Month-end close becomes difficult when finance teams are still searching for missing transactions, resolving balance differences, and validating account activity at the last minute. As transaction volumes grow across payables, receivables, payroll, expenses, and cash management, even small discrepancies can delay reporting and create uncertainty around financial results.

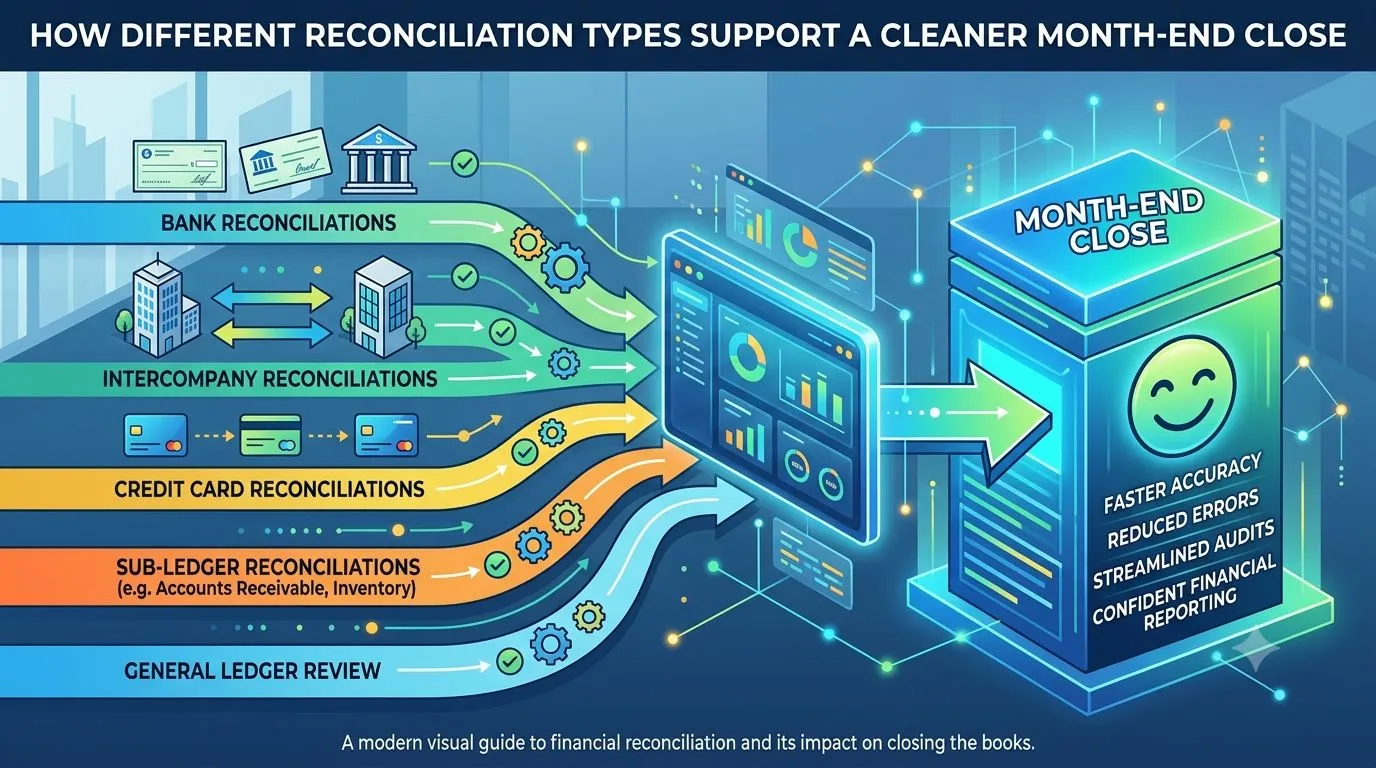

The challenge is that no single reconciliation process can validate every financial account. Different transaction types require different reconciliation approaches. A cleaner month-end close depends on how effectively finance teams reconcile cash, payables, payroll, expenses, inventory, and intercompany activity throughout the reporting period. In this guide, we will examine how different reconciliation types support close accuracy, reduce reporting delays, and improve confidence in financial statements.

Why Month-End Close Depends on Reconciliation Accuracy

A successful close process starts with accurate account balances.

Growth in financial transactions across finance systems before close

Organizations process thousands of transactions across ERP systems, payroll platforms, banking portals, expense systems, and procurement applications every month.

Why unresolved discrepancies create reporting delays

When discrepancies remain unresolved, finance teams spend additional time investigating balances before financial statements can be finalized.

Impact of reconciliation quality on close accuracy and confidence

Well-reconciled accounts reduce uncertainty and help management rely on reported numbers.

What Reconciliation Means in the Month-End Close Process

Reconciliation validates whether financial records accurately reflect business activity.

Definition of reconciliation in finance operations

Reconciliation compares accounting records against supporting documents, transaction sources, and external records.

Relationship between transaction validation and financial reporting

Financial reports are only as reliable as the transactions supporting them.

Why reconciliation helps confirm account accuracy before close

It identifies errors, omissions, duplicates, and timing differences before reporting deadlines arrive.

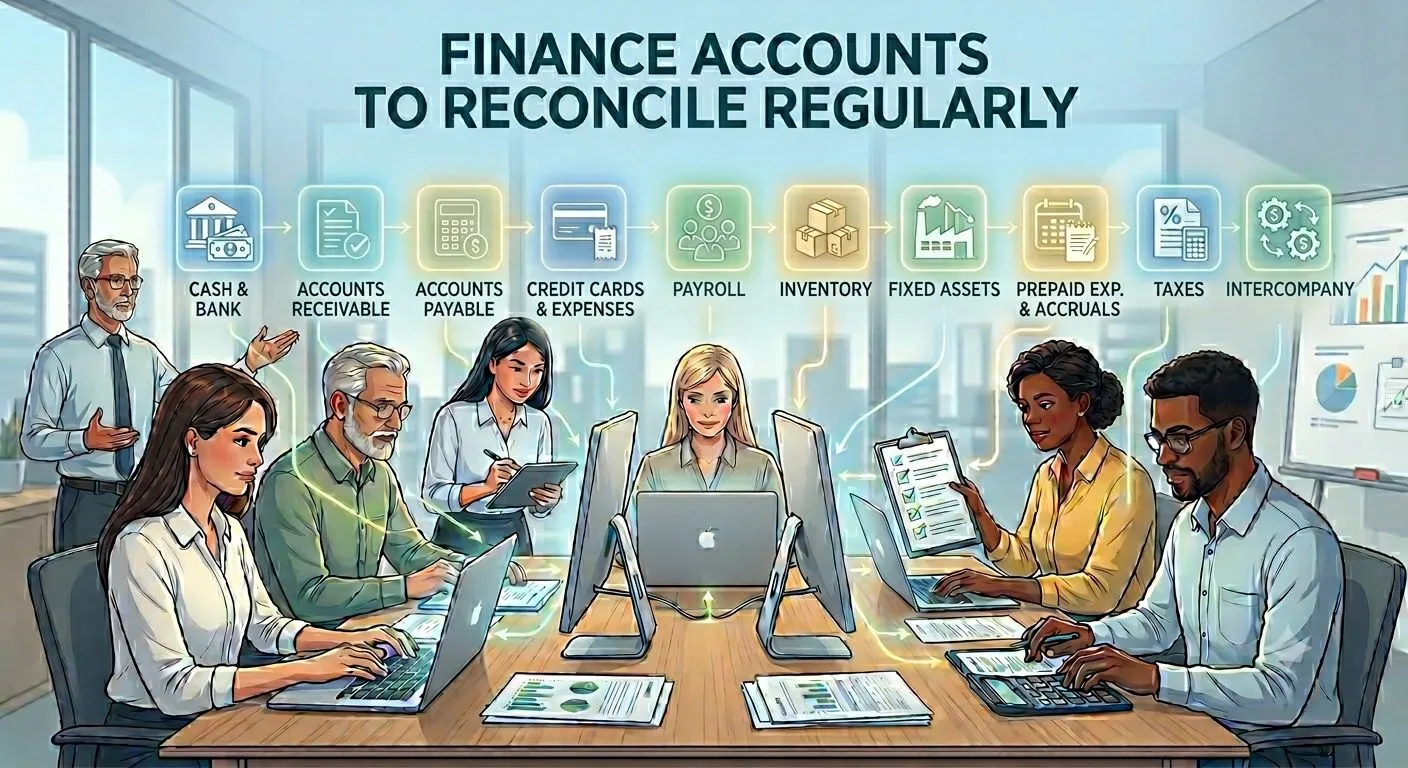

Why Different Reconciliation Types Exist Across Finance Functions

Different accounts require different validation methods.

Different transaction sources require different validation methods

Bank transactions, supplier invoices, payroll records, and expense claims each have unique supporting records.

Relationship between operational records and accounting balances

Accounting balances must match the operational activity that generated them.

Why no single reconciliation process covers every account

Each account category presents different risks, transaction volumes, and reporting requirements.

How Reconciliation Supports a Cleaner Month-End Close

Reconciliation acts as a quality check before reporting begins.

Identification of discrepancies before reporting deadlines

Issues are detected earlier when reconciliations occur continuously throughout the month.

Validation of balances before financial statements are prepared

Validated balances reduce the need for late-stage corrections.

Reduction of manual corrections during close

Fewer unresolved issues mean less rework during reporting.

Better visibility into unresolved accounting issues

Teams can focus on exceptions instead of reviewing every transaction manually.

Bank Reconciliation and Its Role in Month-End Close

Bank reconciliation validates whether recorded cash activity matches bank records.

Validation of bank balances against general ledger records

Bank balances should align with ledger balances after timing differences are accounted for.

Review of deposits in transit and outstanding payments

Deposits and payments that have not yet settled explain temporary differences.

Common bank-reconciliation issues affecting close timelines

Missing transactions, delayed settlements, and duplicate entries often require investigation.

Why cash accuracy starts with bank reconciliation

Cash reporting depends on understanding actual bank activity.

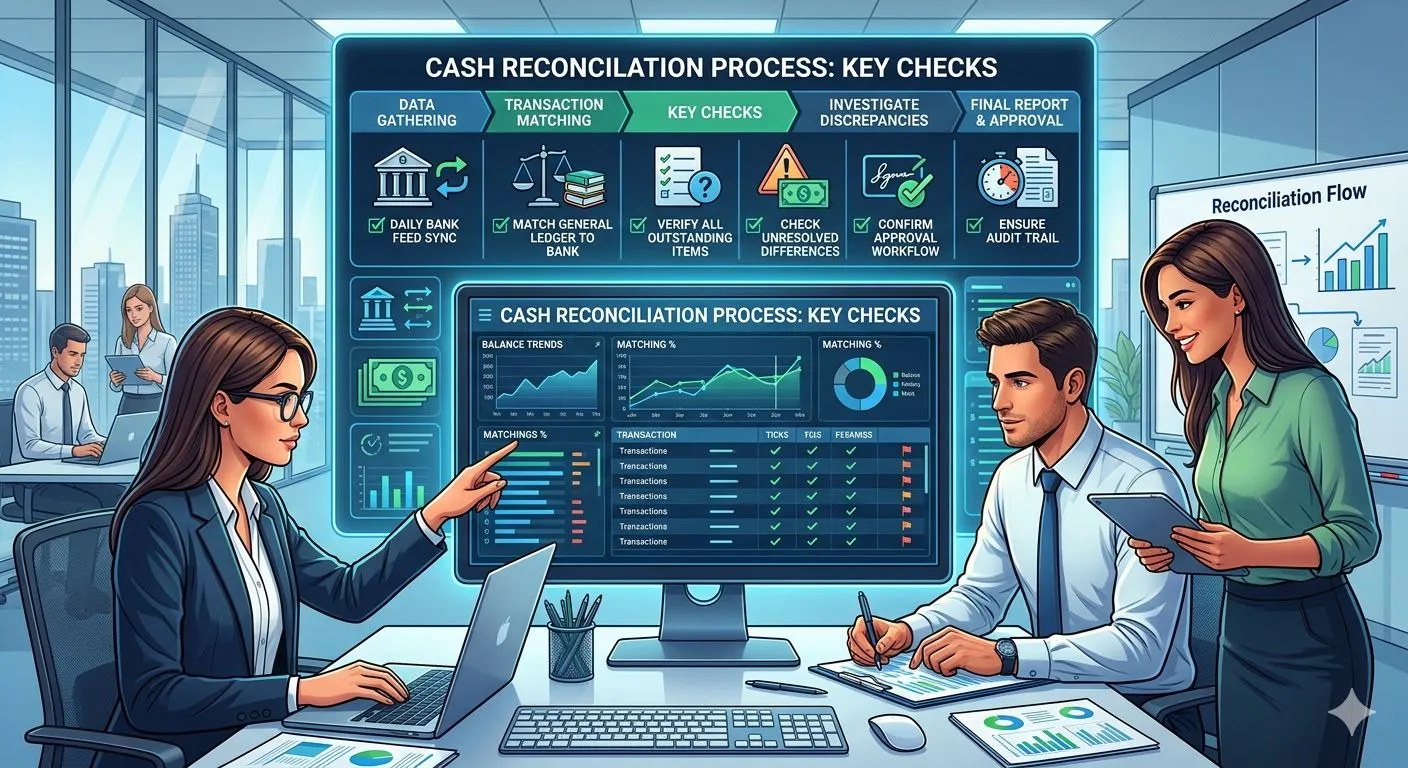

Cash Reconciliation and Liquidity Validation

Strong liquidity reporting depends on accurate cash records.

Validation of cash balances across finance and treasury records

Cash Reconciliation compares cash balances across banking, treasury, and accounting systems.

Treatment of settlement timing differences

Finance teams must identify transactions recorded in one system but not yet reflected in another.

Common cash discrepancies identified before close

Common issues include bank fees, settlement delays, duplicate payments, and missing deposits.

Impact on liquidity and working-capital reporting

Accurate cash balances improve visibility into available funds and working capital.

Accounts Receivable Reconciliation and Revenue Accuracy

Receivable reconciliation validates customer balances and collection activity.

Validation of customer invoices and collections

Finance teams compare invoices, payments, credits, and outstanding balances.

Review of unapplied cash and disputed balances

Unresolved items can distort receivable reporting.

Common receivable discrepancies affecting reporting

Incorrect allocations, missing payments, and duplicate postings frequently occur.

Relationship between AR reconciliation and revenue accuracy

Accurate receivable balances support reliable revenue reporting.

Accounts Payable Reconciliation and Liability Accuracy

Payable reconciliation validates obligations owed to suppliers.

Validation of supplier invoices and payment activity

Vendor Reconciliation helps finance teams compare supplier statements, invoices, credits, and payment records.

Review of outstanding obligations and vendor balances

Open liabilities should match supplier records and accounting balances.

Common payable discrepancies affecting close

Duplicate invoices, missing credits, and payment mismatches can affect liability reporting.

Relationship between AP reconciliation and liability reporting

Validated supplier balances support accurate liability recognition.

Payroll Reconciliation and Expense Validation

Payroll accounts represent significant financial commitments.

Validation of payroll records against accounting balances

Payroll Reconciliation compares payroll registers, tax records, deductions, and accounting entries.

Review of deductions, taxes, and employee payments

Every payroll component should reconcile with supporting records.

Common payroll discrepancies affecting period-end reporting

Incorrect deductions, duplicate payments, and timing differences are common issues.

Why payroll reconciliation supports expense accuracy

Accurate payroll balances contribute to reliable expense reporting.

Inventory Reconciliation and Asset Accuracy

Inventory often represents one of the largest balance sheet assets.

Validation of inventory balances against operational records

Inventory records should align with warehouse activity and physical counts.

Review of write-offs, transfers, and valuation adjustments

These activities directly affect reported inventory value.

Common inventory discrepancies affecting profitability reporting

Missing stock movements and valuation differences can distort results.

Relationship between inventory reconciliation and balance-sheet accuracy

Reliable inventory balances improve asset reporting quality.

Credit Card and Expense Reconciliation Before Close

Expense activity affects profitability and budget reporting.

Validation of card transactions against expense records

Finance teams compare card activity with receipts, expense reports, and accounting entries.

Review of receipts, approvals, and reimbursements

Missing documentation creates reporting risk.

Common spend-related discrepancies affecting reporting

Duplicate claims, missing receipts, and coding errors frequently occur.

Why expense reconciliation improves spend visibility

Expense Reconciliation helps finance teams understand actual spending activity before close.

Intercompany Reconciliation Across Multi-Entity Organizations

Intercompany balances require additional attention.

Validation of intercompany balances between entities

Balances recorded by one entity should match balances recorded by the other.

Settlement tracking and elimination requirements

Settlement activity must be tracked before consolidation.

Common intercompany mismatches affecting consolidated reporting

Timing differences and inconsistent accounting treatment often create issues.

Why intercompany reconciliation often delays close

Unresolved intercompany balances can hold up consolidated reporting.

Why Timing Differences Create Month-End Reconciliation Pressure

Timing differences are one of the most common reconciliation challenges.

Delayed settlements and transaction feeds

External systems may update after accounting records.

Cross-period posting inconsistencies

Transactions may be recorded in different reporting periods.

Outstanding transactions remaining unresolved before close

Open items require investigation before financial statements are finalized.

Impact of aging reconciliation items on reporting readiness

Older exceptions become more difficult to resolve.

Common Reconciliation Issues That Delay Month-End Close

Several recurring issues create close delays.

Duplicate transactions and duplicate postings

Duplicates can overstate balances.

Missing transactions and incomplete records

Missing activity creates unsupported balances.

Incorrect account mappings and coding errors

Coding issues affect classification and reporting.

Unsupported adjustments and write-offs

Manual corrections require validation.

Unresolved exceptions carried into future periods

Open issues increase reporting risk.

Reconciliation Controls That Improve Close Accuracy

Controls help finance teams maintain consistency.

Segregation of duties across finance workflows

Separate responsibilities reduce error risk.

Validation checkpoints before ledger posting

Checks help identify issues before balances are finalized.

Approval governance for adjustments and write-offs

Approvals support accountability.

Documentation standards supporting audit readiness

Strong documentation supports reporting confidence.

How Automation Supports Multiple Reconciliation Types

Automation helps finance teams manage larger transaction volumes.

Automated matching across finance systems

Matching engines compare transactions from multiple sources automatically.

Real-time visibility into unresolved balances

Teams can review issues as they occur.

Continuous validation before close deadlines

Problems are identified earlier in the reporting cycle.

Reduced repetitive manual review effort

Finance professionals can focus on exception analysis instead of repetitive transaction matching.

Future Direction of Reconciliation and Month-End Close

Month-end close processes are becoming more proactive and data-driven.

AI-assisted identification of unusual transaction activity

AI can highlight exceptions requiring attention.

Predictive detection of close-related risks

Potential reporting issues can be identified earlier.

Continuous reconciliation across enterprise finance systems

Organizations are moving away from period-end dependency.

Real-time close readiness supported by intelligent matching logic

Continuous validation creates cleaner closes, stronger reporting confidence, and more reliable financial statements.

Sign in to leave a comment.