavior, lenders reduce friction and increase the likelihood of timely payments.

5. Portfolio Monitoring and Adjustment

Beyond individual borrowers, predictive analytics helps monitor entire loan portfolios in real time. Lenders can detect macro patterns—like increasing default risks in a particular region, industry, or customer segment—and make proactive changes to lending policies.

Real-World Results: Predictive Analytics in Action

Several fintech innovators and digital banks are already seeing results:

- Reduced NPL ratios by over 25% in 12 months

- Faster loan approvals with better default prediction

- Increased customer satisfaction through personalization

- Lower operational costs through automated risk assessments

These outcomes aren’t limited to large banks. Even emerging fintech startups are leveraging predictive analytics tools to gain a competitive edge in credit risk management.

Platforms like Kody Technolab offer specialized predictive analytics consulting that helps businesses navigate technical complexity while ensuring strategic value and compliance.

Future Outlook: Predictive Analytics Will Be the Backbone of Lending

As AI and data technologies mature, predictive analytics will become the default standard for credit decision-making across the world.

We’re already seeing:

- AI-powered underwriting engines

- Conversational AI interfaces recommending loan options

- Real-time credit scoring via mobile apps

- Embedded lending through fintech APIs

In this context, the ability to predict and prevent loan defaults won’t be a competitive edge—it’ll be a basic necessity for survival.

Final Thoughts

Predictive analytics is not just about minimizing losses; it’s about maximizing opportunity. By helping lenders make faster, smarter, and more personalized decisions, it enables financial institutions to thrive in an increasingly uncertain lending environment.

If you’re in the lending space, whether a traditional bank, digital lender, or fintech startup, now is the time to explore how predictive analytics reduces loan defaults and reshapes credit risk management.

Sign in to leave a comment.